Refinance an Investment Property to Pay Off Your Home Loan: 7 Checks

A practical Australian guide to using an investment-property refinance to reduce a home loan, including mixed-purpose borrowing, tax traps, and a worked example.

Yes, you can refinance an investment property to help pay down your home loan, but the interest on the part used for your primary residence is usually private rather than deductible. That is the part many Australian investors miss: the security property matters less than the purpose of the new borrowed funds. If the refinance simply replaces existing rental-property debt, the tax treatment is usually cleaner. If you cash out to reduce your PPOR loan, the structure needs much more care.

This guide is for investors who want a straight answer before changing lenders, redrawing funds, or shifting debt around. It focuses on cash flow, deductibility, and the evidence you need if you go ahead.

The short answer: when this strategy works and when it goes wrong

This strategy can work as a cash-flow move. If you refinance the investment loan, pull out extra funds, and reduce your owner-occupied mortgage, your total monthly outgoings may fall.

The tax problem is different. The ATO's Interest expenses guidance says deductibility follows the use of the borrowed money. If the extra debt is used to pay down your home loan, that portion usually becomes private. It does not stay deductible just because the loan is secured by a rental property.

That means the real decision is not "Can I do it?" The real decision is "Do the cash-flow and flexibility benefits still stack up once I separate the deductible and non-deductible parts correctly?"

If you are still deciding whether refinancing is worthwhile at all, the broader companion read is Should You Refinance Your Investment Property Loan?.

Refinance vs redraw vs equity release: do not treat them as the same thing

Readers often use these terms interchangeably, but they create different records and different tax headaches.

| Structure | What is happening | Main risk in this scenario |

|---|---|---|

| Refinance | You replace the existing loan with a new loan, often with a new lender | The replacement debt may be clean, but any extra amount used for private purposes usually needs separate treatment |

| Redraw | You pull back amounts that were already repaid into the loan | Redrawn amounts used privately can contaminate deductibility quickly if the account is not split clearly |

| Equity release / cash-out | You borrow additional funds against available equity | The extra debt may improve cash flow elsewhere, but the purpose of that extra borrowing controls deductibility |

In practice, the safest structure is usually a clean split. One split replaces the original investment debt. A second split holds the private-purpose amount used to reduce the home loan. That does not make the private split deductible, but it does make the record-keeping defensible.

The ATO's Apportioning rental interest expenses guidance is useful here because it reinforces the ongoing need to apportion when a rental-property loan is used for another purpose.

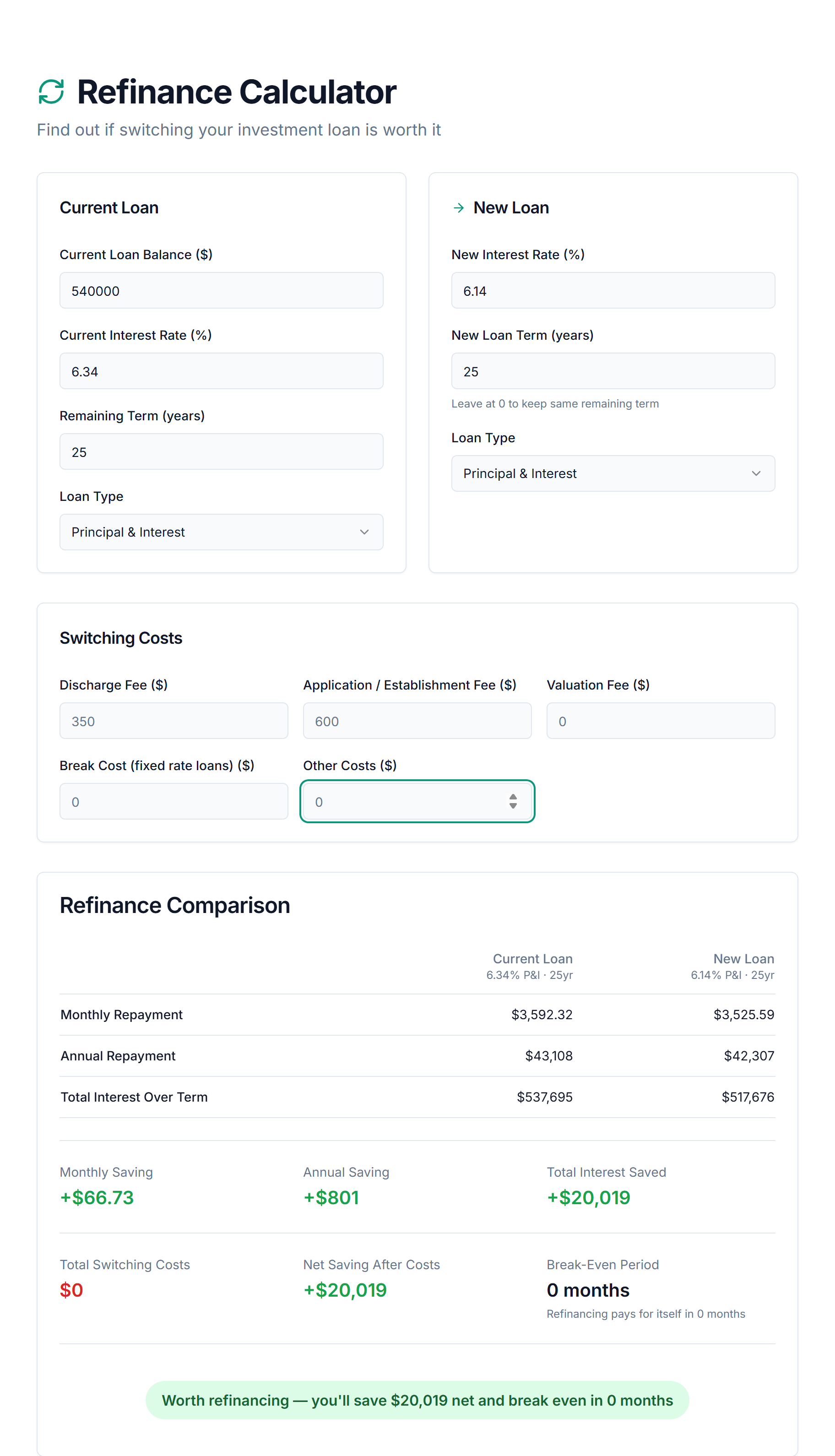

Worked example: a refinance that helps cash flow but weakens deductibility

Assume an investor has:

- an investment-property loan balance of $540,000 at 6.34% with 25 years remaining

- a home loan balance of $310,000 at 6.04% with 25 years remaining

- enough usable equity to refinance the rental-property loan up to $600,000

The investor refinances the rental-property loan to $600,000 at 6.14% and uses the extra $60,000 to reduce the home loan.

| Loan position | Before refinance | After refinance |

|---|---|---|

| Investment loan balance | $540,000 | $600,000 |

| Investment loan monthly repayment | $3,592 | $3,917 |

| Home loan balance | $310,000 | $250,000 |

| Home loan monthly repayment | $2,005 | $1,617 |

| Combined monthly outflow | $5,597 | $5,534 |

At first glance, the investor is ahead: combined monthly outflow drops by about $63 a month. But the refinance did not create a free deduction.

Because $60,000 of the new $600,000 facility was used to reduce the home loan, 10% of the refinanced debt is now private. On a rough first-year interest cost of about $36,840, that means around $3,684 relates to the private portion and around $33,156 relates to the investment-purpose portion.

That is the key decision-rule insight. The strategy can improve household cash flow and still reduce the deductible share of the investment loan. Whether it is worth doing depends on the trade-off between:

- slightly lower total monthly outflow

- the loss of deductibility on the private-purpose portion

- the administrative effort of keeping the loan purpose traceable

Now compare that with a like-for-like refinance only. If the investor refinanced the original $540,000 balance at 6.14% on the same remaining term, the monthly repayment would be about $3,526. That is a cleaner saving of roughly $67 a month on the investment loan itself, with no new private-purpose contamination.

When interest usually stays deductible and when it usually does not

| Scenario | Likely outcome | Why |

|---|---|---|

| New loan only replaces the old investment-property balance | Usually deductible | The purpose of the debt is still the income-producing property |

| Extra borrowing funds repairs, deductible costs, or approved investment use on the rental property | Often deductible, subject to the facts | The borrowed money still supports the income-producing asset |

| Extra borrowing pays down a PPOR or funds private spending | Usually private, not deductible | The new borrowing is now serving a private purpose |

| One blended account is used for both investment and private purposes | Apportionment required | You need to split or trace the use of funds over time |

| Redraw from the rental-property loan is later used for private spending | Private portion usually loses deductibility | The use of the redrawn amount controls the tax result |

The ATO's rental-property guidance also separates loan interest from borrowing expenses. Application fees, valuations, and lender charges do not always get claimed in the same way as ordinary interest. Some borrowing expenses are spread over time rather than claimed immediately.

If you mention capital gains tax in this scenario, keep it narrow. Refinancing by itself is not usually the CGT event. CGT usually becomes relevant later if ownership changes, the property is sold, or cost-base evidence matters.

The 7 checks before you switch

-

Check the purpose of every new dollar borrowed. If the extra funds reduce your home loan, treat that portion as private from day one. Do not assume the whole refinanced balance remains deductible.

-

Split the debt instead of blending it. If possible, keep the investment replacement debt separate from the private-purpose debt. A split loan is easier to explain to your accountant and easier to defend if the ATO ever asks.

-

Hold the remaining term constant before judging the saving. A refinance often looks better when the term resets. Compare the current loan and the new loan on the same remaining term first.

-

Re-test the household cash flow, not just the investment loan. Your rental-property repayment might rise while your home-loan repayment falls. The relevant number is the combined effect across both loans.

-

Compare principal and interest against interest only on purpose, not by habit. Interest only may help short-term cash flow, but it can leave the balance high and make the long-run PPOR payoff strategy weaker.

-

Include fees, break costs, and loan features. Do not ignore package fees, discharge fees, valuation costs, or the value of an offset feature. If cash access matters, the offset trade-off may be more important than the headline rate. This is where Offset Accounts for Investment Properties is a better next read than another rates article.

-

Plan the evidence before settlement. Keep the refinance proposal, split-loan documents, settlement statement, and a clear trail showing where the extra funds went. The structure is only as good as the records behind it.

Is P&I or interest only better for this strategy?

There is no universal winner. For this specific strategy, P&I is usually cleaner if your real goal is to reduce debt over time. Interest only can help short-term cash flow, but it often preserves the balance and pushes the harder repayment problem into the future.

Use the loan repayment calculator alongside the refinance decision when you are comparing repayment types. That gives you a cleaner view of whether the strategy is helping you reduce debt, protect buffers, or simply move the pressure somewhere else.

For many investors, the better question is which structure leaves the best balance between deductible debt, private debt reduction, and portfolio cash flow over the next two to five years.

When a separate split or a different strategy is better

Sometimes refinancing the investment property to reduce the home loan is not the best move at all.

Some "pay your house off fast" content sells this as using chunks of equity from investment properties. One advantage of paying off investment-property debt, or paying off debt in general, is the added equity it can provide, but home buyers employ a variety of strategies to pay off their home loans quicker, and refinance is only one of them.

If the refinance only improves combined cash flow by a few dollars a week, the record-keeping burden may not be worth it. Once you have built up enough equity, you can look to access it through refinancing and increasing the amount you owe on the investment property, or by using home equity to invest or buy your next home, but those are different decisions from reducing a PPOR loan.

Some forum threads reduce this to "refinance investment, withdraw equity, and buy a primary residence" or use the equity in your existing property as 100% of the 20% deposit through a cross-tied mortgage. Slow down if that is the pitch. Selling the investment property, leaving the loan untouched, or using a cleaner home-loan strategy may be better.

That is where the PropBoss angle becomes genuinely useful. The refinance calculator is not just there to produce a monthly repayment. It helps you compare the old and new structure, then test how the change affects broader portfolio cash flow before you sign anything.

What records to keep for the ATO after refinancing

If you go ahead, keep more than the bank statement.

- refinance approval and credit proposal

- settlement statement and discharge letter

- loan split schedule showing investment and private-purpose portions

- invoices for any rental-property repairs or improvements funded from the refinance

- evidence of where the cash-out amount was transferred

- accountant notes on how the interest should be apportioned from the settlement date

Once the loan purpose changes, the quality of your evidence becomes part of the tax outcome. That is one reason PropBoss can help after the refinance: tracking loan changes, cash flow, and supporting records is easier when they sit in one operating system instead of scattered spreadsheets and email threads.

FAQ

Can you refinance an investment property to pay off your primary residence?

Yes. Lenders may allow it, and the household cash-flow result can improve. But the part of the new borrowing used to reduce your home loan is usually private rather than deductible.

Is the interest still tax deductible if you use the refinance to pay down your home loan?

Usually only on the part that still relates to the income-producing property. The private-purpose portion used for the home loan generally does not stay deductible.

What is the difference between redraw, refinance, and equity release in this scenario?

Refinance replaces the old loan, redraw pulls back amounts already repaid, and equity release or cash-out borrows above the old balance. In all three cases, the use of the funds controls deductibility.

Can you use equity from an investment property to pay off a mortgage?

Yes, but using equity this way does not make the resulting interest deductible by itself. It can still be a sensible cash-flow move, but it needs to be tested on both cash flow and tax outcome.

Should you sell the investment property instead of refinancing it to reduce your home loan?

Sometimes that is the cleaner option, especially if the refinance savings are weak, the record-keeping would be messy, or the property no longer fits your strategy. The right answer depends on tax, selling costs, cash flow, and what the property is doing inside the portfolio.

What records do you need to keep for the ATO after refinancing?

Keep the refinance paperwork, split-loan records, settlement documents, proof of where the borrowed funds went, and supporting invoices or accountant notes. If the facility serves both investment and private purposes, the evidence trail matters.

Is this the same as using refinance to buy multiple investment properties?

No. This guide is not about how to buy multiple investment properties. It is about whether one existing investment-property refinance should be used to pay off a primary residence loan.

Model it before you change the loan

Use the PropBoss refinance calculator to test the rate change, keep the term honest, and compare the combined effect across your investment loan and home loan before you switch.

If you want to track the post-refinance cash-flow effect, compare loan structures, and keep the evidence in one place, create an account at PropBoss Owner.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more