Offset Account Interest Rate in Australia: Full Guide 2026

Australian guide to offset account interest rates: compare loan pricing, package fees, break-even maths, tax issues and refinance decisions.

An offset account usually does not have its own earnings rate in Australia. What matters is the interest rate on the linked home loan, plus any package or monthly fee, because those costs determine whether the offset feature actually saves you money.

Borrowers search for an "offset account interest rate" as if the account itself pays a special return. In practice, the real question is whether an offset-enabled loan leaves you better off than a cheaper loan without offset, extra repayments, or a savings account.

If you want to model your own numbers before changing lenders, start with the PropBoss offset calculator.

What Does "Offset Account Interest Rate" Actually Mean?

An offset account is a transaction account linked to a home loan. Instead of paying deposit interest on the cash balance, the lender reduces the loan balance used to calculate interest. In practical terms, offset accounts typically offer 0% interest earned on the balance and create value by lowering the mortgage interest charged instead.

That means the "offset account interest rate" is really shorthand for three moving parts:

- the interest rate on the linked home loan

- any monthly fee or annual package fee attached to the offset feature

- the average amount of money in your offset

The regulator guidance is clear on the mechanics. Moneysmart explains that interest on most home loans is calculated daily and your lender subtracts the offset balance from the loan balance before working out that day's interest.

So if you owe $620,000 and keep $45,000 in offset, you pay interest on roughly $575,000, not the full $620,000. The higher the home loan interest rate, the more valuable each dollar in offset becomes.

How a Home Loan Offset Changes the Interest You Pay

The easiest way to think about offset is that it reduces the interest you pay without locking your cash inside the loan.

That is different from making extra repayments directly into the mortgage. With extra repayments, the loan balance falls. With offset, the loan balance stays the same, but the bank charges interest on a smaller net balance.

Money in Your Offset Reduces the Interest You Pay

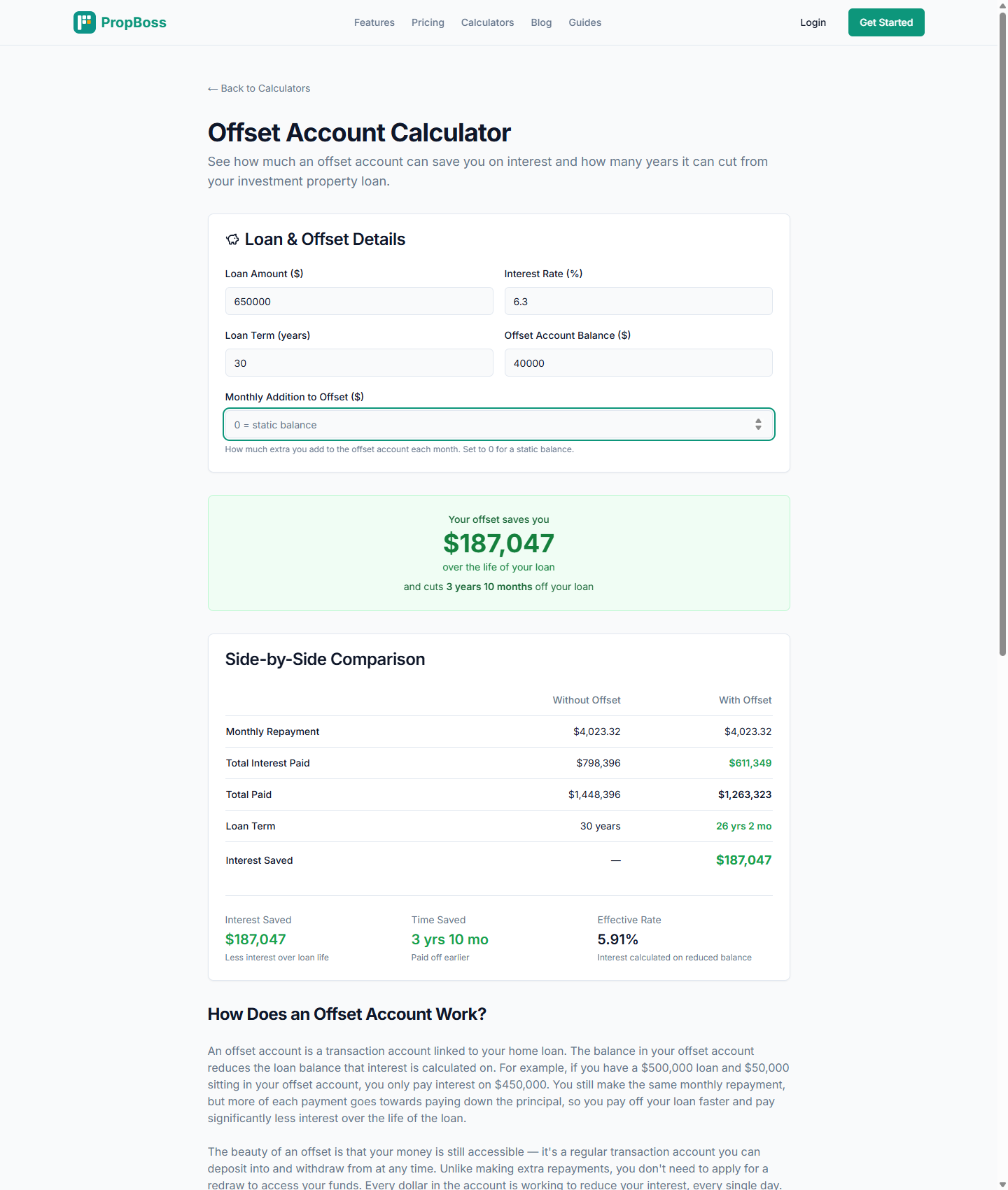

Assume an owner-occupier or investor has:

| Item | Amount |

|---|---|

| Loan balance | $650,000 |

| Home loan interest rate | 6.30% p.a. |

| Average offset balance | $40,000 |

Approximate annual interest saving:

$40,000 x 6.30% = $2,520

Using the same numbers in the live PropBoss offset calculator, a $650,000 loan at 6.30% with a static $40,000 offset balance over 30 years shows about $187,047 less interest paid over the loan life and the loan finishing roughly 3 years 10 months earlier.

That is why offset can outperform a normal savings account even though the account itself pays no deposit interest. The effective benefit comes from avoiding mortgage interest at the loan rate.

Why the Home Loan Interest Rate Matters More Than Deposit Interest

If a savings account pays 4.75% and your home loan costs 6.30%, the gross offset benefit is usually stronger before tax is even considered.

The gap can widen further because savings-account interest is taxable, while the interest you avoid paying on a home loan is not treated as bank interest income. In other words, the effective return from an offset account is often higher and more tax-efficient than a regular savings account. That is one reason offset remains popular with higher-income borrowers, investors with large cash buffers, and households that keep salary and emergency funds in one account.

Current Home Loan Interest Rate Examples for Offset Borrowers

Check the lender page on the day you apply, because rates and discounts move. Current examples show why "offset account interest rate" is really loan pricing plus feature pricing.

Published Investment Rate Examples

As of 24 April 2026, CommBank's published Simple Home Loan investment principal and interest rates ranged from 6.29% at 60% or below LVR to 6.44% at 70.01% to 80% LVR, with rates effective 27 March 2026. The page also confirms offset-linked accounts on eligible loans. Source: CommBank Simple Home Loan.

ANZ's public Standard Variable home loan page states that eligible borrowers can add an ANZ One Offset account and that a $10 monthly fee applies. ANZ also notes that higher discounts may apply when your loan-to-value ratio is 80% or less. Source: ANZ Standard Variable Home Loan.

That creates the real comparison problem:

- a cheaper basic variable loan with no offset

- a slightly dearer variable loan with offset

- a packaged loan with offset plus a monthly fee or annual package cost

The correct question is not "Which offset account has the best rate?" It is "Does the offset feature leave me paying less total interest and fees over the period I expect to hold the loan?"

Why Loan-to-Value Ratio Still Changes Offset Pricing

Even when two lenders both offer offset, the price can shift materially with your loan-to-value ratio. Borrowers at 60% LVR often get sharper variable pricing than borrowers at 80% or 90% LVR, which means the same offset strategy can look excellent for one borrower and ordinary for another.

Monthly Fee and Rate Premium: When Does Offset Still Win?

Offset is not automatically worth paying for. Moneysmart specifically warns that some lenders charge higher interest rates, annual package fees, and monthly account fees for offset-eligible loans.

Here is a simple break-even example using an investment property borrower:

| Scenario | No Offset Loan | Offset Loan |

|---|---|---|

| Loan balance | $650,000 | $650,000 |

| Interest rate | 6.10% | 6.30% |

| Average money in offset | $0 | $40,000 |

| Monthly offset fee | $0 | $10 |

Annual cost of the higher rate:

$650,000 x 0.20% = $1,300

Annual benefit from the offset balance:

$40,000 x 6.30% = $2,520

Less annual fee:

$10 x 12 = $120

Estimated net benefit of choosing the offset loan:

$2,520 - $1,300 - $120 = $1,100

In that example, offset still wins. But if your average balance is only $10,000, the gross benefit falls to about $630 a year, and the same rate premium plus fee would leave you behind.

That is why small balances and expensive packages are a bad combination. A borrower who rarely keeps money in the account may be paying offset pricing for no real outcome.

Extra Repayments vs Offset: Which Saves More?

From a pure interest perspective, $20,000 sitting in offset and $20,000 paid directly off the loan often create a similar short-term saving. The major difference is flexibility.

With offset, the cash remains accessible. With extra repayments, the money has gone into the loan and future access depends on redraw rules.

Extra Repayments Can Be Fine for Stable Owner-Occupier Debt

If you have a stable income, no need for a large cash reserve, and no tax complexity, extra repayments can be perfectly sensible. They reduce the loan balance and can shorten the term fast.

For borrowers focused mainly on the repayment schedule, the loan repayment calculator is the right companion tool.

Investment Property Loans, Redraw and the ATO

For investors, the tax difference between offset and redraw matters more. The ATO interest expenses guidance says interest must be apportioned when part of a loan is used for private purposes, including after a redraw.

That is why many property investors prefer keeping surplus cash in offset instead of paying it into the loan and redrawing later for personal spending. While both offset and redraw can reduce interest, an offset account provides more immediate access to funds, while redraw facilities may come with lender-specific withdrawal rules, delays, or minimum redraw amounts. The offset approach generally preserves access to the cash without contaminating the investment loan in the same way a mixed redraw can.

If you are restructuring debt, selling, or considering a lender switch, read our guide on refinancing and the deeper article on Should You Refinance Your Investment Property Loan?.

Credit Card Strategy: Why It Can Increase Offset Savings

Moneysmart also notes that some borrowers use a credit card alongside offset so more cash stays in the offset account for longer, then pay the card in full by the due date.

Used carefully, that can improve the average daily offset balance. For example:

- salary lands in offset on the first of the month

- daily spending goes through a credit card

- the card is repaid in full before interest is charged

That keeps more money in your offset for more days, which increases the interest savings. Having your salary paid directly into the offset account can maximize interest savings because home loan interest is calculated daily on the net balance after offset. The strategy only works if the card is cleared on time every month. If you carry a high-interest credit card balance, the card debt will usually cost far more than the mortgage interest you are saving.

Fixed Rate, Variable Rate Home Loans and Partial Offset

Most offset products in Australia are attached to variable rate home loans. Some lenders offer partial offset or limited offset functionality on selected fixed products, but you should never assume the feature is full or free.

Check:

- whether the loan is variable, fixed, or split

- whether the offset is 100% or partial

- how many linked transaction accounts are allowed

- whether the offset applies to the whole loan or only a variable split

- whether a monthly fee or annual package fee applies

If you are weighing principal and interest against interest-only repayments on an investment loan, the offset benefit can still be valuable in either structure. The main issue is not just repayment type. It is whether the loan product and your cash habits produce net savings after fees.

Multiple offset accounts can help with budgeting, tax reserves, and bill separation, but they do not create extra savings by themselves. The savings come from the combined average balance sitting against the loan, not from the number of linked accounts.

For broader strategy examples, see Offset Accounts for Investment Properties: How Much Interest Can You Actually Save?.

How Much Money in Your Offset Do You Need to Break Even?

You can estimate a rough break-even offset balance with this formula:

(annual fee + annual cost of higher rate) / loan rate

Example:

| Item | Amount |

|---|---|

| Loan balance | $700,000 |

| Extra rate for offset product | 0.15% |

| Annual package cost | $395 |

| Home loan rate | 6.20% |

Step 1: annual cost of higher rate

$700,000 x 0.15% = $1,050

Step 2: total annual offset cost

$1,050 + $395 = $1,445

Step 3: break-even offset balance

$1,445 / 6.20% = about $23,306

So if your average offset balance is meaningfully above $23,000, the offset loan may be worth it. If it is well below that level, you may be paying for a feature you are not really using.

How to Compare Offset Offers Before You Apply

Before choosing an offset loan, compare these items side by side:

- actual interest rate, not just marketing copy

- comparison rate and what fees it captures

- monthly fee or annual package fee

- full offset or partial offset

- number of linked accounts allowed

- redraw rules and access restrictions

- whether the lender prices investment loans above owner-occupier loans

- whether the loan still works for future borrowing capacity

For investors, also check whether the lender's policy supports later debt recycling, split loans, and clean record keeping. A slightly lower advertised rate can be the wrong move if the loan structure makes future portfolio decisions harder.

FAQ

What is a good offset account interest rate?

A good offset account interest rate is really a good home loan rate on an offset-enabled product after fees. The right benchmark is not just the advertised rate. It is the net result after comparing the rate premium and fees against your expected offset balance.

Do you usually pay a higher home loan interest rate for an offset account?

Often yes. Some lenders charge a higher rate, a package fee, a monthly fee, or a mix of all three for offset eligibility. That is why the feature should be tested with real numbers rather than assumed to be worth it.

Does an offset account reduce monthly repayments?

Usually not automatically. Many lenders keep the scheduled repayment the same, but more of each repayment goes toward principal because less interest accrues. That can help repay the loan faster.

Is offset better than extra repayments?

It depends on your need for flexibility. If you want access to the cash, offset is usually cleaner. If you do not need the money and the product pricing is cheaper without offset, extra repayments may be better.

Is offset better than redraw on an investment property loan?

Often yes for tax hygiene. The ATO's interest guidance makes clear that redraw used for private purposes can require ongoing apportionment. Offset usually avoids that mixed-purpose borrowing problem because the funds were not paid into the loan principal in the first place.

Can an offset account work with a fixed rate loan?

Sometimes, but not always. In Australia the feature is most commonly attached to variable rate home loans or only to the variable split of a split loan. Check the lender's product terms carefully.

Model Your Offset Strategy Before You Apply or Refinance

The best offset setup is not the one with the flashiest feature list. It is the one where the interest you save is consistently higher than the rate premium and fees you pay for the product.

If you are comparing lenders, testing an investment property structure, or deciding whether to keep cash in offset versus making extra repayments, run the numbers first. Use the PropBoss offset calculator, then create a free account at /register/owner to track loan balances, cash flow, and repayment scenarios across your portfolio in one place.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more