Investment Property Calculator Australia Guide for 2026

A practical Australian guide to using an investment property calculator with worked numbers, tax context, and portfolio-level checks.

An investment property calculator in Australia should connect purchase costs, loan structure, property expenses, cash flow, capital gains tax, and portfolio impact before you commit.

What an Investment Property Calculator Australia Should Include

An investment property calculator australia investors can rely on needs more than a headline yield. The model should show monthly cash flow and portfolio fit.

At minimum, a serious investment property calculator should include:

- Purchase price, deposit, stamp duty, legal fees, and borrowing costs

- Weekly rent, vacancy allowance, and other income assumptions

- Loan amount, loan term, repayment type, and whether the debt is principal and interest or interest only

- Property expenses such as rates, insurance, management fees, repairs, and maintenance

- Tax settings including depreciation, marginal tax rate, and negative gearing

- Exit assumptions including selling costs, capital gains tax, and growth rate

If the property calculator leaves out ownership costs or tax treatment, the answer is usually too optimistic. To calculate the potential returns on an investment property, investors should consider factors such as purchase price, expected rental income, loan amount, interest rate, and estimated property expenses. A rental property calculator or rental yield calculator can help with a quick screen, but the broader model should compare gross rental yield, net rental yield, annual rental income, operating expenses, and total ROI. Gross rental yield is calculated by dividing the annual rental income by the property's purchase price, expressed as a percentage, providing an overview of the property's potential return. Net rental yield is a more accurate measure of profitability than gross rental yield, as it factors in annual expenses.

Property Investment Assumptions for an Australian Worked Example

For 2026, many Australian investors are still stress testing deals against elevated borrowing costs after the RBA cash rate reached 4.10% on 18 March 2026, so a cautious calculator should allow for loan rates that remain well above the old low-rate cycle (RBA cash rate target).

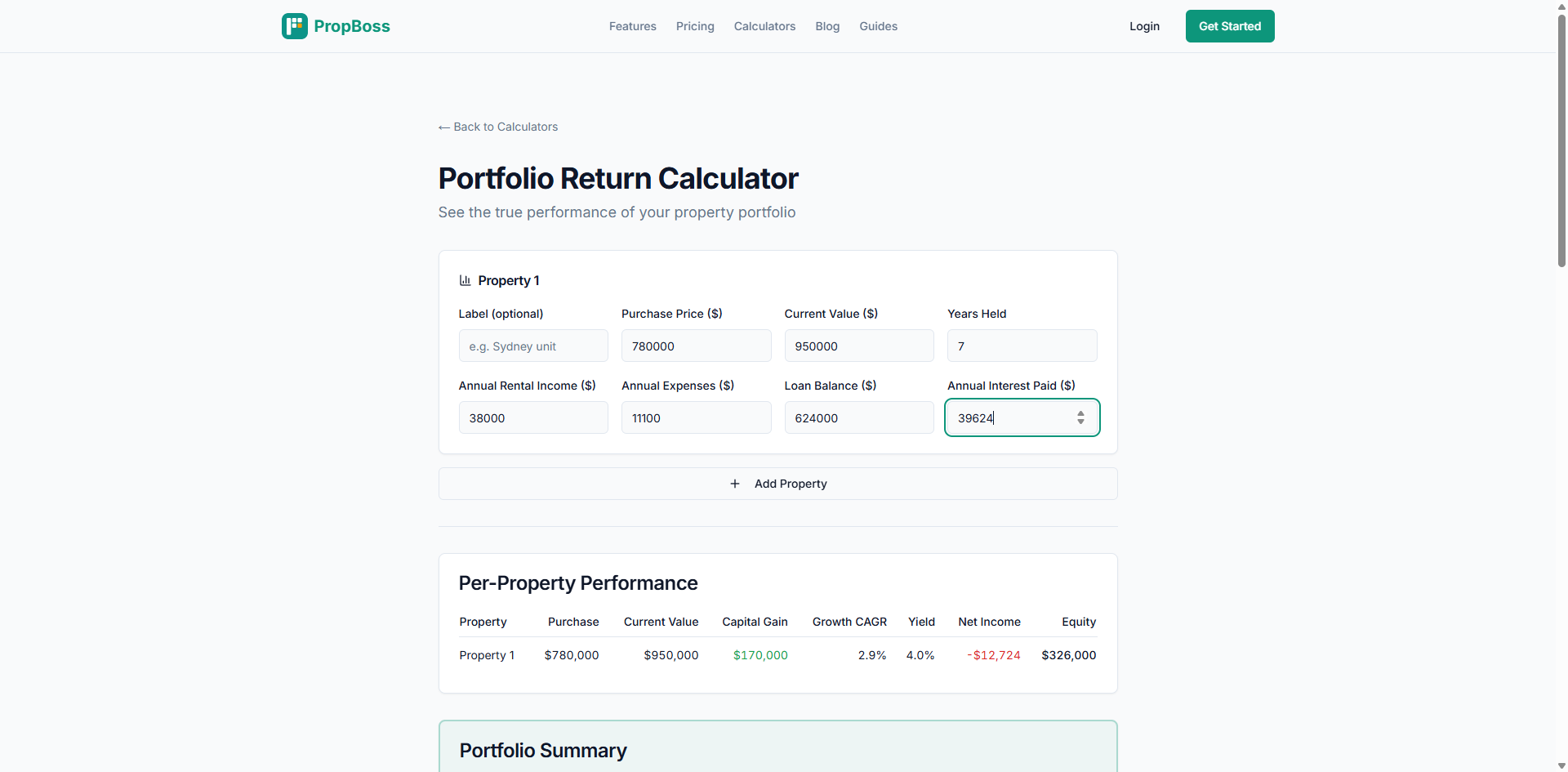

Assume an investment property in Brisbane with these inputs:

| Item | Amount |

|---|---|

| Purchase price | $780,000 |

| Deposit | $156,000 |

| Loan amount | $624,000 |

| Weekly rent | $760 |

| Vacancy allowance | 2 weeks |

| Investor loan rate | 6.35% |

| Property manager fee | 7.5% of collected rent |

| Annual repairs and maintenance | $2,400 |

| Council rates, insurance and water | $5,850 |

Weekly rent should be based on realistic market rates, not the most optimistic asking number in the suburb. Conservative calculations usually assume 2 to 3 weeks of downtime each year, while vacancy rates below 2% usually indicate stronger demand and lower non-income risk.

Collected annual rental income after two vacant weeks is about $38,000.

Property Details That Change the Result Fast

If the same investment property rents for $730 rather than $760 per week, annual rental income falls by $1,560 before vacancy.

If the purchase price rises from $780,000 to $810,000, the deposit, stamp duty, and debt also rise.

Two details are often missed. If a deposit is under 20%, Lender's Mortgage Insurance (LMI) usually applies. That premium increases acquisition costs and changes the amount of cash you need at settlement.

Investors chasing stronger growth often want a land-heavy asset because land generally drives long-term capital growth more than fixtures do. In many Australian suburbs, investors prefer a land-to-asset ratio above roughly 70% when the goal is long-run growth. Gentrification can also be a useful signal when median incomes, amenity, and buyer demand are improving in the same pocket.

Interest Rates, Loan Repayments and Interest Only Settings

Using the example above, annual interest on a $624,000 loan at 6.35% is about $39,624. If rates move to 7.10%, the annual interest bill jumps to roughly $44,304. That is an extra $4,680 a year.

Loan repayments also depend on structure. Interest-only loans often yield better short-term cash flow for investors than principal and interest loans, but the debt does not reduce during the interest only period.

Principal and interest settings usually create stronger long-term equity growth, but they increase the monthly holding cost immediately.

The calculator should let you test principal and interest versus interest only, 25-year versus 30-year terms, rate buffers of 1 to 2 percentage points, and multiple loans across more than one investment property.

Property Expenses, Cash Flow and Negative Gearing

Property expenses are where many calculators understate reality. A real investment property calculator should force you to include management, council rates, landlord insurance, water, repairs, leasing fees, and a vacancy buffer before it labels a deal "positive". Ongoing costs for investment properties typically include maintenance, property management fees, insurance, and council rates, which can significantly impact overall profitability.

Acquisition costs usually include stamp duty, legal fees, conveyancing, and building or pest inspections, and many investors budget roughly 5% of the purchase price for these buying costs.

Using the Brisbane example:

| Annual item | Amount |

|---|---|

| Collected rent | $38,000 |

| Loan interest | -$39,624 |

| Property manager fees | -$2,850 |

| Rates, insurance and water | -$5,850 |

| Repairs and maintenance | -$2,400 |

| Pre-tax cash flow | -$12,724 |

That result means the property has negative pre-tax cash flow. Negative gearing is a tax characteristic, not a performance strategy by itself.

The ATO's rental expense guidance says investors can generally claim items such as interest on loans, council rates, and repairs in the income year they incur them, while some other costs are claimed over several years.

The ATO also says investors should keep records for rental income, rental expenses, purchase documents, refinance documents, and sale costs for each property in a portfolio (ATO record keeping for rentals).

Ongoing property expenses in Australia often include council rates, water charges, strata or body corporate fees, land tax, maintenance, property management fees, and insurance.

Land tax is based on the unimproved value of land and usually rises as additional properties are added. Stamp duty and land tax rates vary significantly across Australian states and territories, so investors in NSW, Victoria, Queensland, and other markets should not assume the same holding-cost outcome.

Depreciation also matters. Depreciation deduction estimators are used for both "Plant and Equipment" and "Capital Works" to calculate non-cash deductions. Assume the owner is on a 39% marginal tax rate including Medicare levy and the full $12,724 is deductible.

The rough tax benefit is about $4,962, reducing the after-tax cash cost to about $7,762. Negative gearing may allow losses from property expenses to be deducted from taxable income, and inputting the marginal tax rate is crucial because the tax value of the loss changes by investor.

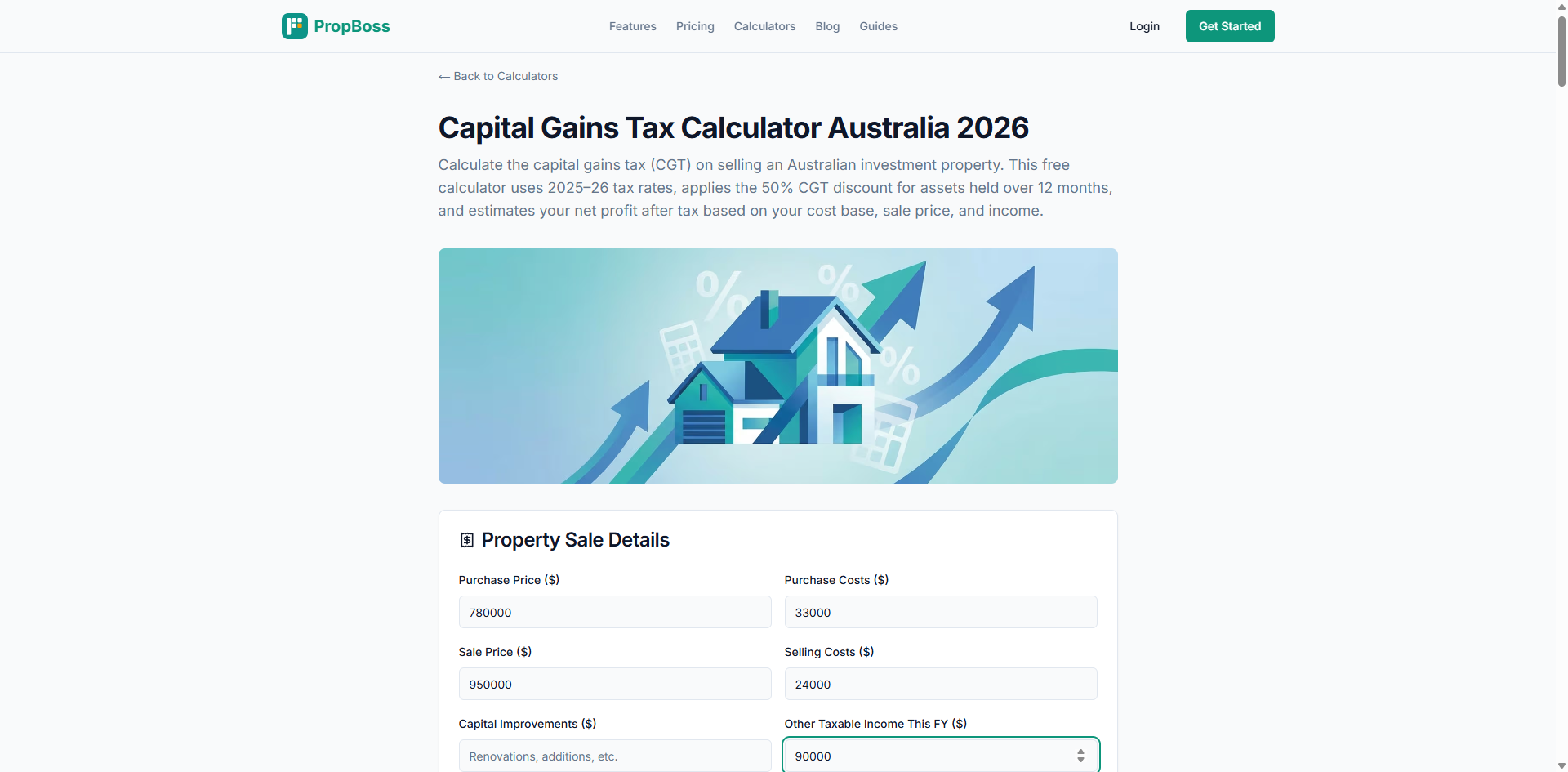

Growth Rate, Capital Gains Tax and Total Return

A calculator should allow optimistic, base, and conservative growth scenarios so you can see how much total return depends on future appreciation.

Suppose the same investment property grows from $780,000 to $950,000 over 7 years. Assume selling costs of $24,000 and buying costs of $33,000. The rough capital gain calculation looks like this:

| Item | Amount |

|---|---|

| Sale price | $950,000 |

| Less purchase price | -$780,000 |

| Less buying costs | -$33,000 |

| Less selling costs | -$24,000 |

| Estimated capital gain | $113,000 |

That is not the same as after-tax profit. Investors should consider capital gains tax (CGT) when selling an investment property, which is calculated from the profit left after deducting purchase costs and associated selling expenses, while ownership structure and the 12-month discount still matter.

Property investment ROI measures how much profit your property generates relative to the cash you've tied up in it, combining rental income, holding costs, negative gearing tax benefits, and long-term capital growth. The ROI formula includes total investment, annual net income, projected sale price, selling costs, capital gain, and total return, allowing investors to calculate their overall return on investment.

A property with a low rental yield may still deliver a strong ROI if capital growth is strong, highlighting the need to assess both income and appreciation.

Which Property Calculator Should You Use for a Portfolio

Most serious property investment decisions happen at portfolio level, so the better approach is to measure total rent, total debt and blended interest rates, property expenses by asset and by portfolio, and net cash flow before and after tax.

Gross rental yield divides annual rental income by purchase price. Net rental yield is more useful because it also reflects annual expenses.

Some investors still use the 1% rule as a quick screen, asking whether gross monthly rent is at least 1% of purchase price, but it is only a blunt filter. Gross rental yield is annual rental income divided by purchase price and expressed as a percentage.

The capitalization rate compares net operating income with market value and is only a quick comparison tool.

That is why PropBoss pushes investors toward a portfolio-level model rather than a one-line ROI calculator. If you are still designing the broader plan, read how to build a property portfolio in Australia.

Common Mistakes When Using an Investment Property Calculator

Common mistakes include using today's asking rent without a vacancy allowance, ignoring one-off buying costs when calculating return on cash invested, forgetting landlord insurance or irregular maintenance, and treating negative gearing as proof that the deal is smart.

Location assumptions matter too. Strong rental demand and lower risks of non-income periods are often associated with vacancy rates below 2%.

Properties with energy efficiency features like solar panels and good insulation are currently attracting higher tenant demand.

Investment Property Calculator Australia FAQ

What is the best investment property calculator Australia investors should use

The best investment property calculator australia investors use is one that combines rent, debt, property expenses, tax, and exit assumptions in the same model.

Can an investment property calculator show negative gearing

Yes. A proper investment property calculator should show pre-tax cash flow, deductible losses, and an estimated after-tax position so you can see whether negative gearing changes the holding cost materially.

Stop Managing Property Numbers Manually

Use the portfolio return calculator to run the numbers, then create your [owner account]( For a quick definition, see our due diligence.

Also read our buying an investment property guide. /register/owner) if you want to track the whole portfolio without relying on spreadsheets.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Investment Property ROI Calculator Australia Guide 2026

A practical Australian guide to calculating investment property ROI with rent, loan repayments, expenses, tax, growth, and selling costs.

Read more

Property Portfolio Example: 3-Property Australia Plan 2026

A worked Australian property portfolio example showing how three investment properties can be tracked, measured and stress-tested.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more