Buying an Investment Property with Super Explained - A Complete Guide for Australian Investors

Last updated: April 2026 - Financial year 2025-26

Buying an investment property with super, or more precisely buying an investment property with superannuation through an SMSF, is possible in Australia, but it is not just a smarter-sounding version of a normal property purchase. You are not buying in your own name. You are buying through a self-managed super fund (SMSF), usually with tighter borrowing terms, more compliance, and far less room for sloppy paperwork or lifestyle use.

That is why this topic gets misunderstood. Many investors hear "15% tax" and "property inside super" and assume it is an obvious upgrade over buying personally. The reality is more nuanced. Residential SMSF property cannot be lived in by you or your family, major borrowing mistakes can be expensive, and losses stay inside the fund rather than reducing your salary tax bill. In other words: the structure can be powerful, but only if the property, the cash buffer, and the compliance burden all make sense together.

This guide breaks down exactly how buying an investment property with super works in 2026, the rules you must satisfy, the costs that catch trustees out, and the situations where an SMSF purchase is genuinely worth considering. It also shows you how the super route compares with a normal investment property purchase, where due diligence, stamp duty, conveyancing, and cash flow still matter just as much as the tax wrapper.

Rule settings in this guide were checked against ATO, Moneysmart, and RBA guidance in April 2026.

General information only: This guide is educational content for Australian property investors. It is not personal financial, tax, legal, or SMSF advice. Before you buy property through super, get advice from a licensed financial adviser, SMSF accountant, and property solicitor who can review your fund, borrowing structure, and compliance risks.

Methodology note: The worked example and calculator screenshots in this guide were checked against live PropBoss calculator outputs on 28 April 2026, while SMSF rule references were aligned to ATO and Moneysmart guidance and the rate setting cited here was checked against the RBA.

What Does Buying an Investment Property with Super Mean?

Buying an investment property with super means using an SMSF to acquire residential or commercial real estate for retirement purposes. The property is owned by the fund's trustee structure, not by you personally, and every decision has to satisfy the SMSF's investment strategy and the "sole purpose test" of providing retirement benefits to members.

That difference changes almost everything. If you buy personally, income, deductions, and capital gains sit in your own tax position. If you buy through super, rent and expenses sit inside the fund, losses generally stay inside the fund, and any borrowing must be done under a limited recourse borrowing arrangement (LRBA) rather than a standard investment loan. Residential property also has a hard line around related-party use: you cannot move in, your relatives cannot move in, and the property cannot quietly become a family asset later.

It also means the property decision cannot be separated from the rest of the fund. An SMSF that uses most of its balance on one property is taking a concentration bet. That may be fine for some investors with a long horizon and strong contributions, but a poor fit for others who would be better served by diversified exposure through super plus a personal property strategy. If you are still weighing the non-super route, read our broader guide to buying an investment property in Australia as well.

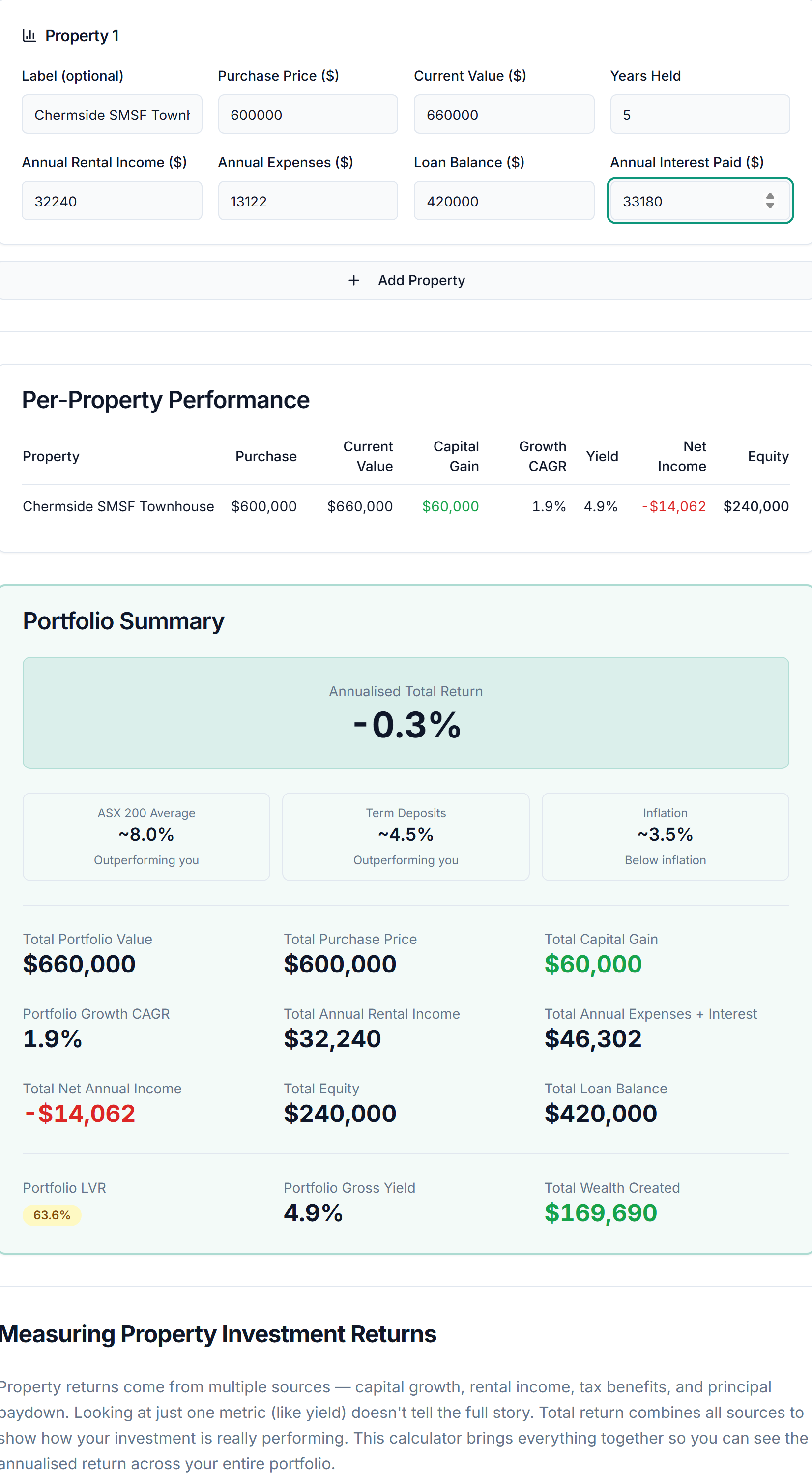

Worked Example: Buying a $600,000 Brisbane Investment Property through an SMSF

Assume a two-member SMSF wants to buy a $600,000 townhouse in Chermside, Brisbane, using an LRBA. The fund has $335,000 in combined super, steady employer contributions, and wants to keep a meaningful liquidity buffer after settlement.

Acquisition Snapshot

| Item | Amount |

|---|---|

| Purchase price | $600,000 |

| Deposit (30%) | $180,000 |

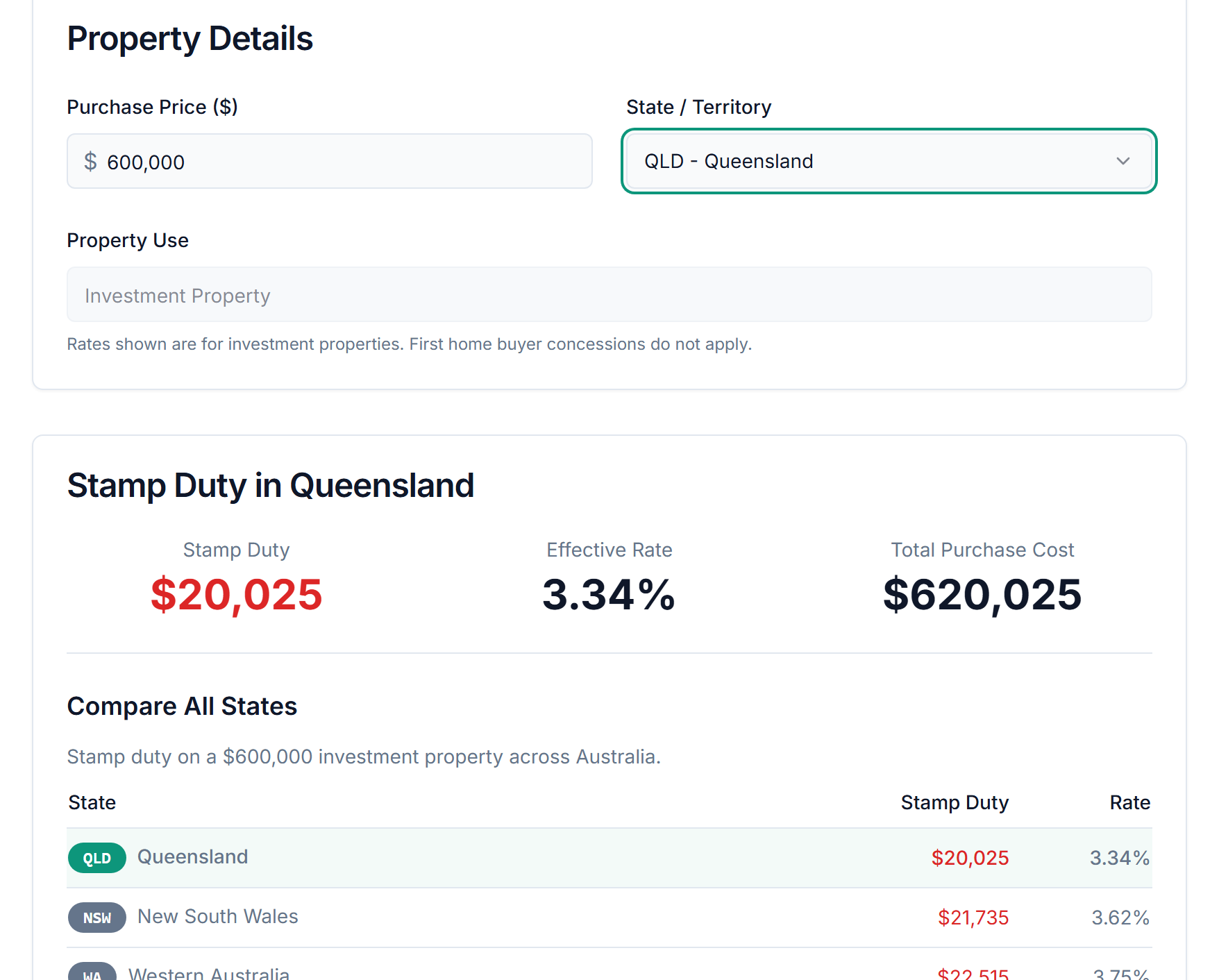

| Stamp duty (QLD investor) | $20,025 |

| Bare trust / LRBA legal setup | $4,500 |

| Conveyancing, searches, registration | $2,200 |

| Loan valuation / establishment fees | $1,200 |

| Building and pest inspection | $650 |

| Cash buffer retained in SMSF after settlement | $45,000 |

| Total SMSF cash needed before loan drawdown | $253,575 |

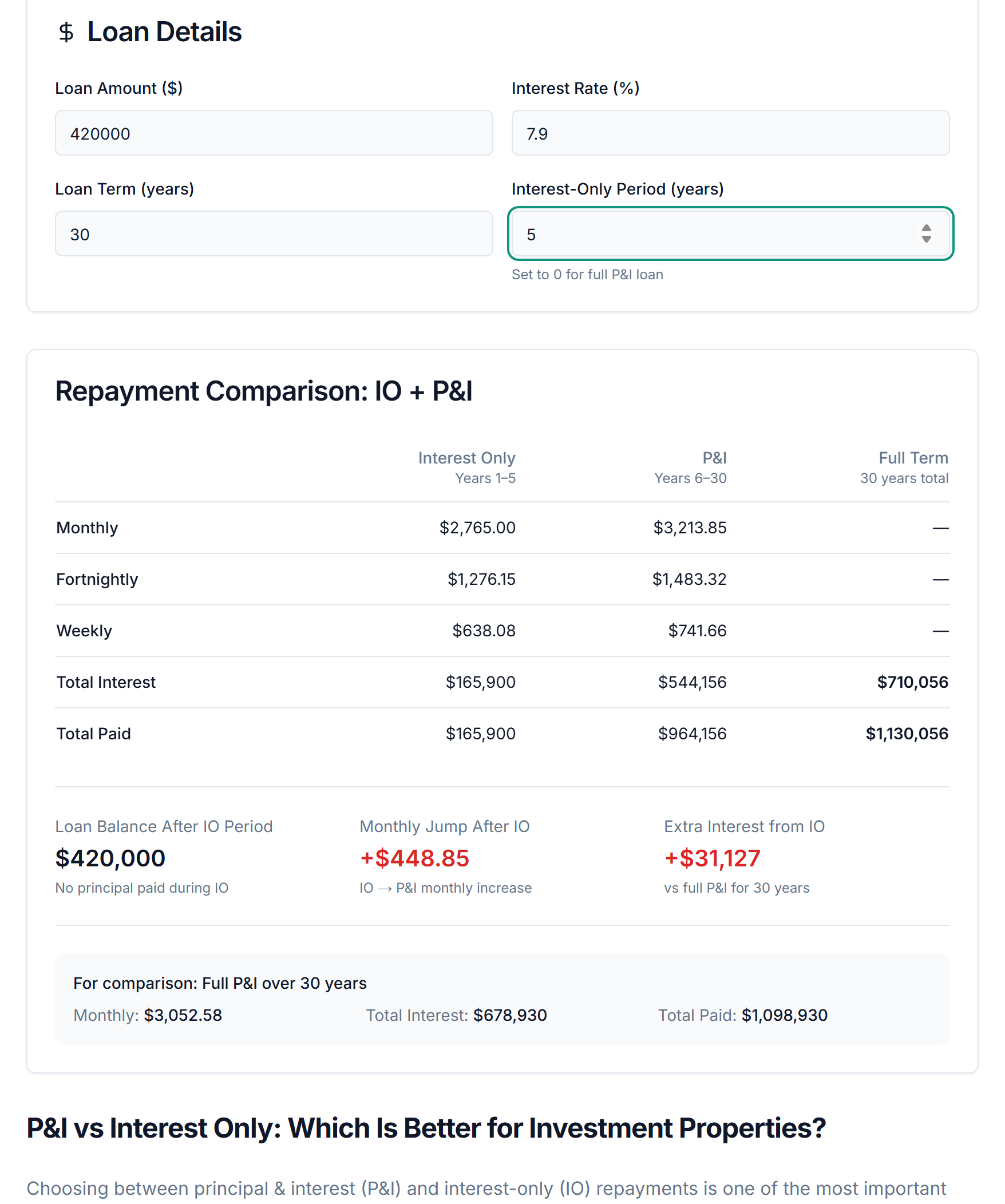

| Loan amount | $420,000 |

The live calculator output matches the Queensland transfer duty figure used in this worked example and shows why duty needs to be budgeted alongside the deposit rather than treated as a small side cost.

Year 1 Income and Costs

| Item | Annual Amount |

|---|---|

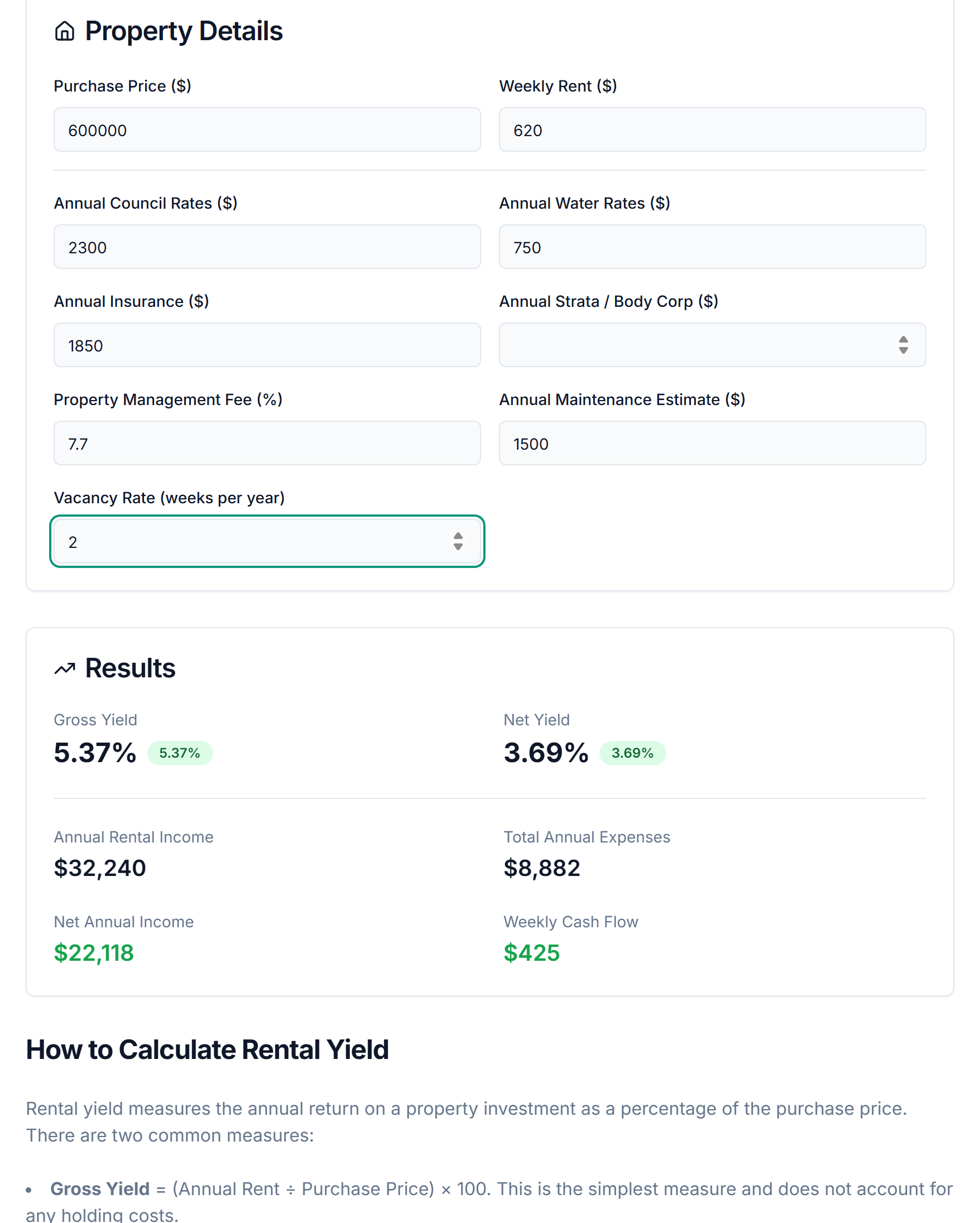

| Gross rent ($620 per week) | +$32,240 |

| Loan interest (7.90% on $420,000) | -$33,180 |

| Property management (7% + GST) | -$2,482 |

| Council and water rates | -$3,050 |

| Building and landlord insurance | -$1,850 |

| Repairs and maintenance reserve | -$1,500 |

| SMSF audit, accounting, admin | -$3,000 |

| Vacancy allowance | -$1,240 |

| Net cash result before depreciation | -$14,062 |

| Estimated depreciation deductions | -$6,500 |

| Tax result inside the SMSF | -$20,562 |

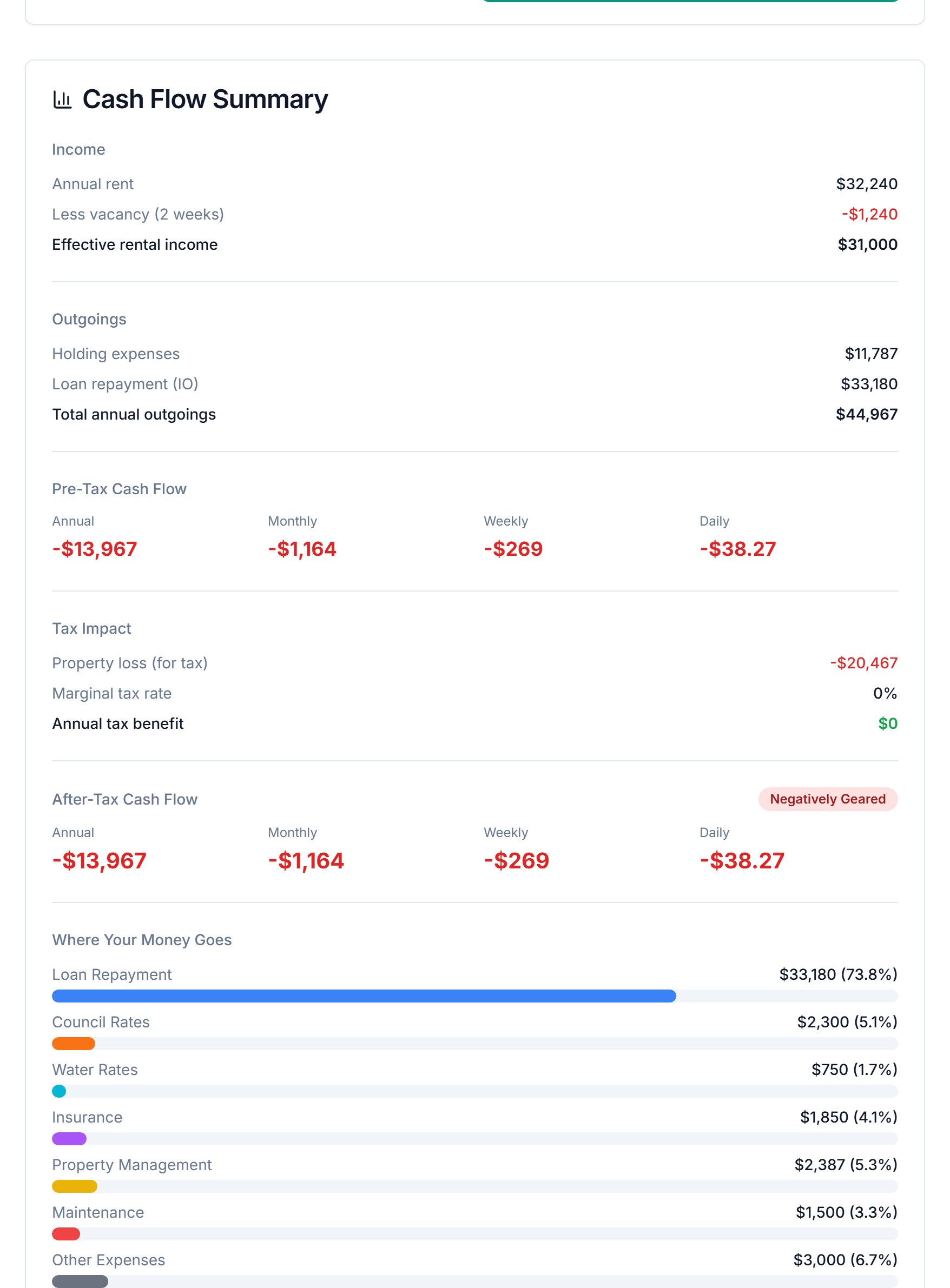

For SMSF use, the taxable income field was set to $0 so the calculator does not assume a personal PAYG offset outside the fund. The point here is to stress-test the rent, debt, vacancy, and holding costs, not to pretend the fund's loss can reduce your salary tax. The calculator lands $95 less negative than the table because it applies the management fee to collected rent after the vacancy allowance rather than to gross scheduled rent.

That last line is where many investors get caught. If the SMSF makes a tax loss, the fund does not use that loss to reduce your personal salary tax. Moneysmart explicitly warns that tax losses from SMSF property cannot be offset against income outside the fund. The benefit only exists inside the SMSF, either against other fund income or as a carried-forward tax loss.

This is why the real decision is not "Can I buy property with super?" but "Can my SMSF carry the deposit, the fees, the vacancy risk, the compliance burden, and the concentration risk without damaging the rest of the fund?"

How Does Buying an Investment Property with Super Work?

1. Build a fund balance that is actually workable

There is no legal minimum SMSF balance for property, but there is a practical minimum where the numbers stop being silly. Once you allow for a 20% to 30% deposit, stamp duty, legal work, setup costs, and a cash buffer, many SMSF property deals only become sensible when the fund has roughly $250,000 to $300,000 or more.

The ATO's 2025-26 contribution caps matter here. The concessional contribution cap is $30,000 and the non-concessional cap is $120,000. Those caps can help you build a fund faster, but they also limit how quickly you can repair a stretched SMSF after settlement. If the property is likely to consume nearly all of the fund, the transaction probably needs more patience or a different structure.

2. Set up or review the SMSF properly

Before any contract is signed, the fund needs a valid trust deed, trustee structure, bank account, tax registrations, and an investment strategy that clearly explains why property suits the fund's goals and risk profile. That strategy cannot be a generic template. It needs to address return expectations, liquidity, diversification, insurance, and how the fund will handle periods where rent or contributions fall short.

This is where many trustees confuse enthusiasm with governance. If you would struggle to explain to an auditor why the property fits the SMSF better than diversified super investments, you are not ready yet.

3. Decide whether residential or commercial property is the better fit

Residential property is the most common path, but it is also the more restrictive one for related-party use. No member, spouse, child, parent, or other related party can live in it or rent it. That makes the purchase clean from a compliance point of view, but it also means the property must stand on its own as a pure investment.

Commercial property can be more flexible. If it qualifies as business real property, the SMSF may be able to buy it and lease it to a related business at market rent. That is one reason business owners compare SMSF property with other ownership structures such as property trusts. The upside is control. The downside is that every lease, valuation, rent review, and cash movement needs to look unquestionably commercial.

4. Arrange borrowing under an LRBA if needed

If the SMSF is not buying outright, the borrowing must be done under an LRBA. The ATO notes that an LRBA is designed around a single acquirable asset and that real property on separate titles is not automatically treated as one asset. That matters because sloppy structuring at purchase can become a legal and tax problem later.

In practice, SMSF lenders often want bigger deposits, tighter serviceability, and stronger cash reserves than standard investment lending. This is also where loan-to-value ratio discipline matters. A lower LVR may feel conservative, but it gives the fund more room to survive vacancy, rate pressure, and unexpected expenses.

5. Settle in the correct name and run everything at arm's length

The contract, holding trust, and title structure all need to be correct from day one. If the paperwork is wrong, the fix can be expensive and, in some cases, impossible without unwinding the arrangement.

After settlement, all rent, expenses, rates, insurance, loan repayments, and maintenance need to flow through the SMSF or its approved structure. If you quietly pay a bill personally or let a related party use the property "just for a few weeks", you are not being flexible - you are creating audit and compliance risk.

If you are still comparing where to direct capital, our guide to where to buy investment property in Australia can help you weigh market selection separately from SMSF structure.

Tax Treatment: SMSF Ownership vs Personal Ownership

One of the biggest mistakes in this space is assuming SMSF property works like normal personal investing with a lower tax rate. It does not. The tax wrapper changes the math and the limits.

| Structure | Rental income tax treatment | Capital gains treatment on assets held 12+ months | Can losses reduce your personal salary tax? |

|---|---|---|---|

| Personal ownership | Taxed at your marginal rate | 50% CGT discount for individuals | Yes, if the property is negatively geared |

| SMSF in accumulation phase | Generally taxed up to 15% | Effective 10% CGT rate after the one-third fund discount | No - losses stay inside the SMSF |

| SMSF in retirement / pension phase | Often more concessional, subject to super rules and caps | Often more concessional, subject to super rules and caps | No - still not a personal tax offset |

That is why the super route is not automatically "better" just because the headline tax rate is lower. If the property is heavily negatively geared, a personal investor on a higher marginal rate may get a larger immediate tax effect than an SMSF investor, even though the long-run super environment may still be attractive.

Model the debt side with our free Loan Repayment Calculator, then run the holding costs through our Cash Flow Calculator before assuming the SMSF path wins.

Using the same $420,000 debt figure from the worked example shows the pressure point clearly: low IO repayments help short-term cash flow, but the later P&I reset is much heavier and needs to be survivable inside the fund.

What Your SMSF Can Pay For - And What It Cannot

The easiest way to stay out of trouble is to think of the property as a fund asset with commercial rules, not as a family asset with future retirement plans attached.

| Item or Action | What it means in practice |

|---|---|

| Deposit and purchase costs | The SMSF can fund the deposit, duty, legal fees, and approved acquisition costs from fund money. |

| Loan interest and bank fees | Deductible to the SMSF where they relate to earning assessable income, but they still need to be affordable in cash terms. |

| Rates, insurance, management, and repairs | Ongoing costs can be paid by the fund and should be budgeted from day one. |

| Depreciation and property-related deductions | The SMSF can generally claim eligible deductions, but those deductions only help inside the fund. |

| Buying from a related party | Generally restricted, although business real property can be an exception if acquired at market value. |

| Living in the property | Not allowed for residential SMSF property if you are a member or related party. |

| Renting to a related party | Not allowed for residential SMSF property. Commercial property can be different if the rules are satisfied and rent is at market value. |

| Major improvement with borrowed LRBA funds | Not allowed. Repairs and maintenance are different from changing the character of the asset. |

| Personal payment of SMSF property bills | Risky. Mixing personal and fund expenses can create compliance issues. |

| Using the property as a lifestyle bridge to retirement | Also risky. The fund has to satisfy retirement-purpose rules first, not personal convenience. |

This is also why traditional buying checks still matter. An SMSF investor still needs strong due diligence, clarity on body corporate exposure, understanding of strata obligations, awareness of torrens title versus strata ownership issues, and caution around off-the-plan settlement risk.

Residential SMSF Property vs Commercial SMSF Property

Commercial property is often treated as an advanced variation, but it can actually be the cleaner strategic fit for some business owners because the related-business lease exception is clearer than the rules for residential use.

| Factor | Residential SMSF property | Commercial SMSF property |

|---|---|---|

| Related-party use | Members and related parties cannot live in or rent it | A related business may lease it if it qualifies as business real property and the lease is at market value |

| Common reason investors choose it | Long-term capital growth and rental income | Business premises control plus rent flowing into super |

| Lending profile | Usually conservative, with bigger deposits and buffers | Also conservative, sometimes even tighter depending on asset type |

| Operational complexity | High | High, plus lease documentation and valuation discipline |

| Lifestyle temptation | High - especially if it is in a desirable area | Lower, because it is usually a working asset |

| Best suited to | Investors focused on retirement wealth and tenant income | Business owners wanting property exposure through super |

If you are exploring the commercial angle, our commercial property investment guide is a useful companion. If you are comparing broader strategy options, our property investment strategies guide covers how SMSF property fits alongside more conventional portfolio building.

Is Buying an Investment Property with Super Worth It in 2026?

The short answer is: sometimes, but the hurdle is higher than the marketing makes it sound.

The interest-rate environment is still demanding

The RBA cash rate target is 4.10% effective 18 March 2026. That matters because SMSF lending tends to price above standard investment lending, which means the fund's margin for error is thinner. If the property only works when everything goes right, it probably does not work.

The rule environment is stable, but still strict

The core rule set has not become more relaxed just because SMSF property is better understood than it was a decade ago. The sole purpose test, related-party restrictions, LRBA limits, annual valuation and audit expectations, and market-value dealing rules are still the centre of the structure. The government has not turned SMSF property into an easy shortcut around normal property-investment discipline.

Property inside super is common, but that does not mean it suits everyone

Moneysmart says there were more than 653,000 SMSFs at 31 December 2025 holding more than $1 trillion in assets, with around 17.5% of SMSF assets in residential and commercial property. That tells you SMSF property is mainstream enough to study seriously. It does not tell you that your fund should do it.

It is usually a better fit when all four of these are true

- Your fund has enough capital to keep a real cash buffer after purchase.

- You have a long time horizon before major retirement drawdowns.

- You understand that tax losses do not reduce your salary tax outside the fund.

- The property adds to the fund's strategy rather than replacing diversification with hope.

It is usually a poor fit when any of these are true

- The fund would become almost entirely one property.

- You need to stretch on the deposit or rely on future contributions just to survive.

- You are mainly attracted by the idea of eventually using the property personally.

- You do not want the paperwork, audit, valuation, and compliance burden.

For many Australians, the better answer is to keep super diversified and build property outside super instead, using strategies such as rentvesting, equity release, or a conventional investment loan.

Why Liquidity and Diversification Matter More Than Tax Hype

The most important sub-topic in this entire guide is not tax. It is liquidity.

Tax benefits are easy to market because they sound clean and immediate. Liquidity risk is harder to sell because it forces you to ask uncomfortable questions. What happens if the property sits vacant for 10 weeks? What happens if one member stops working and concessional contributions fall? What happens if the fund has to cover a large repair, a death-benefit withdrawal, or refinance at a worse rate?

Moneysmart's risk framing is useful here: the fund still has to meet property expenses, loan repayments, and future benefit obligations, and it may have to sell the property at the wrong time if cash pressure rises. That matters even more when the fund is concentrated in one asset and you do not have the same flexibility you would with listed investments.

Diversification is the other half of the problem. If the fund owns mostly one property, you are making a location bet, a tenant-risk bet, a debt bet, and a timing bet all at once. That is why trustees should review how SMSF property sits alongside other assets, not just whether the property itself looks attractive. If your broader plan is portfolio growth, compare the super route with non-super alternatives such as investment property in Perth or other diversified buying paths before locking the fund into a single asset.

Common SMSF Property Mistakes to Avoid

Treating SMSF property like personal negative gearing

An SMSF loss is not the same as a personal rental loss. The fund can use deductions internally, but you do not get to offset the loss against your salary outside the fund. This mistake makes bad deals look good on paper.

Starting with too little super and no real buffer

If the deposit wipes out the fund's flexibility, the SMSF becomes fragile from day one. A property strategy with no margin for vacancy, repairs, or rate shocks is a stress strategy, not a retirement strategy.

Getting the legal structure wrong at purchase

Title, trustee names, and bare trust paperwork are not admin details to clean up later. If they are wrong, you may face double handling, extra duty risk, or an arrangement that is painful to unwind.

Assuming residential property can later become a member benefit

Residential SMSF property is not a "buy now, move in later" shortcut. The structure exists for retirement benefits, not private use. If personal future use is a core attraction, you are probably trying to solve the wrong problem.

Ignoring concentration and liquidity risk

A property that looks great in isolation may still be a bad SMSF asset if it leaves the fund under-diversified and cash-poor. This is especially relevant for trustees who already hold personal property outside super.

Underestimating ongoing compliance

Audit, accounting, valuations, lease discipline, insurance, and annual record keeping are not optional. They are part of the cost of owning the asset through super.

Confusing repairs, improvements, and LRBA limitations

Normal maintenance is one thing. Borrowed-money improvements that change the character of the property are another. If your strategy depends on a major renovation after purchase, you need specialist advice before assuming the SMSF structure can support it.

How to Calculate Whether an SMSF Property Deal Stacks Up

The starting point is not the listing price. It is the all-in cash requirement plus the fund-level holding cost.

Step 1: Calculate the SMSF cash needed before settlement

SMSF cash needed = deposit + stamp duty + legal and setup costs + lender fees + inspections + required liquidity buffer

For the Brisbane example above:

$180,000 + $20,025 + $4,500 + $2,200 + $1,200 + $650 + $45,000 = $253,575

Step 2: Calculate the annual property result inside the fund

Net fund property result = annual rent - interest - property costs - SMSF admin costs - vacancy allowance - maintenance reserve

Using the example:

| Item | Annual Amount |

|---|---|

| Gross rent | +$32,240 |

| Total cash costs | -$46,302 |

| Net cash result | -$14,062 |

This is the cleaner debt-free view of the same deal. Before you worry about tax wrappers or borrowing structure, the raw yield numbers tell you whether the rent-to-price relationship is strong enough to justify deeper modelling.

Step 3: Add depreciation and understand the tax effect correctly

If depreciation adds another $6,500 of deductions, the total tax result becomes -$20,562 inside the fund. That can help offset other SMSF income or create a carried-forward tax loss, but it does not reduce your personal PAYG tax bill outside the fund.

Step 4: Ask the only question that matters

After settlement, can the SMSF still survive:

- a rate increase,

- a vacancy period,

- a major repair,

- lower future contributions, and

- the need to stay diversified enough for member retirement goals?

If the answer is no, the structure is too tight.

Check purchase costs with our Stamp Duty Calculator, test holding costs with the Cash Flow Calculator, compare returns with the Rental Yield Calculator, and look at whole-of-portfolio outcomes with the Portfolio Return Calculator.

At the portfolio level, the worked example looks exactly like the strategic warning in this guide: one property can still build equity over time, but it also concentrates liquidity risk, debt risk, and return expectations in a single asset.

Frequently Asked Questions

Is it worth buying an investment property with super?

It can be worth it if your fund balance is strong, your time horizon is long, and the property will not leave your SMSF short of cash. In practice, SMSF property tends to suit investors with roughly $250,000 to $300,000 or more in super, at least 10 years until retirement, and enough buffer to cover vacancy, rates, insurance, audit costs, and loan repayments. As of 18 March 2026 the RBA cash rate target is 4.10%, which keeps SMSF borrowing expensive, so the deal needs to work on cash flow and risk - not just tax. If your balance is small, your fund would become too concentrated, or you need flexibility, diversified super investments may be the better fit.

Can I buy an investment property with my super?

Yes, but only through a self-managed super fund (SMSF). You cannot simply withdraw money from an industry or retail super fund to buy an investment property in your own name. If the property is residential, neither you, your relatives, nor any other related party can live in it or rent it. The purchase must satisfy the sole purpose test, be run at market value, and comply with the SMSF borrowing and related-party rules.

How do you buy an investment property through an SMSF?

The usual process is to set up or review your SMSF, document an investment strategy that supports property, roll over or contribute enough capital, keep a liquidity buffer, arrange an LRBA and holding trust if borrowing is required, and settle the purchase in the correct trustee structure. After settlement, all rent, expenses, loan repayments, insurance, and compliance costs must flow through the SMSF. The property must then be managed at arm's length and reviewed each year as part of the fund's reporting and valuation process.

How much super do I need to buy an investment property?

There is no legal minimum, but in practice many SMSF property deals become more workable once the fund has about $250,000 to $300,000 or more. That is because the fund may need a 20% to 30% deposit, stamp duty, legal and bare trust costs, lender fees, annual audit and accounting costs, and a cash buffer after settlement. A smaller balance can be possible, but it often leaves the fund too concentrated and too exposed to vacancy or rate shocks.

What are the main SMSF property rules and restrictions?

The key rules are the sole purpose test, related-party acquisition rules, arm's-length dealing requirements, and LRBA restrictions. Residential property generally cannot be acquired from, lived in by, or rented to members or related parties. If the fund borrows, the LRBA must be limited to a single acquirable asset and major improvements with borrowed money are not allowed. Trustees also need annual accounts, audit, valuations, and records that show every transaction was run on commercial terms.

Can I buy an investment property with my super and rent it to myself?

Not if it is residential property. An SMSF residential property cannot be rented to you, your spouse, your children, or other related parties. Doing it anyway can trigger compliance breaches, forced rectification, and potential ATO penalties. Commercial property is different: if it qualifies as business real property, your SMSF may be able to lease it to your business at market rent under a proper lease. That exception is one of the biggest reasons business owners look at SMSF property in the first place.

What are the disadvantages or risks of SMSF property investing?

The biggest risks are concentration, illiquidity, higher borrowing costs, and compliance failure. A single property can dominate the fund, making diversification harder. If the property is vacant or rates rise, the SMSF still needs to meet repayments and ongoing costs. Moneysmart also warns that tax losses from the property cannot be offset against your personal taxable income outside the fund. On top of that, mistakes with title, related-party use, or LRBA structure can trigger serious ATO consequences.

What types of properties can I buy with super?

An SMSF can invest in residential or commercial property, provided the purchase fits the fund's strategy and rules. Residential property is the stricter path because members and related parties cannot use it. Commercial property can be more flexible because a qualifying business premises may be leased to a related business at market value. Off-the-plan property is possible, but it adds extra settlement, funding, and due diligence risk, so trustees need to be especially careful.

How does SMSF borrowing for property work under an LRBA?

Under a limited recourse borrowing arrangement, the lender's claim is generally limited to the acquired asset rather than the SMSF's other assets. The property is usually held in a separate holding or bare trust until the loan is repaid. The arrangement must relate to a single acquirable asset, so the paperwork, title, and trust structure must be set up correctly from day one. In practice, SMSF lenders often want bigger deposits and stronger liquidity than standard investment lending.

What is the 5% SMSF rule?

The 5% rule refers to the in-house asset limit for SMSFs. In broad terms, investments or arrangements involving related parties cannot exceed 5% of the fund's total assets at year end. That matters because some property-related structures can accidentally drift into in-house asset territory if they are not set up correctly. Business real property leased to a related party at market value can be an exception, but trustees should get advice before assuming a property arrangement is safe.

Track Your SMSF Property Strategy Automatically

PropBoss helps Australian investors bring property decisions back to the numbers that matter: purchase costs, debt, rental yield, ongoing tax deductions, and portfolio-wide performance. That matters even more when the property sits inside super, where liquidity mistakes and compliance shortcuts can have outsized consequences.

If you are comparing SMSF property with other buying paths, also read our guides to PPOR meaning for investors, rentvesting, and property investment strategies.

Get Started Free | Try the Calculator

Related Guides & Tools

- Loan Repayment Calculator - model repayments under different deposit and rate scenarios.

- Stamp Duty Calculator - estimate upfront transfer duty before the SMSF signs anything.

- Cash Flow Calculator - test whether the property still works after interest, rates, and management costs.

- Rental Yield Calculator - compare gross and net yield across different markets.

- Where to Buy Investment Property in Australia - research location quality before you commit fund capital.

- Commercial Property Investment Guide - compare the residential SMSF path with commercial-property opportunities.