Investment Loan Repayment Calculator: Investor Scenarios

A practical Australian guide to using an investment loan repayment calculator, with worked examples, rate-stress tests, and investor-specific decision checks.

An investment loan repayment calculator estimates what an Australian investment-property loan will cost each month based on your loan amount, interest rate, term, and repayment type. For investors, the useful part is not the monthly figure on its own. It is whether the debt still works after you compare principal and interest against interest only, stress-test the rate, and match the result against the property's full holding costs.

That distinction matters. A bank calculator can give you a repayment number, but it usually cannot tell you whether that repayment still makes sense for your cash flow, buffer, or next purchase. This guide focuses on the investor decision behind the number, not just the number itself.

What an investment loan repayment calculator actually tells you

Most tools use the same four inputs whether they are labelled an investment loan repayment calculator, a home loan repayment calculator, or a mortgage repayment calculator.

| Input | What it changes | Why investors care |

|---|---|---|

| Loan amount | The base repayment | Higher debt lifts both monthly cost and total interest |

| Interest rate | Monthly repayment and total interest | Small rate changes can wipe out cash-flow margin |

| Loan term | The size of each repayment | A longer term lowers repayments but increases lifetime interest |

| Repayment type | How the balance behaves | Principal and interest reduces debt; interest only protects short-term cash flow |

A calculator is useful because it turns those inputs into something concrete. If you borrow $500,000 over 30 years at 6.30%, you can estimate the monthly repayment before you buy, refinance, or restructure an existing loan. Moneysmart's mortgage calculator is a solid authority source for the mechanics, but an investor still needs to interpret the result in the context of rent, expenses, buffers, and portfolio plans.

The practical question is not just "What is my repayment?" It is "What does that repayment mean for this asset if rates move, vacancy appears, or strategy changes?"

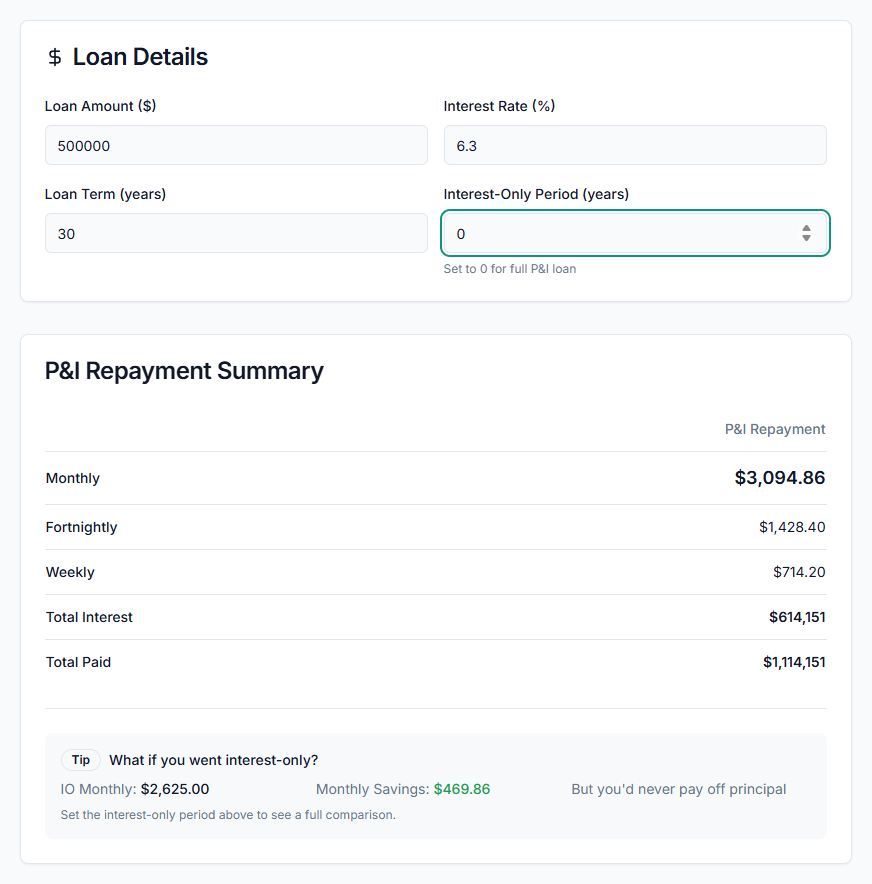

Worked example: repayments on a $500,000 investment loan over 30 years

Assume you buy a Brisbane investment property for $625,000 with a 20% deposit and borrow $500,000 over 30 years.

Here is what the repayment looks like under three common scenarios:

| Scenario | Interest rate | Repayment type | Approx monthly repayment |

|---|---|---|---|

| Base case | 6.30% | Principal and interest | $3,095 |

| Cash-flow first | 6.30% | Interest only | $2,625 |

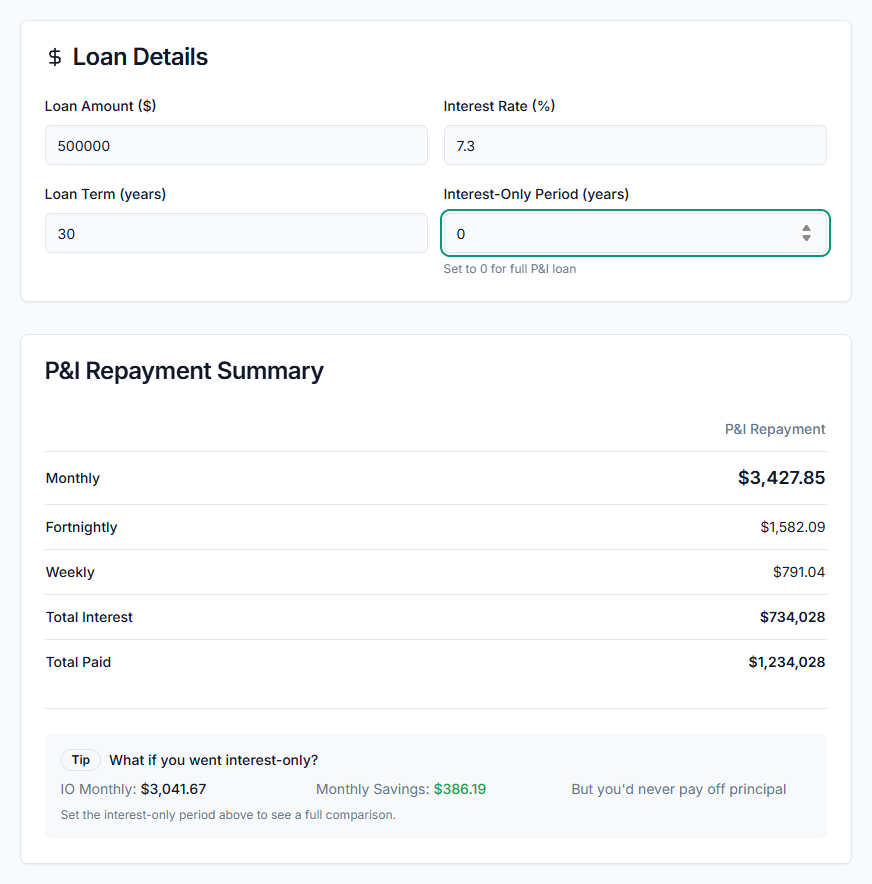

| 1% rate stress test | 7.30% | Principal and interest | $3,428 |

That single table answers two of the most common investor questions.

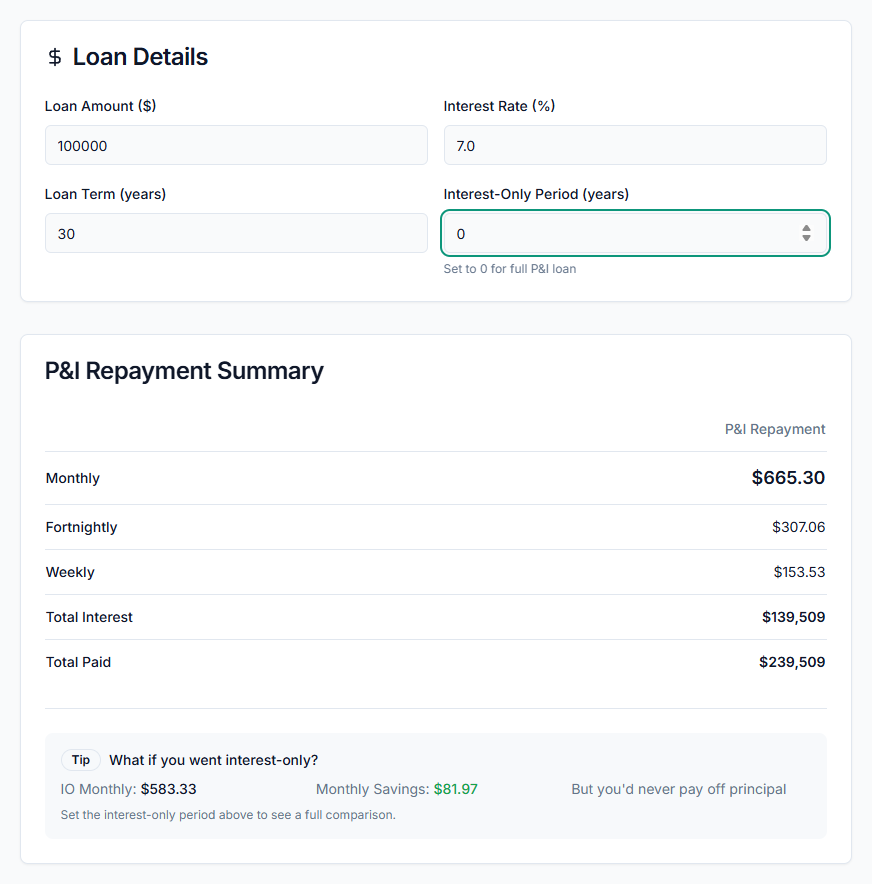

A common smaller-version question is, "How much would I pay on a $100,000 mortgage in 2026?" At 7.00% over 30 years on principal and interest, the repayment is about $665 a month.

First, what are the repayments on a $500,000 investment loan over 30 years? At 6.30% on principal and interest, the answer is about $3,095 a month.

Second, how much does a 1% rate change matter? Moving from 6.30% to 7.30% adds about $333 a month, or just under $4,000 a year, before you count insurance, council rates, maintenance, or vacancy.

One scenario is not enough. A repayment calculator becomes useful when you compare a realistic base case against a tougher rate environment.

Principal and interest vs interest only: what changes for investors?

The biggest strategic choice is usually between principal and interest and an interest only loan.

With principal and interest, each repayment covers interest plus part of the balance, so the debt reduces from the first month. With interest only, the repayment is lower during the interest-only period because you are not repaying principal, but the balance does not shrink.

| Structure | Short-term repayment | Long-term effect | Best fit |

|---|---|---|---|

| Principal and interest | Higher | Faster debt reduction, lower lifetime interest | Investors prioritising deleveraging and equity growth |

| Interest only | Lower | Higher later repayments and more total interest if held long enough | Investors prioritising short-term cash flow and liquidity |

Neither structure is automatically better. If your cash flow is tight and you want more buffer, interest only can protect breathing room. If you want to reduce debt faster and build equity sooner, principal and interest is usually the cleaner long-term option.

The trap is assuming the lower interest-only repayment means the deal is healthier. Often it just means the pressure has been deferred. The ATO explains in its interest expenses guidance for rental properties that interest may be deductible when the borrowing is used for an income-producing property, but the tax position does not change the fact that the loan still has to be serviced.

How much does a 1% interest-rate change affect repayments?

For most investors, rate sensitivity matters more than the starting repayment.

Here is the same comparison on two loan sizes:

| Loan size | 6.30% P&I | 7.30% P&I | Monthly increase |

|---|---|---|---|

| $500,000 | $3,095 | $3,428 | $333 |

| $700,000 | $4,333 | $4,799 | $466 |

This is where fixed-versus-variable and refinance decisions start to matter. A one-point rate move sounds small in percentage terms, but at investor loan sizes it quickly becomes a real monthly cash-flow problem.

If a property only works at today's rate, the deal is fragile. A better test is to run the calculator at the likely starting rate, then at 0.50% and 1.00% above that rate. If the holding costs become uncomfortable under the stressed version, the purchase or loan structure probably needs to change.

This is also where investors should think beyond the loan itself. If the repayment still works after a rate rise but the full property does not, the real issue may be operating cash flow rather than the mortgage alone. In that case, pair the repayment estimate with the cash-flow calculator instead of treating the debt number as the whole story.

A repayment calculator is not the same as borrowing power or serviceability

A repayment calculator answers, "What would this loan cost each month?" It does not answer, "Will a lender approve this loan?"

That second question is a serviceability question. Lenders assess serviceability using income, existing debts, shaded rental income, living expenses, and policy buffers above the note rate. So when someone asks, "How much do you need to earn for a $700,000 mortgage?", they are really asking about lender assessment, not just repayment size.

If you are asking how much money you need to make before buying a house, there is no universal income number. Lenders combine salary, other income, shaded rent, existing debts, living costs, and serviceability buffers rather than relying on a single repayment figure.

This distinction matters because a calculator can show a repayment that looks manageable in your own budget while a lender still says no. The reverse can also happen. You may technically qualify, but the repayment leaves too little monthly buffer once you include real-world investor costs.

That is one reason disclosure and lending context matter. In Australia, responsible lending and disclosure sit inside the framework of the National Consumer Credit Protection Act 2009. A calculator is still only a scenario tool. You need to read the product terms, understand the comparison rate, and check whether the structure still works once the lender's assessment assumptions are applied.

How to interpret the result before you buy or refinance

Once the calculator gives you a number, the next job is calculator output explanation: turning the result into a decision about cash flow, buffers, loan structure, and timing.

- Test the base scenario using the likely loan amount, term, and rate that match the product you are actually considering.

- Re-run the same loan 0.50% to 1.00% higher. If the repayment jump breaks the deal, you need more margin.

- Compare principal and interest beside interest only. A lower repayment is only useful if it improves the whole investment decision, not just the first year.

- Check the full property cash flow, not just the mortgage line. Rates, insurance, maintenance, and vacancy still exist even if the loan looks manageable.

- Decide what the next move is. If the rate is the problem, refinancing may matter. If liquidity matters more, offset strategy may matter. If the deal barely works even after stress testing, walking away may be the right call.

When rates or structure are the issue, the next useful read is Refinance Investment Property Loan: Should You Switch in 2026?. When flexibility matters more than direct debt reduction, Offset Accounts for Investment Properties: How Much Interest Can You Actually Save? is the better comparison.

Common mistakes investors make with repayment calculators

The most common errors are simple:

- using the purchase price instead of the actual loan amount

- forgetting that interest-only repayments jump when the interest-only period ends

- comparing headline rates instead of comparison rates

- assuming extra repayments are always sustainable

- treating the repayment estimate as a proxy for borrowing power

This guide is also not a substitute for a car loan, personal loan, or construction loan calculator. Those products have different repayment structures, fees, and approval rules, so the right answer starts with the right calculator.

Another common mistake is copying lender marketing language into your own decision. A glossy bank tool might show a neat monthly number, but it does not know your vacancy buffer, your renovation budget, or whether you are trying to preserve borrowing capacity for the next purchase.

A better habit is to use the calculator as a decision aid. Estimate the repayment, stress the downside, then compare that result against the full property economics rather than trying to force the numbers to work.

FAQ

What are the repayments on a $500,000 investment loan over 30 years?

At 6.30% on principal and interest over 30 years, the repayment is about $3,095 a month. At the same rate on interest only, the monthly cost is about $2,625, but the balance does not reduce during the interest-only period.

How much does a 1% interest-rate change affect investment-loan repayments?

On a $500,000 loan over 30 years, moving from 6.30% to 7.30% adds about $333 a month. On a $700,000 loan, the same 1% rise adds about $466 a month. That is why rate-stress testing matters before you commit.

Is an investment loan worth it if the repayment estimate is tight?

Usually not without more testing. If the repayment only works under a best-case rate or rent assumption, the property is too fragile. A sound investment loan should still look acceptable after a realistic rate stress and a full cash-flow check.

Is a repayment calculator the same as a borrowing-power or serviceability calculator?

No. A repayment calculator estimates loan cost. Borrowing power and serviceability tools estimate what a lender may approve. Investors need both, because affordability and approval are related but not identical.

What changes when you switch from principal and interest to interest-only repayments?

The monthly repayment falls, which can help short-term cash flow, but the balance does not reduce during the interest-only period. When that period ends, repayments usually jump because the remaining principal has to be repaid over a shorter timeframe.

Run the scenario before you commit

If you want the clean repayment number first, use the PropBoss loan repayment calculator. If you want to compare that result against the rest of your portfolio and your next purchase decision, create a free PropBoss owner account before you commit.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Principal and Interest Calculator: Australia Guide (2026)

A practical Australian guide to principal and interest repayments, with worked examples, investor trade-offs, and better ways to model loan decisions.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more