Property Portfolio Example: 3-Property Australia Plan 2026

A worked Australian property portfolio example showing how three investment properties can be tracked, measured and stress-tested.

A property portfolio example shows how multiple investment properties work together after deposits, loans, rent, costs, equity and tax records are tracked in one place. The point is to see how a portfolio can look strong on paper while still needing enough cash flow, borrowing capacity and risk controls to survive higher rates or vacancies.

Property Portfolio Example Assumptions

This example uses three Australian properties bought over several years. The investor couple has a combined income of $180,000, keeps a cash buffer, and uses principal and interest loans where possible.

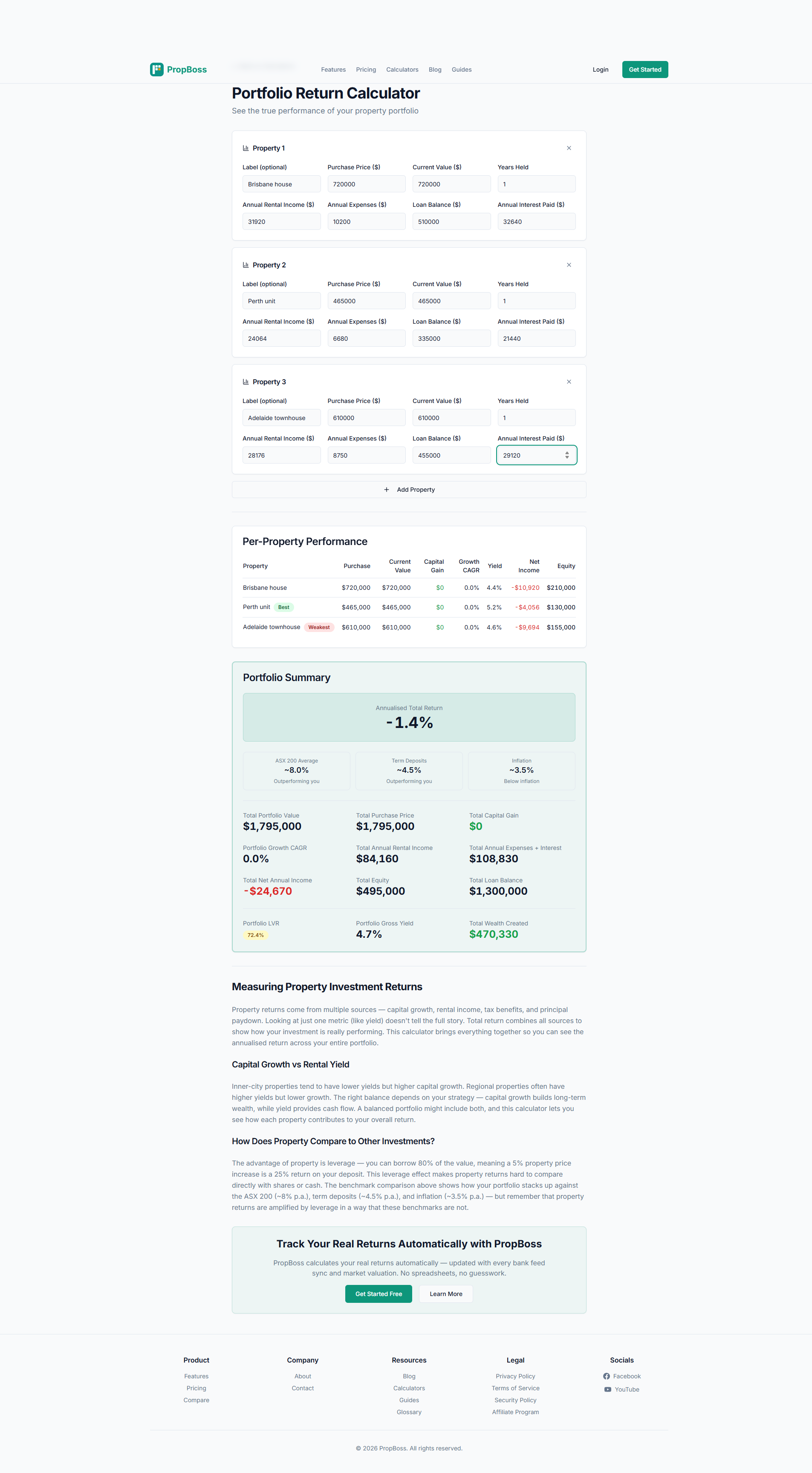

| Property | Market value | Loan | Weekly rent | Gross yield |

|---|---|---|---|---|

| Brisbane house | $720,000 | $510,000 | $690 | 5.0% |

| Perth unit | $465,000 | $335,000 | $520 | 5.8% |

| Adelaide townhouse | $610,000 | $455,000 | $610 | 5.2% |

Total market value is $1,795,000. Total debt is $1,300,000. That leaves $495,000 of gross equity before selling costs, tax and buffers.

Property Portfolio Starting Position

The first investment property was the Brisbane house. The couple used a 20% deposit and kept $25,000 in an offset account.

The Perth unit came later after capital growth lifted the Brisbane house value. The Adelaide townhouse was added only after the portfolio could handle a 1.5 percentage point rate increase.

Investment Property Loans and Equity

Equity is useful, but it is not spendable money. Lenders focus on usable equity, loan-to-value ratio, income, living costs, repayments and serviceability.

In this example, the portfolio has $495,000 gross equity. At an 80% loan-to-value ratio, $1,795,000 of property supports $1,436,000 of debt. With $1,300,000 already borrowed, the rough headroom is $136,000 before costs and lender rules.

How Much Equity Is Actually Usable?

Usable equity estimate:

| Item | Amount |

|---|---|

| 80% of total property value | $1,436,000 |

| Current loans | -$1,300,000 |

| Estimated usable equity | $136,000 |

That does not mean the couple should borrow the full amount. A conservative plan might cap usable equity at $90,000 and keep the rest as a safety margin. The portfolio return calculator helps track equity, debt, rental income and returns across the entire portfolio.

Rental Income and Cash Flow

The three properties generate $1,820 per week in rent, or about $94,640 per year before vacancies. After allowing for two weeks vacancy per property, collected rent falls to about $84,160.

Annual expenses might look like this:

| Cost | Annual estimate |

|---|---|

| Loan interest at 6.4% on $1.3m | $83,200 |

| Property manager fees | $6,730 |

| Council rates, water, strata and insurance | $12,900 |

| Repairs and maintenance | $6,000 |

| Total cash costs before tax | $108,830 |

Cash Flow Before and After Tax

This portfolio has negative pre-tax cash flow of about $24,670 per year. That does not automatically make it bad. It means the investors need high enough income, a clear tax plan and confidence that capital growth or rent increases justify the holding cost.

Where rental income is less than ongoing costs, negatively geared properties may create tax losses that offset taxable income, which is one reason they can appeal to high income investors. Check that effect with an accountant rather than assuming it from the cash shortfall.

The Australian Taxation Office says rental property owners need records for income, expenses, interest and ownership costs. Keep source documents, not only bank descriptions: https://www.ato.gov.au/individuals-and-families/investments-and-assets/property-and-land/residential-rental-properties/records-for-rental-properties-and-holiday-homes.

Capital Growth and Return on Investment

Assume the properties grow by a combined 4% in the next year. On $1,795,000 of property, that is $71,800 of paper growth. After subtracting the $24,670 cash shortfall, the before-tax portfolio result is about $47,130.

That is a simple return on investment view, not a sale calculation. It ignores selling costs and capital gains tax because the properties are still held.

Property Market Risk in This Example

The risk is concentration. All three properties rely on tenants, lenders and a stable Australian property market. If one property sits vacant for eight weeks and interest rates lift another 0.75 percentage points, cash flow can deteriorate quickly.

Diversification should be practical, not decorative. In this example, a fourth purchase should not simply be another Brisbane house unless it improves the rent, debt, land exposure or state mix of the existing portfolio.

MoneySmart notes that property investment can involve high entry costs, ongoing expenses and periods without tenants: https://moneysmart.gov.au/property-investment.

Property Manager and Operating Costs

A good property manager can protect rental income, but fees are only one operating cost. Investors also need to allow for lease renewals, compliance, landlord insurance, repairs and upgrades.

Active management means directly handling tenant screening, repairs and follow-up work. Passive management usually means hiring property managers and using the portfolio data for decisions. Either way, effective portfolio management depends on tracking rental income, expenses and each property's performance.

Here, the Perth unit has the best rental income relative to price, the Adelaide townhouse may offer stronger capital growth, and the Brisbane house gives land exposure but needs a higher cash buffer.

Investment Property Tax Records

ATO-compliant records matter because the portfolio has loan interest, rent, repairs, council rates, insurance, depreciation schedules and EOFY statements. The ATO's rental expense guidance is at https://www.ato.gov.au/individuals-and-families/investments-and-assets/property-and-land/residential-rental-properties/rental-expenses/how-to-claim-rental-expenses.

Do not wait until June. Track expenses as they happen, attach documents to each property, and separate private costs from rental costs.

Property Investment Decisions From the Numbers

The numbers suggest three decisions:

- Keep the portfolio cash buffer above $35,000.

- Use an equity calculator before considering a fourth property.

- Review the Brisbane house if cash flow remains weak after the next rent review.

The portfolio is not failing, but is not ready for expansion. The next move should be based on borrowing capacity, not fear of missing out.

How This Example Differs From a Build Plan

A build plan explains how to start. This property portfolio example explains how to monitor what has already been built.

If you are still planning, read how to build a property portfolio in Australia first. Then test this example against your income, deposit, loans and risk tolerance.

When to Add the Next Property

The fourth purchase should wait until three tests pass: the portfolio survives a 1 percentage point rate rise, the cash buffer covers three months of repayments and expenses, and the next property improves the mix rather than just adding debt.

Real Estate Portfolio Checklist

Before another purchase, define your goals, choose the location deliberately, check repayments at a higher rate, and ask your accountant how tax losses or depreciation change the result. If the numbers still work, consider whether an offset account, refinance or loan split makes the deal easier to manage.

Buy based on strategy, not pressure. A real estate portfolio should support your life, not force every decision around debt. Track the same numbers each year so you can learn from each property and avoid adding one that looks good alone but weakens the portfolio.

This example is about directly owned residential property. Real Estate Investment Trusts, or REITs, are different: they let investors own shares in larger commercial property portfolios without directly managing the properties.

To compare those portfolio results with a cleaner single-metric benchmark, read our investment property ROI calculator guide.

FAQ

What is a simple property portfolio example?

A simple property portfolio example is three properties worth $1.795 million, with $1.3 million of loans, $94,640 gross annual rent and $495,000 gross equity. Value looks healthy, but cash flow is still negative before tax.

How much equity do you need to buy another investment property?

You usually need enough equity for the deposit, purchase costs and lender buffer. In this example, 80% loan-to-value math suggests about $136,000 of possible equity headroom, but a conservative investor may use much less.

Can a property portfolio have negative cash flow?

Yes. Many investors hold negatively geared properties because they expect capital growth or future rent increases. The risk is that negative cash flow still needs to be funded every month from salary or cash reserves.

Is there a tool that does this automatically?

Yes. PropBoss tracks portfolio performance across all your investment properties with automated bank feeds, depreciation schedules and ATO-compliant reporting. It handles rental income, loan interest, cash flow and property documents so you do not need spreadsheets. Start with the owner account setup.

Stop Managing Spreadsheets

PropBoss tracks property portfolio performance across rent, expenses, cash flow, documents and returns.

Use the portfolio return calculator to test your numbers, then start a free trial from $1/property/month. For tracking the numbers behind this example, see property portfolio management software Australia. If your portfolio includes super, read SMSF property rules for investors.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Investment Property Calculator Australia Guide for 2026

A practical Australian guide to using an investment property calculator with worked numbers, tax context, and portfolio-level checks.

Read more

Investment Property ROI Calculator Australia Guide 2026

A practical Australian guide to calculating investment property ROI with rent, loan repayments, expenses, tax, growth, and selling costs.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more