SMSF Property Rules ATO Guide for Property Investors

ATO SMSF property rules explained for Australian investors: related parties, LRBAs, valuations, rent, tax, costs, and records in 2026.

SMSF property rules from the ATO allow a self managed super fund to buy investment property when it is acquired, leased, valued, and recorded for retirement. Before buying, transferring, renting, or improving SMSF property, check the sole purpose test, in-house asset rules, borrowing restrictions, and arm's length basis.

SMSF Property Rules ATO Checks Before You Buy

The ATO's starting point is simple: the fund must invest for retirement benefits, not personal use today. That means an SMSF property should fit the investment strategy, have liquidity, and be held on commercial terms.

Purchasing property through a Self-Managed Super Fund (SMSF) requires passing the sole purpose test, purchasing at market value, and not using the property as a personal residence. Legal ownership of assets must stay separate from personal or business assets.

For a $750,000 property with a $300,000 deposit, assess sole purpose, liquidity, diversification, and records before signing.

The ATO's SMSF investment restrictions explain in-house assets and related party dealings.

Self Managed Super Fund Property Owned by a Related Party

A self managed super fund generally cannot acquire residential property from a related party, including members, relatives, companies, trusts, and associates.

Business real property is the main exception. A member's company may sell or lease commercial premises to the fund at market value and on an arm's length basis.

Common errors include member use, relatives renting residential property, weak business leases, below-market rent, and purchases made for personal convenience.

If the property owned by the fund is treated as an in-house asset, the 5% market value limit can become a breach. Document valuations, rent reviews, leases, and member connections before the transaction happens.

The fund must not provide loans or direct financial assistance to a member or relative, and any related party asset acquired by the fund must reflect market value. In-house assets in your SMSF must not exceed 5% of total fund assets; if they do, trustees need a written plan to reduce them.

Related Party Rules for Residential Property

Related party rules are tighter for residential property. A residential SMSF property cannot be lived in by a member or relative, and even market rent can fail if a related party gets present-day access.

Collectables and personal use assets held by your SMSF must be for genuine retirement purposes, cannot provide any present-day benefit, and must be insured within 7 days of acquisition.

Moneysmart's SMSFs and property guidance gives the same warning: trustees must comply before buying.

SMSF Borrowing Power and LRBA Rules

An SMSF can borrow money for property only in limited cases, most commonly through a limited recourse borrowing arrangement. LRBAs allow SMSF trustees to borrow money to purchase property; if the mortgage defaults, only the purchased property is at risk, protecting other SMSF assets.

When using an LRBA, an SMSF can only purchase a single asset, such as one residential or commercial property, and the investment must align with the fund's investment strategy and risk profile.

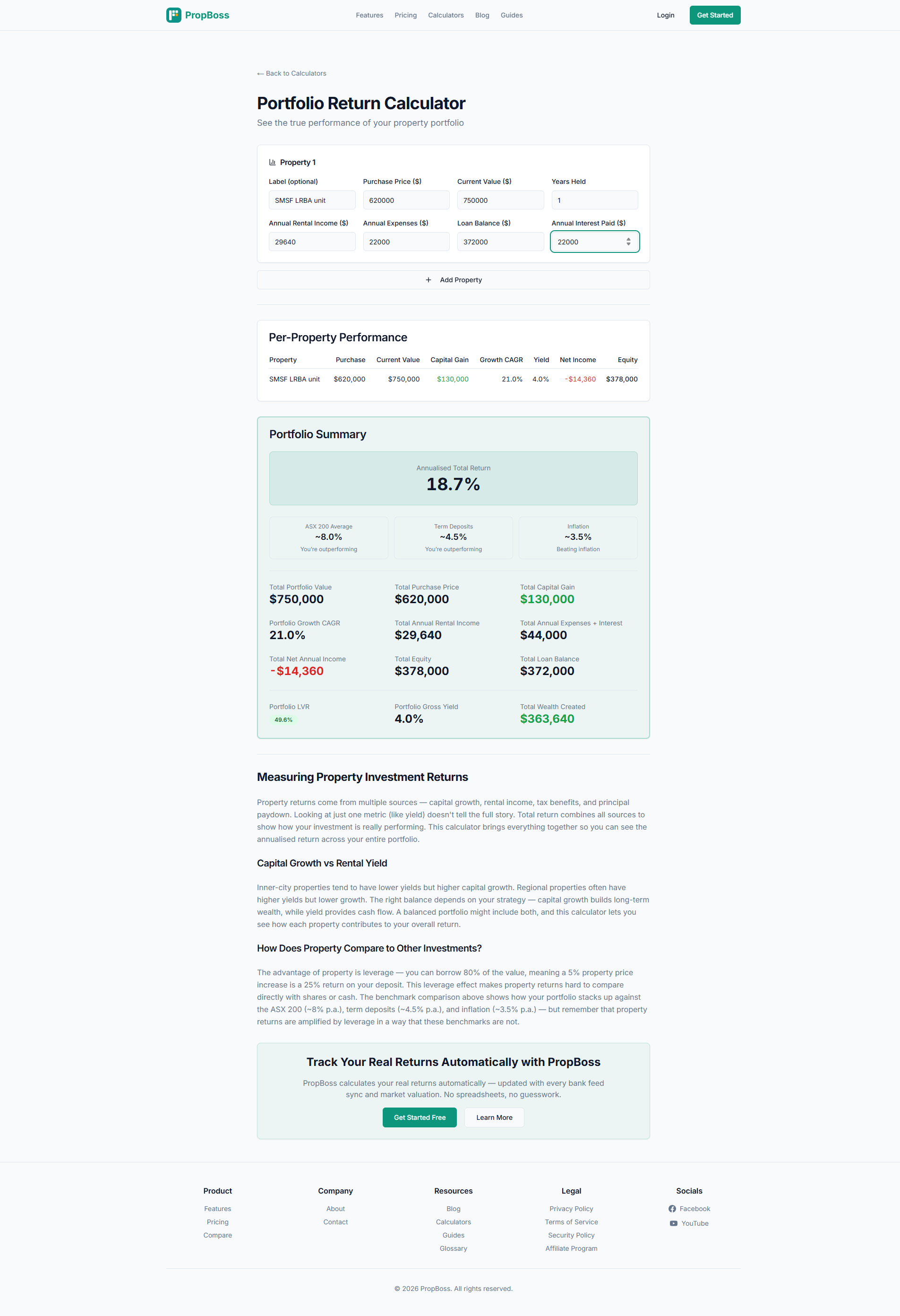

Assume a fund purchases a $620,000 unit with a $248,000 deposit, $31,000 estimated stamp duty and costs, a $372,000 LRBA loan, $570 weekly rent, and $22,000 annual interest and expenses.

Borrowed funds can usually cover repairs and maintenance, but not significant improvements that fundamentally alter the asset. SMSF borrowing power also varies by lender; some assess only 80% of rent for servicing, while others may use 100%, changing the maximum loan size.

PropBoss handles this automatically -- the portfolio return calculator and portfolio dashboard track cash flow, market value, loan position, and return on investment across the whole fund.

Market Value, Tax, and Records Trustees Need

The ATO expects evidence that property is valued at market value and transactions are commercial. Keep appraisals, comparable sales, leases, rent statements, loan documents, and expense records.

Transactions involving SMSF property must be conducted at market value to ensure compliance with arm's length principles; non-compliance may trigger Non-Arm's-Length Income (NALI), taxed at the highest rate of 45%. Assets in an SMSF must be valued at fair market value for financial reporting and audits, supported by verifiable data.

Annual valuation matters for related party leases, LRBAs, large repairs, insurance claims, vacancies, planned transfers, sales, and member benefit payments tied to fund asset values.

Tax records matter too. Rental income, interest, depreciation, land tax, and [capital gains tax](/glossary/capital-gains-tax) need clear records.

Purchase and sale costs can reduce the super balance. Allow for legal fees, stamp duty, loan setup, advice, administration, audit, and management fees before signing.

Read the ATO's SMSF borrowing restrictions before any loan is signed.

Property Owned Inside a Portfolio

SMSF property should not be assessed in isolation. One house can make the fund look strong on paper but weak in liquidity if pension payments, repairs, or rate changes arrive.

Use portfolio measures: net rent after interest, insurance, land tax, and maintenance; loan to value ratio; refinance risk; return on investment after tax; cash buffer; and exposure to one suburb, tenant, or property type.

For a fund with $1.2 million in assets, one $750,000 property represents 62.5% before debt. Trustees should record why it meets the strategy and what happens after a 10-week vacancy.

FAQ

Can I live in my SMSF property?

No. Living in SMSF property is generally a breach because the property must be used for retirement benefits, not current personal use.

Can my business rent commercial property from my SMSF?

It can be possible if the property is business real property, the lease is arm's length, rent is at market value, and the arrangement matches the strategy.

Can an SMSF borrow to buy investment property?

Yes, but only under limited rules such as an LRBA. The fund must comply with superannuation law.

A financial adviser who gives SMSF property advice needs an Australian financial services licence or must be authorised under one.

Is there a tool that automates SMSF property tracking?

PropBoss tracks SMSF property rules with bank feeds, depreciation schedules, ATO-compliant reporting, rental income, expenses, loan records, valuations, and portfolio returns. Start with PropBoss.

Stop Managing SMSF Property in Spreadsheets

SMSF property mistakes usually come from missing records, stale valuations, weak cash flow checks, or unclear related party arrangements. PropBoss tracks SMSF property with portfolio dashboards, bank feeds, EOFY reports, and return modelling from $1/property/month. Try the portfolio return calculator, then start your free trial.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

SMSF Capital Gains Tax: Australian Property Guide for 2026

A practical guide to SMSF capital gains tax on Australian property, with worked examples for accumulation and pension phase investors.

Read more

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more