Principal and Interest Calculator: Australia Guide (2026)

A practical Australian guide to principal and interest repayments, with worked examples, investor trade-offs, and better ways to model loan decisions.

A P&I calculator helps an investor estimate repayments, mortgage repayments, and how fast a balance falls over time. It quickly shows whether a home loan still works before you buy, refinance, or change the structure.

A good calculator shows how amount, term, repayment type, and interest rate affect cash flow, repayment amounts, and total interest. It also shows how a higher interest rate or different structure can reshape the decision over the life of the loan.

For most investors, the real starting point is understanding when a principal and interest structure is stronger than interest only, then checking whether the deal still holds up when the assumptions get less generous.

What a Principal and Interest Calculator Actually Tells You

A strong home loan repayment calculator should show estimated repayments for a given amount, interest rate, term, and repayment type. It should also separate interest repayments from principal and interest repayments so borrowers can see whether their monthly repayments are reducing debt or just covering interest charged.

A useful calculator also lets you compare scenarios side by side. For a home loan investor, that means comparing home loan repayments before a purchase, refinance, or loan restructure. That matters because borrowers often choose from a headline rate alone, when cash flow, fees and charges, and the way the debt behaves over time matter just as much.

The Inputs That Change Home Loan Repayments

The biggest drivers of repayments are amount, term, interest rate, frequency, and repayment type. If one input is wrong, the estimated repayments are wrong too.

Loan Amount

Start with the actual loan amount, not the property value. If a property is worth $720,000 and the investor borrowed $576,000, the loan amount is $576,000. If the balance later falls to $548,000, the next test should use that updated amount and loan balance.

The distinction matters even more when a larger home loan pushes the deal into a different risk bucket. A bigger amount can bring a higher loan to value ratio, trigger lenders mortgage insurance, and change the effective cost before the borrower starts comparing products.

Loan Term

The term changes the repayment more than many borrowers expect. A 25-year remaining loan term produces higher home loan repayments than a fresh 30 years at the same interest rate because the principal has to be repaid faster.

That is why a refinance can change the result even when the interest rate barely moves. The debt may be the same size, but the shorter term can still increase monthly repayments.

Interest Rate

Use the actual interest rate first, then test a higher interest rate and a lower interest rate. For an investor, a practical stress test is current interest rate, current interest rate plus 1.00%, and current interest rate plus 2.00%.

That simple range does more work than a single optimistic number. It shows whether the deal survives when the interest rate moves and whether the borrower is relying on a rate that is too close to the edge.

Repayment Frequency

Repayment frequency matters because weekly, fortnightly, and monthly views change how the borrower experiences the same debt. If rent lands weekly but the loan is reviewed monthly, compare both home loan repayments and repayments so the strain is visible in the same cash-flow frame.

How Interest Calculated Daily Changes the Result

Most lenders calculate interest daily and charge it monthly. That means interest charged is highest at the start, when the balance is largest, so interest repayments take a bigger share of each repayment in the early years.

As the balance falls, less interest is charged and more of the scheduled payment goes to principal. That is why principal and interest repayments feel slow at the start, why borrowers see more interest in the first years, and why an interest only structure can look easier before the only period ends.

Worked Example: Brisbane Investment Property

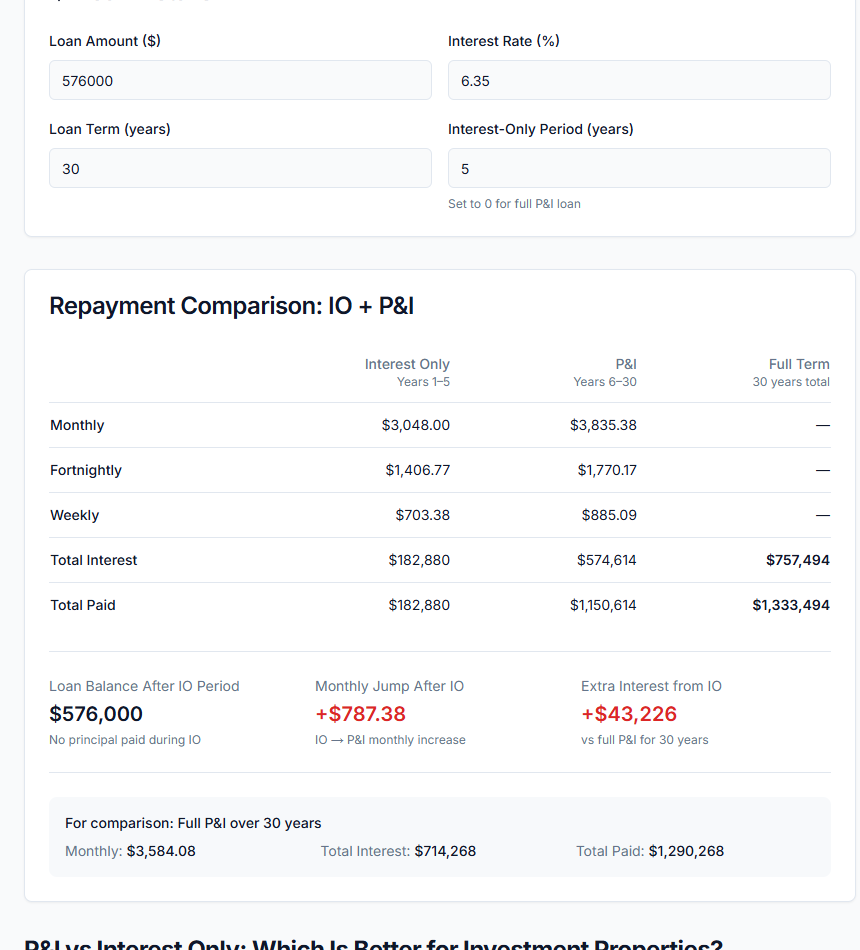

Assume an investor buys a Brisbane unit in 2026 for $720,000 and borrows $576,000 over 30 years at 6.35%. These repayment figures are based on that rate, loan amount, loan term, and repayment type only.

P&I Scenario

At those settings, monthly repayments are about $3,584, or roughly $43,009 a year. With rent at $760 a week, gross annual rent is about $39,520. The mortgage repayments do not fully cover the debt cost before strata, insurance, rates, and repairs.

That result matters because a home loan can look manageable at purchase time and still fail once the real holding costs appear. The next step is to connect those repayments to the broader property position in a cash flow calculator.

Interest Only Comparison

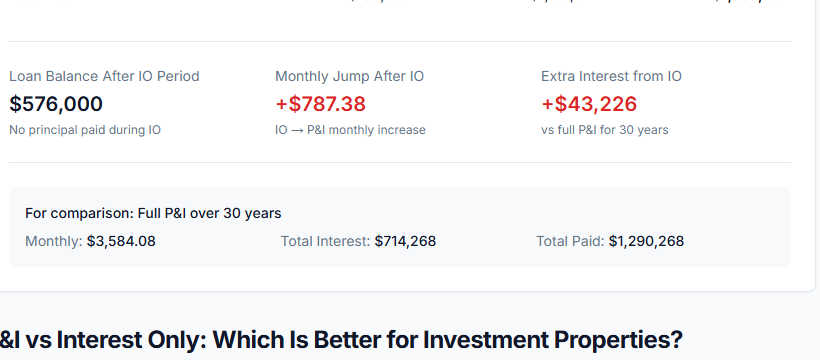

Now assume the same debt stays at 6.35% but moves to interest only for five years. During that interest only period, monthly repayments fall to roughly $3,048 because the borrower is paying interest rather than reducing principal.

Interest only loans can protect liquidity in the short term, but interest only loans also keep the balance higher for longer and create more interest over 30 years. On these settings, the monthly jump after the IO period is about $787, taking the repayment to roughly $3,835 from year 6 onward, and the IO path adds about $43,226 in extra interest versus full P&I over 30 years. That is why an apparently easier structure can create a sharper cash-flow squeeze later.

Comparison Rate, Fees, and Loan Offers

The comparison rate helps borrowers assess whether fees and charges, account fees, and the headline interest rate tell the same story. A comparison rate can be useful, but a comparison rate is true only for the standardised example used in lender disclosures, not every situation.

When you compare products, use the actual interest rate you expect to pay, then check whether the comparison rate, account fees, and other fees and charges suggest a different effective cost. That matters because rates are subject to change, while fees often stay in place regardless of the headline offer. Moneysmart mortgage guidance remains one of the clearest public references for that distinction.

This is where the fine print matters. Rates are subject to change, eligibility criteria apply before a lender issues an offer, and an Australian credit licence disclosure does not turn a calculator result into a product recommendation or formal credit approval. An Australian credit licence also does not mean the home loan has been assessed or approved for the borrower's personal circumstances.

Borrowers should remember that a calculator result is an estimate, not a commitment. The National Consumer Credit Protection Act 2009 sets the legal context, but it does not replace assessment.

Fixed Rate, Variable Rate, and Other Loan Options

A home loan repayment calculator becomes more useful when it compares loan options instead of only one number. The most common choice is between a fixed rate home loan, a variable rate home loan, or a split that combines both.

When a Fixed Rate Loan Helps

A fixed rate loan gives the borrower a fixed rate for a defined fixed rate period, which can make budgeting easier when cash flow is already tight. For an investor carrying a marginal property, a fixed rate can stabilise home loan repayments and reduce surprises.

Fixed loans are not automatically better. A fixed rate home loan can limit flexibility on extra repayments, and the length of the fixed rate period can matter more than the opening rate if the investor expects to refinance or sell within that window.

When a Variable Rate Loan Helps

A variable rate loan usually provides better flexibility for offset strategy, refinancing, and day-to-day management. If the borrower wants a loan that supports redraw, faster balance reduction, or future restructuring, a variable rate loan can be the more practical fit.

The main trade-off is that a variable rate can rise quickly, so a variable rate home loan needs stronger cash-flow resilience than a short fixed rate loan. For borrowers focused on reducing the term faster, Extra Loan Repayment Calculator: Australian Investor Guide is the closest related walkthrough. If the repayment result pushes the property toward a cash-flow loss, the negative gearing guide is the better next read for the tax-side context.

How Extra Repayments Change the Result

Making extra payments is one of the simplest ways to make a calculator useful. Instead of asking only for the minimum figure, test what happens when the borrower adds $100, $250, or $500 a month.

On the Brisbane example, extra repayments shorten the term, reduce interest charged, and cut how much interest is paid over the life of the loan. Some lenders describe them as additional repayments, but the effect is the same: the balance falls sooner and the debt can finish sooner.

That does not mean every investor should use extra repayments as the default move. If the deal still needs a stronger liquidity buffer, an offset or cash reserve may be the better choice than forcing the fastest reduction.

Calculator Output Is Not the Same as Serviceability

A home loan calculator estimates the debt cost. It does not tell you whether a lender will approve the application, whether the security property is acceptable, or whether the borrower meets the lender's eligibility criteria in practice.

What Lenders Test

Lenders assess serviceability using buffered repayments, living-expense assumptions, other debts, and often shaded rent. That is why estimated repayments can look comfortable while credit approval still fails. A borrower may also discover that approval changes once the lender checks the loan purpose, security property, and final documentation.

What Investors Should Test

Investors need a second lens beyond credit approval. The debt still has to work against vacancy, repairs, insurance, and tax treatment. ATO rental interest guidance is the right reference point because interest costs can be deductible only when the use of funds and property context line up.

A better workflow is sequential: estimate home loan repayments, compare those mortgage repayments against real property costs, then decide whether the structure still supports the wider portfolio.

Common Mistakes That Make Estimated Repayments Misleading

Most bad outcomes come from bad inputs. Before relying on the calculator, check these points:

- Use the real loan amount and current loan balance, not just the property value.

- Use the remaining term, not the original 30 years from settlement.

- Test more than one interest rate and more than one repayment type.

- Check fees and charges, package fees, and whether rates are subject to change.

- Confirm whether the structure is interest only or a model that reduces principal.

- Do not treat estimated repayments as credit approval.

How To Use a Home Loan Repayment Calculator Before You Buy or Refinance

A home loan repayment calculator is most useful when the borrower knows which decision it is supporting. Purchase analysis and refinance analysis use the same tool, but different questions.

Before a Purchase

Start with the proposed debt, the expected interest rate, and the real property costs. Then test whether the deal still works if the rate rises, if rent softens, or if a variable rate stays higher for longer.

Before a Refinance

Compare the current structure against the replacement structure on rate, term, fees and charges, and flexibility. A cheaper product can still be the weaker deal if it stretches the debt too long or removes useful features.

For a deeper look, see our how much can I borrow for an investment property. You can also read our interest only investment loan.

For investor-specific repayment examples, compare scenarios in our investment loan repayment calculator guide.

FAQ

Is P&I better than interest only for an investment property?

Not automatically. A principal and interest structure reduces debt faster, while interest only can preserve liquidity during the only period. The right answer depends on the strategy, the investor's buffer, and whether the property needs lower repayments now or stronger reduction later.

Can I use a repayment calculator for extra repayments?

Yes. A solid calculator should let you test extra repayments, additional repayments, and repayment frequency so you can compare the result before changing the structure.

What does comparison rate mean on a home loan?

The comparison rate is intended to show a broader loan cost once fees and charges are considered. It is helpful, but it is not a perfect substitute for understanding the actual interest rate, product features, and how the loan behaves in your own circumstances.

Should I use the current rate or a higher buffer?

Use both. Start with the actual interest rate, then test a higher interest rate and a variable rate scenario so the loan is not judged only on the best case.

Run Your Scenario in PropBoss

Use the PropBoss loan repayment calculator to model your home loan, compare it against interest only, and test how rate, term, and extra repayments affect the result.

If you want to connect those home loan repayments to portfolio planning instead of a one-off spreadsheet, create an account at PropBoss Owner. For current rate context, read investment property mortgage rates Australia. If broker choice affects your repayment setup, see mortgage broker for investment property.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Investment Loan Repayment Calculator: Investor Scenarios

A practical Australian guide to using an investment loan repayment calculator, with worked examples, rate-stress tests, and investor-specific decision checks.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more