Refinancing Investment Property Tax Implications Explained

Check what you can still claim when refinancing an investment property, including interest deductibility, borrowing costs, break costs, CGT issues, and mixed-use loan traps.

Refinancing an investment property in Australia can change what interest, loan fees and capital gains tax items you can claim, because deductibility follows how the new borrowed funds are used. If the refinancing simply replaces an existing investment property loan on the same investment property, the tax outcome is usually straightforward. If you redraw, cash out, or mix personal and investment purposes, the tax implications become more complex very quickly. The complexity is manageable with clean settlement documentation.

Before you change lenders, model the repayment impact in the refinance calculator and compare it with the tax position and equity release plan. A lower rate can help cash flow, but the replacement-loan structure matters just as much. If you are still deciding, pair this article with Refinance Investment Property Loan: Should You Switch in 2026?.

How refinancing impacts your investment property loan in Australia

Refinancing Investment Property Tax Implications Australia at a glance

A refinance does not create a deduction by itself. What matters is whether the new loan is still being used for income producing purposes.

If your replacement loan clears the balance of an existing investment property loan and the property remains an investment property, the related loan interest will usually stay deductible. Interest on a refinanced loan remains tax deductible if the loan continues to fund investment purposes. If you increase the loan and use part of the extra debt for private spending, only the investment portion may be tax deductible.

When you can claim tax deductions after refinancing

Most investors want to know whether they can still claim tax deductions after loan restructuring. The answer is usually yes for the replacement debt, but only if the refinance keeps supporting the same income producing asset.

For example, assume your original investment loan balance is $420,000 on a Brisbane rental property and you refinance to a replacement loan of $420,000 with a lower rate and lower annual fees. The underlying use of the debt has not changed, so the interest payments should generally keep the same tax character.

If you refinance to $470,000 and use the extra $50,000 for a family car, holiday or school fees, that extra portion is private. In that scenario, you would not claim tax deductions on the private interest even though the whole facility sits against the same property.

Interest deductibility depends on the use of borrowed funds

The Australian Taxation Office (ATO) Interest expenses guidance focuses on use, not security. In other words, the fact that a new loan is secured by your rental property does not automatically make all interest deductibility available.

This distinction matters when investors access equity. If the extra amount funds another income-producing purchase or its acquisition costs, the interest may still be deductible. If it goes to private use, deductibility usually stops there.

Interest expenses on the replacement loan

Interest expenses on the replacement part of the refinanced debt usually follow the original investment purpose. The interest bill on additional split loan amounts depends on the separate use of those borrowed funds.

When lower interest rates do and do not improve your tax position

Lower interest rates can improve after-tax cash flow, but they do not change the tax law. Paying less interest may reduce the deduction, yet you are still ahead if the cash saved is greater than the tax you give up.

Some investors overvalue a deduction and forget that a $1 deduction does not save $1. At a 37% marginal rate, $1,200 less deductible interest cuts tax by about $444, but you still keep the other $756 in cash.

Borrowing costs, loan fees and discharge fees

Refinancing costs trip investors up because borrowing expenses, ongoing loan fees, and capital costs do not all get the same tax treatment.

Some replacement-loan fees are spread over five years or the loan term, whichever is shorter. Others sit inside borrowing expenses rather than immediate deductions. The ATO borrowing expenses guidance is the starting point for sorting those line items.

If total borrowing expenses are $100 or less, you can generally claim the full amount in the income year the expense is incurred. Totals above $100 are usually spread over the loan term or five years, whichever is shorter.

Deductible refinancing costs can include loan establishment fees, mortgage discharge fees, valuation fees and, in some cases, lender's mortgage insurance on a rental property, with those amounts often spread over five years when they are treated as borrowing expenses.

Are break costs tax deductible?

Break costs can be deductible in some situations where they relate to ending a fixed-rate investment loan used for a rental property, but the facts matter. The ATO generally looks at why the cost was incurred and whether it is sufficiently connected to earning rental income.

If those break costs arise because you are replacing one investment property loan with another on the same asset, the connection is usually much stronger than if you are refinancing for private reasons.

Loan fees and discharge fees

Loan fees can include loan establishment fees, title search costs, mortgage registration, mortgage broker fees, and some lender legal charges. Discharge fees paid to exit the old loan may also need to be considered separately from those costs on the replacement loan.

For a worked refinance comparison, list every exit cost, application cost and annual fee. That gives you the real refinancing cost rather than a marketing estimate.

When capital gains tax changes and when it does not

Refinancing by itself does not trigger capital gains tax. CGT usually happens when you dispose of the property, not when you change lenders on the same title. The ATO property and capital gains tax guidance is most useful when the refinance sits alongside a sale, transfer or ownership change.

Where investors get confused is when refinancing supports later transactions that affect the cost base, ownership structure, or mixed private use of the property. The issue usually sits in the evidence trail rather than the refinance itself.

Improvements funded with borrowed money can affect your cost base and reduce a later taxable gain. Some refinance-related capital costs are not deductible now but can still be added to cost base, while ordinary loan interest and many borrowing expenses stay in the income-tax bucket.

If you need the broader selling-side rules, read Capital Gains Tax on Property: What Australian Investors Need to Know in 2026. The refinance itself usually is not the CGT event, but what you do around the refinance can affect later record-keeping and cost-base evidence.

Cash-out refinance for personal and investment purposes

The highest-risk refinance structure is a mixed loan used for personal and investment purposes. This is where refinancing can become expensive from a tax point of view.

Assume you refinance an investment property to a new loan of $600,000. Of that amount, $520,000 replaces the original investment loan, $40,000 pays refinancing fees and minor improvements to the property, and $40,000 is transferred into your offset account to fund a private renovation at home. In that case, the interest on the first two portions may be tax deductible, while the private portion is not.

The ATO expects apportionment where borrowed funds have mixed use. A single blended account can make that calculation messy, so many accountants recommend separate splits from day one.

For example, if 95% of the refinanced balance still relates to the rental property and 5% has shifted to private use, you would keep apportioning interest on that 95/5 mix until the underlying loan purpose changes again.

Can I refinance investment property to pay off primary residence?

You can do it commercially, but that does not make the interest on that portion deductible. If you refinance an investment property to pay off your principal home loan, the secured property is less important than the use of the borrowed funds.

That means the extra debt used to reduce your owner-occupied mortgage is usually private, even though the refinance is against the property. This is one of the most common traps in investment property refinancing.

Worked example: split use of a refinance facility

Consider an investor with an existing loan of $480,000 on a Sydney rental property earning $760 per week. They refinance into a new loan of $560,000 at 6.14%.

Use of funds:

| Loan portion | Amount | Purpose | Likely tax treatment |

|---|---|---|---|

| Replacement debt | $480,000 | Replaces original investment loan | Interest usually deductible |

| Property repairs | $20,000 | Roof leak and safety works on the property | Interest usually deductible |

| Equity release | $60,000 | Home kitchen renovation | Interest usually private |

Annual interest on the full facility at 6.14% is about $34,384. If 60,000 of 560,000 is private, about 10.71% of the interest is private. That means roughly $3,682 would be non-deductible and about $30,702 may relate to the income producing purposes.

A split facility is cleaner than a blended loan. It simplifies tax reporting and gives your accountant a defensible trail.

Worked example: borrowing expenses over five years

Now assume you refinance an investment property with these costs:

- application fee: $450

- valuation fee: $300

- mortgage registration and settlement fees: $420

- broker fee not paid by lender: $830

- lender legal fee: $500

Total borrowing expenses are $2,500. If the new loan term is 25 years, many investors would generally spread those borrowing expenses over five years because that is shorter than the loan term.

That would mean a deduction of about $500 per year, subject to the exact character of each cost. It is not a huge line item, but it matters when lenders are otherwise close on cost.

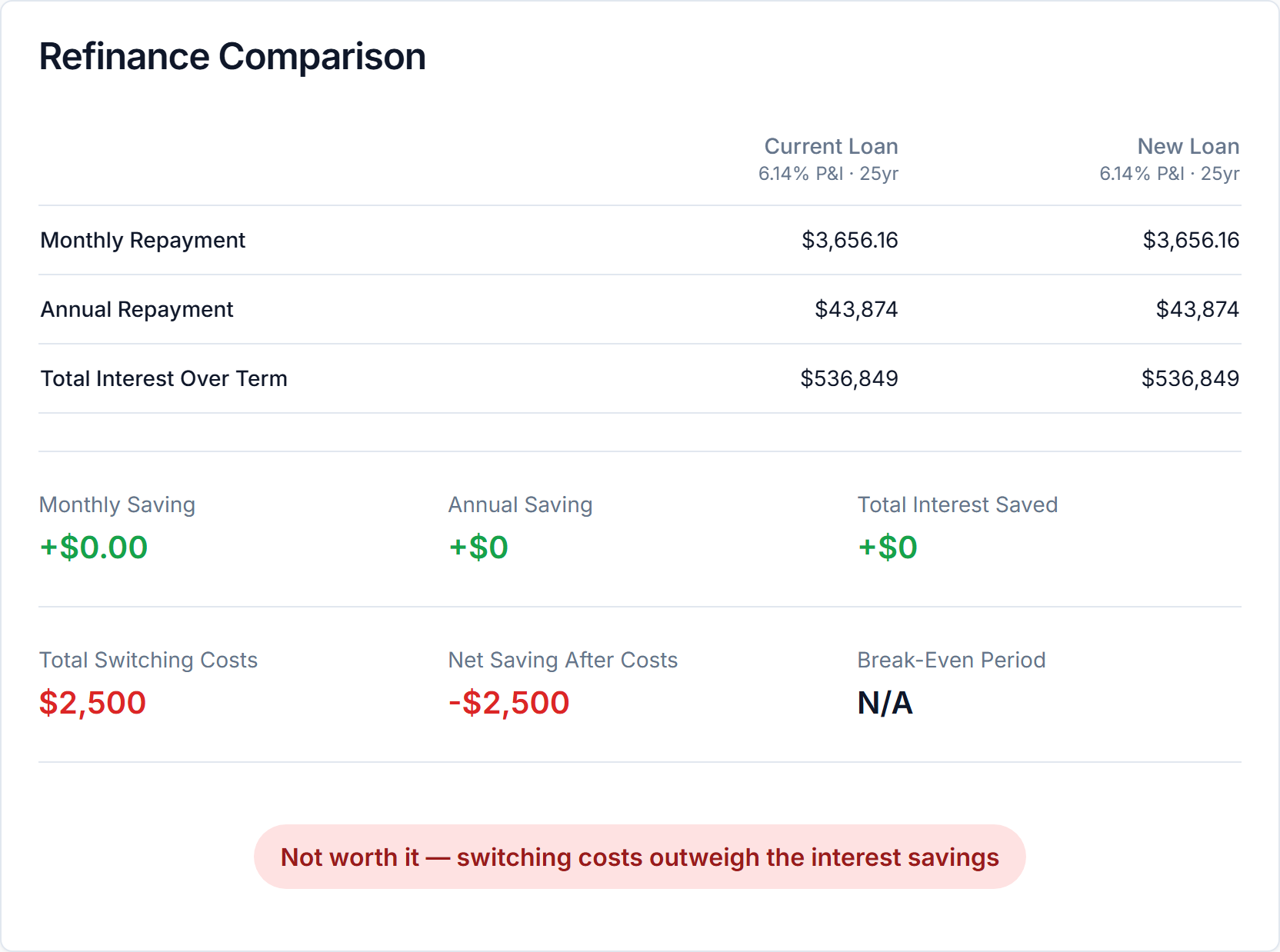

Using the same $560,000 loan balance from the mixed-use example and a $2,500 switching-cost stack, the live PropBoss refinance calculator shows why a refinance still fails the cash-flow test when the rate does not improve. At the same 6.14% rate over 25 years, the calculator holds monthly repayments at $3,656.16, shows annual repayments of $43,874, and leaves the switch $2,500 behind with no break-even point.

Assess your financial circumstances before you refinance

The best refinance is not always the cheapest advertised rate. Holding period, loan structure, refinancing costs, equity plans and offset strategy all matter, and similar repayments can still produce different tax outcomes.

Ask these questions before refinancing your investment property:

- Will the new loan stay purely investment related?

- Are there fixed-rate exit fees on the current fixed loan?

- Will you redraw for personal and investment purposes later?

- Are the loan fees recovered by rate savings inside two to three years?

- Does the lender allow useful split structures for future purchases?

What to document for your accountant

Good documentation is part of the tax outcome. Keep the refinance credit proposal, settlement statement, discharge letter, fee breakdown, and evidence of where each amount was transferred after settlement.

Also keep records of any equity release, because funds that move from investment use to private use can change the tax position. Government stamp duty and legal fees for buying another property are usually capital costs added to cost base rather than immediate deductions. Professional tax advice is most useful when the refinance involves multiple properties, trust structures or mixed loan purposes.

FAQ

Is refinance investment property tax deduction available on all fees?

No. Some costs may be deductible over time as borrowing expenses, some may be immediately deductible depending on the facts, and some may be capital or private in nature. You need to review each cost separately before assuming it is tax deductible.

Does refinancing an investment property affect capital gains tax?

Usually not by itself. The refinance alone does not normally create a CGT event, but it can affect later records and the way certain costs are treated if ownership or asset treatment changes.

How much equity can you safely access when refinancing?

That depends on serviceability, loan to value ratio, lender policy, buffer rates, and your risk tolerance. Borrowing more just because equity is available can weaken cash flow if the new debt is not tied to a strong investment purpose.

When should property investors get professional tax advice?

Get professional tax advice before settlement if the refinance includes cash out, mixed personal and investment purposes, trust ownership, or a plan to recycle debt. It is much easier to structure the loan correctly at the start than to untangle a contaminated loan later.

Use the refinance to improve structure, not just the rate

Refinancing an investment property in Australia can improve your position, but the tax implications only stay manageable when the new loan, refinancing fees, and use of funds are set up cleanly. Run the numbers in the refinance calculator, compare the tax effect with the cash-flow effect, and keep your records clear from day one.

If you want a simpler way to track loans, buffers, tax deductions and portfolio performance in one place, start with PropBoss. It gives property investors a cleaner operating layer around the decisions that sit behind the refinance.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more