Property Portfolio Management Software Australia Guide 2026

A practical guide to choosing software that tracks property data, cash flow, tax records, and portfolio performance across Australian investment properties.

Property portfolio management software helps Australian investors track rental income, costs, loan data, equity, records, and performance across every investment property in one place. The right app replaces scattered trackers with live property data, clearer portfolio visibility, and faster decisions when you are buying, refinancing, or selling.

What property portfolio management software should track

Good property management software for investors is different from software built for property managers. Property managers need tenant workflows, trust account ledgers, inspections, and maintenance requests. Investors need full visibility over the portfolio: valuation, debt, income, ownership structure, and return on investment.

At a minimum, your software should track:

- Rental income by property and by month

- Ongoing costs such as interest, council rates, strata, insurance, repairs, and property management fees

- Loan balances, repayments, and available equity

- Depreciation schedules and tax deduction categories

- Portfolio returns, growth, and risk by asset type

- Centralized data storage for rent rolls, tenant data, leases, contracts, compliance records, and documents

- Accounting and payment integration so rent collection, expenses, and financial statements can flow into one reporting process

Accounting and payment integration allows for seamless integration with accounting software to manage expenses and automate rent collection. Key features of top-tier property portfolio management software include centralized data storage, automated rent collection, performance analytics, lease management, and maintenance tracking. A centralized portfolio view provides a single dashboard to monitor all assets, including rent rolls, tenant data, and documents.

If you own residential and commercial properties, the software also needs flexible categories. A basic plan that only stores one property and a few expenses will not scale when you add another entity, refinance, or compare price points across new opportunities.

The right choice depends on portfolio size and the types of properties you manage. A one-property investor may only need simple tracking; a larger portfolio needs a centralized portfolio view, cloud-based access, scenario modelling, and reporting that can scale without extra server costs or IT maintenance.

Property portfolio: the numbers that matter

A property portfolio is not just a list of addresses. It is a set of assets, loans, cash flow lines, and tax positions that should be measured together.

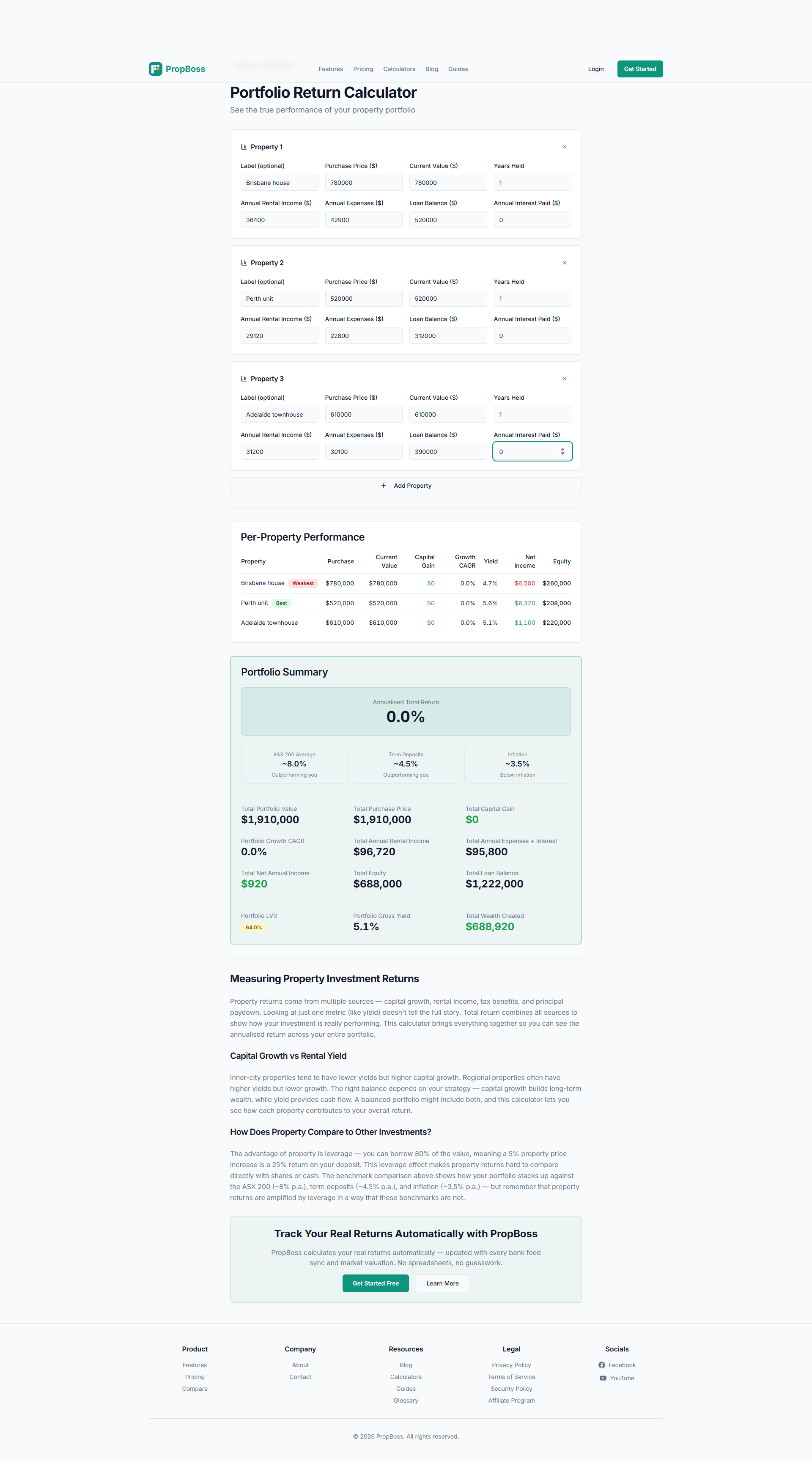

Here is a simple example for an investor with three properties:

| Property | Market value | Loan | Rent p.a. | Expenses p.a. | Net cash flow |

|---|---|---|---|---|---|

| Brisbane house | $780,000 | $520,000 | $36,400 | $42,900 | -$6,500 |

| Perth unit | $520,000 | $312,000 | $29,120 | $22,800 | $6,320 |

| Adelaide townhouse | $610,000 | $390,000 | $31,200 | $30,100 | $1,100 |

The portfolio has $1.91 million in property value, $1.222 million in debt, and $920 in annual pre-tax surplus. That headline position hides the real story: one property is carrying the other two, and a 0.75 percentage point rate increase could turn the result negative.

Use the PropBoss portfolio return calculator to model those numbers before you buy another property or change your loan structure.

Scenario modelling and forecasting tools should let you test what-if changes before they hit your bank account. For example, model a rent increase, a refinance, a vacancy, or a sale to assess the potential portfolio impact and decide whether the move still supports your return target.

Property data and asset types to compare

Your property data should let you compare asset types without rebuilding the tracker every month. Houses, units, townhouses, and commercial properties behave differently. They have different vacancy risk, growth patterns, maintenance costs, stamp duty, and finance terms.

For each asset, track:

- Purchase price, stamp duty, legal costs, and settlement costs

- Current market value and valuation date

- Gross rental yield and net cash flow

- Loan type, rate, repayment, and offset balance

- Insurance, rates, strata, repairs, and property manager fees

This is where many spreadsheets break. They can calculate a single property well, but they struggle to show which asset types are improving performance and which are increasing risk.

How much equity and risk can the portfolio carry?

How much equity you have matters, but usable equity matters more. A $1.91 million portfolio with $1.222 million of debt has $688,000 of paper equity. At an 80% loan-to-value ratio, usable equity is closer to $306,000 before lender buffers and serviceability limits.

That calculation changes as values, rates, rent, and lending policies move. If your software cannot update loan balances and market value assumptions quickly, you may make decisions from stale numbers.

PropBoss handles this automatically -- the portfolio dashboard tracks cash flow, loans, valuation, and property data across your portfolio so you can see risk before it shows up in the bank account.

Portfolio risk management

Risk mitigation starts with a clear view of debt obligations, loan-to-value ratios, and geographic exposure. Large property portfolios carry risks from rents, values, market conditions, interest rates, and personal financial situations, so the dashboard should show whether the whole portfolio remains resilient.

Review the portfolio regularly, not only at tax time. Monthly changes in rent, repayments, vacancies, insurance, and valuation assumptions can alter tolerance levels, especially if you are approaching retirement or using property income to support a financial independence plan.

Regular portfolio reviews are essential for ensuring consistent performance and keeping financial independence plans on track, with a focus on risk management and performance evaluation.

Property management features investors actually need

The best portfolio app should simplify work without turning into a second job. Look for features that reduce manual effort, streamline weekly admin, and improve confidence:

- Bank feeds that match income and expenses to each property

- Rules that categorise recurring costs consistently

- Document storage for leases, loan letters, depreciation schedules, and invoices

- Performance reporting by property, entity, and month

- Exportable tax records for your accountant

- Scenario tools for refinance, sell, hold, or buy strategies

Automation and workflow triggers

Automation matters because repetitive property management tasks are where errors usually enter the process. Good software can automate rent collection checks, expense matching, maintenance tracking, lease reminders, insurance renewals, and compliance alerts so investors and property managers spend less time chasing routine updates.

Maintenance work order management is the agency version of this workflow: requests are assigned, tracked, and completed in one system. Event-based triggers do the same job for investors by activating reminders at the right moment, such as when a fixed loan rolls off, a lease is due for review, or a document needs to be renewed. Some platforms claim routine automation can cut administrative workload by 50-75%, but the practical value is simpler: fewer missed dates, less manual entry, and lower human error.

Automating routine tasks like rent collection and maintenance tracking can reduce administrative workloads by 50-75%. Compliance and risk management features include automated alerts for safety compliance, insurance renewals, and document storage to support audits. Automating workflows in property management can significantly reduce manual effort and save time, allowing property managers to focus on more strategic tasks.

ATO record keeping

For tax, the Australian Taxation Office expects rental property owners to keep records that explain income and deductions. The ATO's rental property record keeping guidance says investors need evidence for income, interest, repairs, and other expenses. Software will not replace tax advice, but it can make those records easier to provide.

Real estate software vs investor software

Some real estate software is designed for agencies, not investors. Real estate agencies often need tenant workflows, arrears, inspections, trust accounting, and owner statements. Real estate asset teams may need leasing, facilities, and fund reporting. Those real estate tools can be useful if you manage rentals for clients, but they may be more than an investor needs.

In Australia, an investor app should help you manage properties, manage loans, manage documents, and manage reporting without agency workflows getting in the way. The goal is to optimise performance, streamline decisions, and choose strategies that fit your portfolio.

For investors, the key question is simple: does the app help you make informed decisions about your own portfolio? If the answer is no, you may be paying for features built for property managers rather than portfolio owners.

Property management software built for managers usually helps them manage residential and commercial properties on behalf of owners. That can include trust accounting, inspections, tenant communication, maintenance, lease management, automated lease renewals, portals, and reporting tools. Those features are useful in an agency, but an owner-investor should only pay for them when they directly improve portfolio visibility or reduce admin.

Integrated lease and document management offers secure storage for leases, contracts, and compliance records with automated tracking for critical dates. Automated lease and tenant management tools help manage lease start/end dates, renewals, and tenant communication via portals.

Pricing, access, and support

Compare pricing across plans by the number of properties, entities, bank feeds, and team seats you need. A software company should make support, data access, and export services clear, because hidden limits can slow reporting when your plans change.

If the product includes branded investor portals or tenant portals, check what they actually do. Investor portals can make returns, financial reports, and documents easier to share; tenant portals can handle rent payments and maintenance requests. Accurate, timely reporting improves transparency, but it should not replace the investor dashboard you use to make decisions.

Branded investor portals and accurate, timely reporting improve transparency, crucial for repeat investments and referrals. Investors can maximize returns by regularly reviewing their property portfolio to ensure consistent performance and alignment with financial goals. Effective property management strategies, including regular performance reviews and action planning, can significantly enhance overall returns on investment.

Spreadsheets, apps, and software compared

| Option | Best for | Main risk |

|---|---|---|

| Spreadsheet | One or two properties and simple tracking | Manual errors, old data, weak visibility |

| Generic accounting app | Business income and expense records | Limited property-specific performance views |

| Property manager portal | Tenant updates and owner statements | Does not show whole-of-portfolio returns |

| Investor portfolio software | Multi-property tracking, cash flow, tax, and decisions | Needs clean setup and regular data feeds |

A spreadsheet can work at the start. It becomes difficult when you add loans, offsets, repairs, depreciation, and multiple entities. That is usually when investors start losing track of what each property really contributes.

Automated reporting and analytics should produce investor-ready reports, financial statements, and performance benchmarks without manual data entry. The most useful financial dashboards show KPIs such as net operating income, internal rate of return, cash-on-cash return, and cash flow across all assets. Data-driven decision-making tools then help investors optimize performance, streamline operations, and align the portfolio with financial goals.

That is why software becomes more valuable as the portfolio grows. Once you manage more than five properties, repetitive tasks, lease dates, renewals, tenant communication, maintenance records, and reporting can create enough admin risk that automation becomes essential.

Centralized financial dashboards provide real-time visibility into key performance indicators such as NOI, IRR, and cash-on-cash return across all assets. Utilizing data-driven decision-making tools can help investors optimize performance and streamline operations across their property portfolios, leading to increased returns.

Tax, ATO records, and depreciation

Portfolio software should help you prepare cleaner records for your accountant. That means separating repairs from improvements, storing invoices, and tracking deductions by property. It should also keep depreciation visible, because a depreciation schedule can materially change after-tax results.

Depreciation and evidence

For background, see the ATO's records for rental properties and holiday homes guidance. You can also read PropBoss guides on investment property cash flow and building a property portfolio before choosing your software.

When you mention stamp duty, capital growth, and cash flow in one investment decision, you are already beyond what a basic file handles well.

If you want a worked benchmark for software-reported returns, use our investment property ROI calculator guide.

FAQ

Is property portfolio management software worth it?

It is worth it if you own more than one investment property, have multiple loans, or want better tax and performance reporting. The time saved is useful, but the bigger value is fewer errors and clearer visibility.

Is there a tool that does this automatically?

PropBoss tracks property portfolio management across all your investment properties with automated bank feeds, depreciation schedules, and ATO-compliant reporting. It handles rental income, costs, cash flow, and portfolio performance so you do not need spreadsheets. Start with PropBoss owner access.

What is the difference between property management and portfolio management?

Property management focuses on tenants, rent collection, maintenance, and inspections. Portfolio management focuses on performance, risk, cash flow, tax records, equity, and decisions across all properties.

Can software calculate return on investment?

Yes, but only if it has accurate purchase costs, current value, debt, income, expenses, and tax assumptions. Use return on investment carefully, because a high pre-tax return can look very different after interest and depreciation.

Should I use a spreadsheet or an app?

Use a spreadsheet if you have one simple property and update it every month. Use software if you want automated data, fewer manual errors, and a single view across several properties. If part of your portfolio sits inside super, review the SMSF property rules for investors before setting up your tracking workflow.

Stop managing spreadsheets

Stop managing spreadsheets. PropBoss tracks your property portfolio automatically with bank feeds, cash flow tracking, depreciation schedules, and portfolio reports from $1/property/month.

Create your account with PropBoss owner access, then use the portfolio return calculator to test your next buy, hold, refinance, or sell scenario.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Investment Property ROI Calculator Australia Guide 2026

A practical Australian guide to calculating investment property ROI with rent, loan repayments, expenses, tax, growth, and selling costs.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more