Property Portfolio Template Australia Guide for 2026

Build a property portfolio template for Australia with the fields, formulas, review cadence, and portfolio checks investors need to track returns in 2026.

Property Portfolio Template Australia: What to Track in 2026

A property portfolio template should track rent, loans, expenses, cash flow, equity, and review notes for every property in one place. If you only record purchase price and weekly rent, you are not really managing a portfolio. You are collecting scattered facts that make it harder to see whether the portfolio is improving or drifting backwards.

For Australian investors, the template matters because rates, insurance, council charges, and maintenance costs do not move in a straight line. One vacancy, one refinance, or one repair blowout can change the result across the whole portfolio. A good template makes that visible before you buy again, hold a weak property too long, or assume a portfolio is performing better than it is.

What a Property Portfolio Template Should Include

The point of the template is not to create a prettier spreadsheet. The point is to show cash flow, equity, and return on investment at property level and portfolio level. Those are the numbers that tell you whether a property is helping the portfolio, dragging on it, or becoming a refinance candidate.

At minimum, each property row should include:

- purchase price

- current market value

- weekly rent and annual rent

- loan balance

- interest rate and annual interest cost

- annual operating costs such as council rates, insurance, management fees, maintenance, and water

- net annual cash flow

- gross yield and simple portfolio notes

If you want the template to stay useful after your first or second purchase, add columns for vacancy allowance, one-off capital works, target rent review date, and a short action note. That note can be as simple as "review refinance in October" or "insurance renewal due next quarter". Without it, the template becomes a scoreboard rather than a decision tool.

Here is a simple starter layout you can copy into Excel, Google Sheets, or your notes app:

| Property | Current value | Weekly rent | Loan balance | Annual interest | Other annual costs | Net cash flow | Equity | Next action |

|---|---|---|---|---|---|---|---|---|

| Property 1 | ||||||||

| Property 2 | ||||||||

| Property 3 |

That gives the reader an actual template object, not just advice about what a template should contain.

A one-property sheet can get away with basic income and expense tracking. A portfolio template cannot. Once you own multiple assets, you need the template to compare properties against each other instead of viewing each one in isolation.

That is where extra fields matter. Add columns for portfolio weighting, blended interest cost, vacancy weeks, and an optional capitalisation rate or target return field if you want a quicker screening view. Residential investors will not use capitalisation rate the same way commercial investors do, but it can still help when you want a simple shorthand for comparing assets before you go deeper.

The practical rule is simple: if a number changes your next decision, it belongs in the template. If it does not, keep it out.

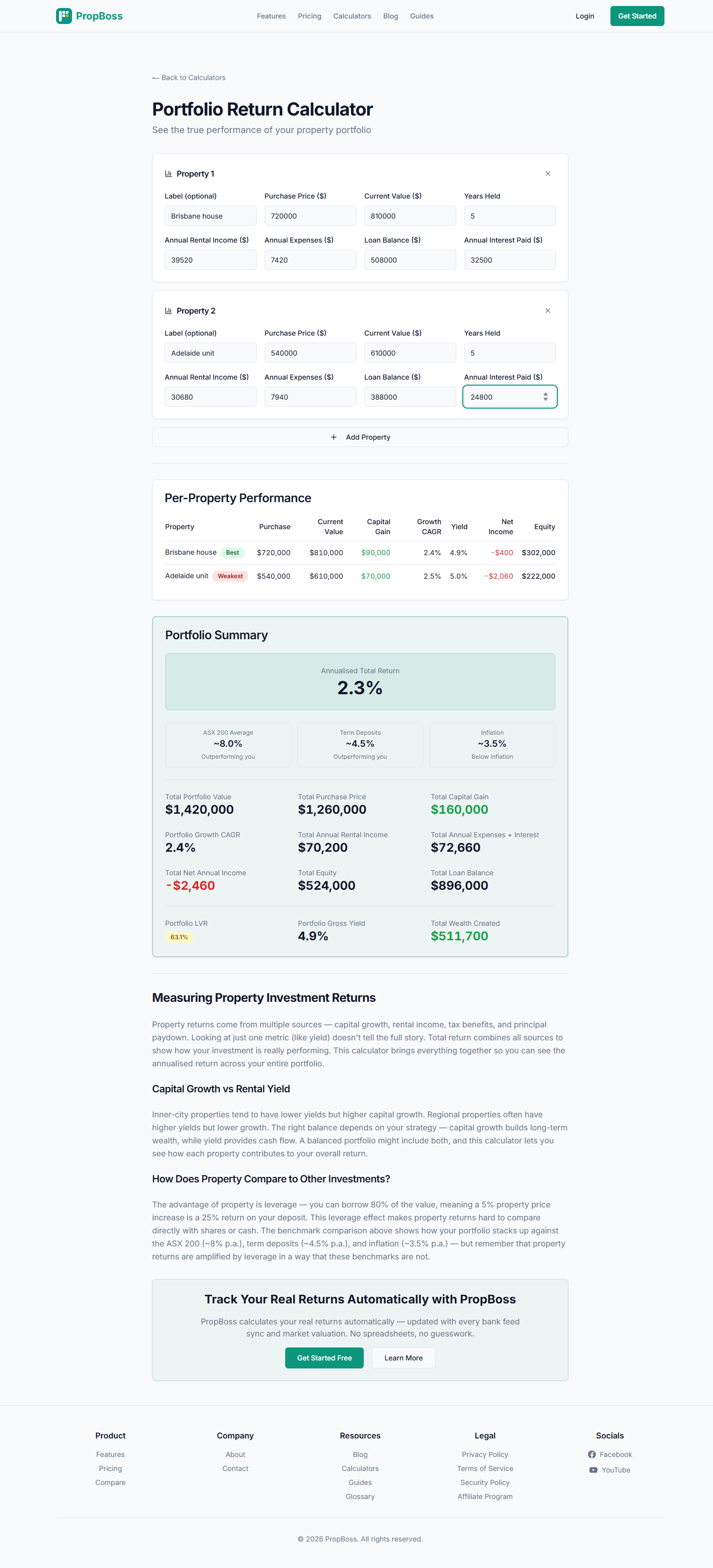

Property Portfolio Template Example for Two Australian Properties

The easiest way to test a template is to run it on a real example. Below is a simple two-property portfolio for an Australian investor reviewing performance at the end of a quarter.

| Property | Purchase price | Current value | Weekly rent | Annual rent | Loan balance | Annual interest | Other annual costs | Net cash flow | Gross yield | Equity |

|---|---|---|---|---|---|---|---|---|---|---|

| Brisbane house | $720,000 | $810,000 | $760 | $39,520 | $508,000 | $32,500 | $7,420 | -$400 | 4.9% | $302,000 |

| Adelaide unit | $540,000 | $610,000 | $590 | $30,680 | $388,000 | $24,800 | $7,940 | -$2,060 | 5.0% | $222,000 |

| Total portfolio | $1,260,000 | $1,420,000 | - | $70,200 | $896,000 | $57,300 | $15,360 | -$2,460 | 4.9% blended | $524,000 |

That table already tells you more than most investors can see from a bank account and a property manager statement. The portfolio is slightly negative on annual cash flow, but it has more than half a million dollars in equity. If the investor expects portfolio-wide capital growth of 3.5% for the next 12 months, that is roughly $49,700 in estimated growth on $1.42 million of assets.

In other words, the template helps you separate three different questions:

- Is the portfolio cash-flow positive right now?

- Is the portfolio building equity fast enough to justify the hold?

- Which property is creating the biggest drag on the overall result?

Without that separation, investors often make the wrong call. They keep a weak property because rent looks healthy, or they panic about a small cash-flow shortfall even though the portfolio is still compounding well.

The example also shows why portfolio review has to happen at total-portfolio level, not just property by property. The Brisbane house is close to neutral on annual cash flow, while the Adelaide unit is more negative, but the combined portfolio still has strong equity and a reasonable blended yield. That creates a very different decision from the one you would make if you only looked at the weaker property in isolation. A good template lets you see whether the next step is to improve rent, trim costs, refinance debt, or simply accept a short-term cash-flow drag because the broader portfolio is still doing its job.

How to Use the Template Each Month and Quarter

Monthly updates keep the template honest. Update rent received, major expenses paid, loan repayment changes, and any material events such as a vacancy, insurance jump, or maintenance item. Many investors only realise how different the portfolio looks from the original plan once those numbers are written down in one place.

If one property is tracking well and another is missing rent, the monthly template shows it early. That matters because decisions about rent reviews, buffers, and refinancing are usually made too late when the investor is relying on memory instead of current numbers.

Quarterly reviews are where the real decisions happen. Revisit current values, compare actual cash flow against the original assumptions, and ask whether the portfolio still supports the next planned purchase. If the answer is unclear, pressure-test the assumptions with the PropBoss portfolio return calculator. That matters even more when the next purchase depends on tight borrowing capacity or a refinance window that may not stay open for long.

Use a supporting tool only when the numbers tell you where the problem sits. If the portfolio is equity-rich but cash-poor, use an equity calculator to test what is actually usable before you redraw or refinance. If cash flow is the issue, compare the annual template numbers against the workflow in Investment Property Cash Flow: How to Calculate Your True Returns.

The ATO's rental property record-keeping guidance matters here too. Your template is not the legal record by itself, but it should tell you whether you have captured the rent, interest, rates, insurance, repairs, and other records you will need at tax time.

Property Portfolio Template vs Portfolio Calculator

A template and a calculator solve related problems, but they are not the same thing.

| Tool | Best use | Main limitation |

|---|---|---|

| Template or spreadsheet | Ongoing record keeping and regular portfolio review | Easy to go stale, especially when assumptions change |

| Portfolio calculator | Scenario comparison before a purchase, refinance, sale, or rent change | Only as good as the inputs you feed it |

The template answers, "What is happening in my portfolio now?" The calculator answers, "What happens if I change something?" That distinction matters. A spreadsheet is great for keeping the portfolio organised, but it does not automatically tell you whether buying one more property, refinancing a loan, or lifting rent by $30 a week actually improves the result.

That is why the strongest workflow is a simple template for ongoing records plus a calculator when you need to compare scenarios. It turns static data into a decision.

For example, a spreadsheet can show that one property is producing a weaker result than expected, but it will not automatically tell you whether the better response is a refinance, a rent increase, a renovation, or a hold decision. A calculator can test those scenarios quickly. That matters when rates move, equity builds unevenly, or the investor is deciding whether to recycle capital into a stronger asset rather than just adding another column to the spreadsheet.

How to Build a Property Portfolio Without Losing Track of the Numbers

Many competitors treat the template as an afterthought and spend most of the article on generic portfolio theory. That is not helpful if you already own property and need a practical system. The real challenge is not understanding that portfolios need structure. It is maintaining a structure that stays useful after the second or third property.

If you are still building the strategy itself, read How to Build a Property Portfolio in Australia. The template in this article sits underneath that strategy. It is the operating layer that helps you review whether the strategy is actually working.

The template is especially useful before common trigger points:

- a refinance or rate reset

- a rent review

- a planned purchase funded by usable equity

- end-of-financial-year record clean-up

- a decision to hold, improve, or sell one underperforming property

When those moments arrive, investors who keep current template data move faster and make calmer decisions than investors who have to reconstruct the numbers first.

What Most Free Portfolio Templates Miss

Many top portfolio templates, free investment spreadsheet downloads, and template-and-landlord bundles are very simple. They may list the real estate portfolio, but they rarely help you decide what to do next. A real estate portfolio is not just an estate portfolio on paper. It is a moving set of loans, rents, costs, and timing decisions.

Some examples also look more like a management plan than an investor worksheet. A government-style plan template such as the RMG500 management plan template DOCX is built to account for the existing property portfolio and governance requirements. That can be useful context, but most Australian investors need a lighter plan template that helps them review cash flow, equity, and purchase readiness.

If you need a complete guide on how to build a property portfolio, treat this template as the operating layer under the broader strategy. Start with goals and borrowing limits, fill the template with current numbers, then use our free portfolio return calculator to compare the next move before you buy again.

Common Mistakes Investors Make With a Property Portfolio Spreadsheet

The most common mistakes are predictable:

- tracking rent but not full holding costs such as council rates, management fees, repairs, and vacancy allowance

- mixing personal and investment records when a former home or shared offset account is involved

- updating the template only when something goes wrong instead of on a regular schedule

- treating the template like the whole decision system instead of the starting point for refinance, hold, or buy-again decisions

If the template never helps you answer a real portfolio question, it is just admin.

FAQ

What should a property portfolio template include?

It should include purchase price, current value, rent, loan balance, interest cost, operating expenses, net cash flow, yield, equity, and a short review note for each property.

How often should you update a property portfolio spreadsheet?

Update rent, expenses, and loan changes monthly. Review values, return assumptions, and next-step decisions quarterly. Do a fuller clean-up before EOFY so the records are ready for tax time.

Can you track multiple properties in one template?

Yes. In fact, that is when the template becomes most useful. The whole value is comparing properties against each other instead of reviewing each one in isolation.

What is the difference between a property portfolio template and a portfolio calculator?

A template records what has already happened. A calculator helps you compare what could happen next. Most investors need both, not one or the other.

When should you stop using a manual spreadsheet and use software or a calculator instead?

Move beyond a basic spreadsheet when you have multiple properties, frequent scenario testing, or too many moving parts to trust manual updates. That is usually the point where calculator-based comparisons save time and reduce mistakes.

Turn a Static Template Into Better Portfolio Decisions

A property portfolio template is useful because it organises the numbers, but the real value comes when those numbers help you make a better decision. If you want to move from record keeping to scenario testing, use the portfolio return calculator to compare the next move, then create your PropBoss account when you are ready to keep those numbers in one place.

External references: ATO records for rental properties, ATO residential rental properties, Moneysmart property investment. For software-backed tracking, see property portfolio management software. If your template includes super-owned property, read SMSF property rules ATO.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more