Cash Flow Real Estate: Forecast Property Returns in 2026

Learn how cash flow real estate works in Australia, with formulas, examples, due diligence checks and forecasting tools for investors.

Cash flow real estate means buying and managing property so the rent, tax position and operating expenses produce a clear surplus or a controlled shortfall. For Australian investors, the question is not just whether a rental property has positive cash flow today. The better question is whether the investment property can keep working after interest rates, vacancy rates, repairs, insurance, land tax and depreciation are included.

This guide shows how to calculate cash flow, how to separate a genuinely cash flow positive asset from a property that only looks profitable, and how to forecast cash flow before you buy property.

What cash flow real estate means

Cash flow is the money left after income and expenses are counted for a property over a monthly or annual period. In real estate, that usually starts with rental income and then subtracts loan interest, council rates, insurance, property management, maintenance, strata, land tax, vacancy allowance and other costs.

A cash flow property can be positive, neutral or negative. A positive cash flow property produces surplus income after regular costs. A negative cash flow property needs extra cash from the property owner to cover the shortfall. A neutral property sits close to break-even.

The calculation sounds simple, but the quality of the answer depends on what you include. Rental income is usually the biggest cash flow driver, and it can move with market conditions, vacancy and tenant demand. Many properties look strong when you only compare rent with loan repayments. Most properties look very different once operating expenses, tax deductions, repairs and vacancy rates are added.

Cash flow positive is not the same as profit

Cash flow positive means the property puts money into your account over the period measured. Profit is broader. It can include capital growth, depreciation, capital works deductions, selling costs and future tax.

For example, a Brisbane rental property could be cash flow positive by $2,000 a year before tax but still deliver weak overall returns if the market value does not grow and major repairs are ignored. Another investment asset could have negative cash flow of $4,500 a year but stronger total value if capital growth and tax benefits are material.

That is why cash flow real estate should be analysed beside capital growth, return on investment and risk.

The cash flow formula investors should use

Use this formula before you buy property and again every year:

| Line item | Annual example |

|---|---|

| Gross rental income | $34,320 |

| Less vacancy allowance | -$1,320 |

| Effective rental income | $33,000 |

| Less loan interest | -$24,960 |

| Less operating expenses | -$6,850 |

| Pre-tax cash flow | $1,190 |

| Add estimated tax refund or subtract tax payable | $620 |

| After-tax cash flow | $1,810 |

In this example, the property is cash flow positive by $1,810 a year, or about $151 per month. It reduces portfolio strain and gives the investor more room for repairs, interest rate changes and future purchases.

Include real operating expenses

Operating expenses should include more than the obvious bills. For a residential investment property, test at least:

- Property management fees, letting fees and statement fees

- Council rates, water charges and strata levy where relevant

- Landlord insurance and building insurance

- Repairs, maintenance and a sinking fund for future work

- Smoke alarm, pest, pool, garden and compliance costs

- Depreciation schedule fees and quantity surveyor costs

- Vacancy allowance, even if the current tenant has been reliable

The ATO rental properties guide distinguishes between rental income, immediately deductible expenses, expenses claimed over several years and capital costs. A cash flow forecast should reflect those timing differences, not just the bank account movement.

Depreciation can also change the after-tax result. Claiming depreciation and hiring a quantity surveyor to create a tax depreciation schedule can significantly lower taxable income for property owners, but it does not remove the need to fund cash expenses as they fall due. Operating expenses such as legal, administration and property management costs are necessary, so the aim is controlled upkeep rather than cutting costs blindly.

Use net operating income before debt

Net operating income, or NOI, is rental income less property operating costs before loan payments. It helps compare real estate deals without mixing in each buyer's debt structure.

Example:

| Measure | Amount |

|---|---|

| Annual rent | $36,400 |

| Vacancy allowance | -$1,400 |

| Operating expenses | -$7,200 |

| Net operating income | $27,800 |

| Purchase price | $650,000 |

| NOI yield | 4.28% |

NOI does not tell you whether the property is cash flow positive after debt. It tells you whether the asset itself earns enough income before your loan structure is added.

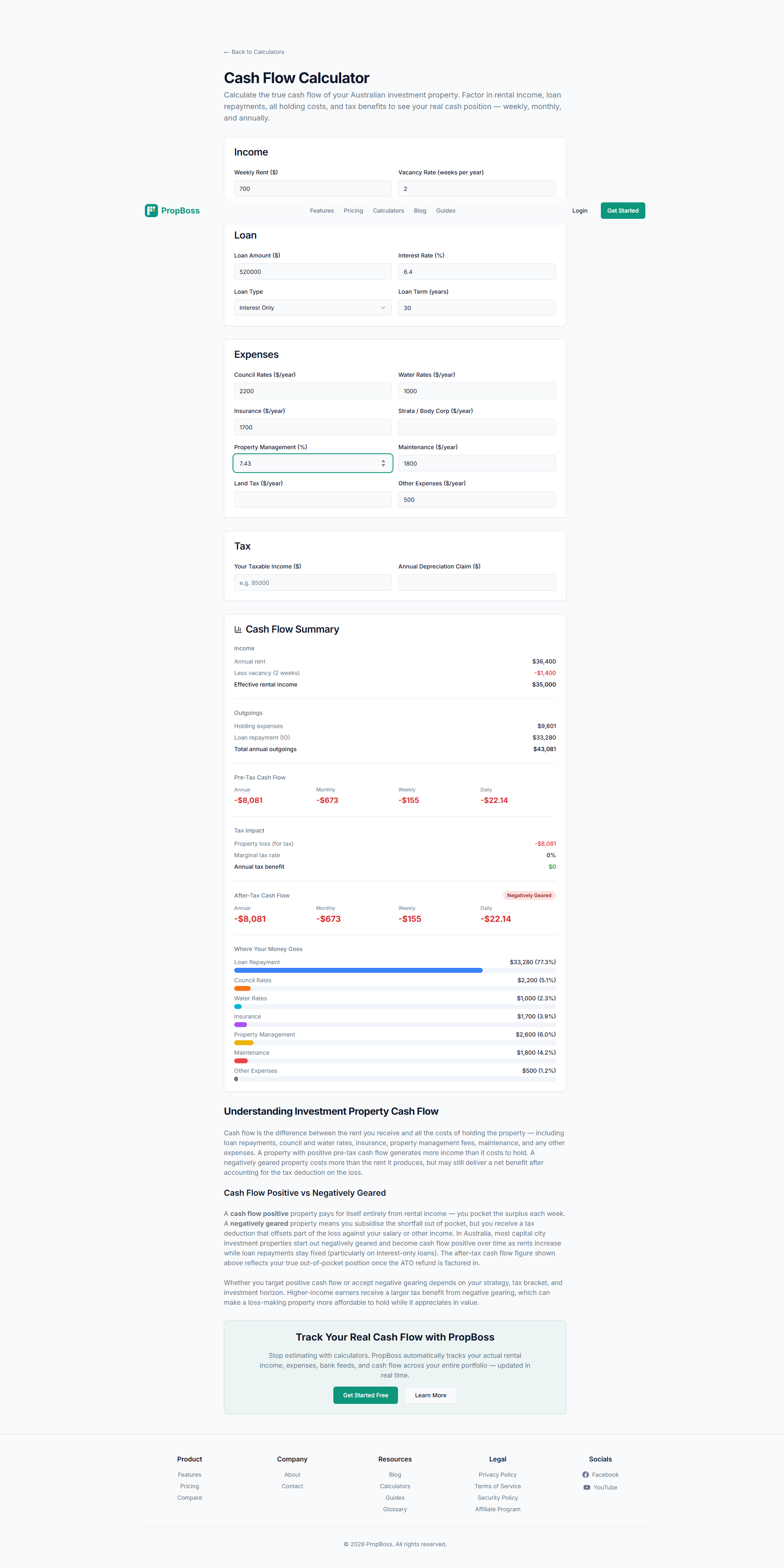

Worked example: a $650,000 rental property

Assume an investor buys a $650,000 property in regional Queensland with a weekly rent of $700. They borrow 80% of the purchase price, or $520,000. They model interest only repayments at 6.4% as a stress-test rate.

Rental income and loan interest

Annual rent is $36,400 before vacancy. If the investor allows two weeks vacant, effective rental income falls to $35,000.

The annual interest cost is:

$520,000 x 6.4% = $33,280

On rent minus interest alone, this property has:

$35,000 - $33,280 = $1,720

That looks cash flow positive, but it is not the finished calculation.

Expenses, tax and positive cash flow

Now add real costs:

| Cost | Annual amount |

|---|---|

| Property management and letting | $2,600 |

| Council and water rates | $3,200 |

| Insurance | $1,700 |

| Repairs and maintenance | $1,800 |

| Compliance and admin | $500 |

| Total operating expenses | $9,800 |

The property now has negative cash flow before tax:

$35,000 - $33,280 - $9,800 = -$8,080

If the investor can claim interest, management fees, rates, insurance and repairs as tax deductions, the after-tax result may improve. But the cash account still needs to handle bills when they arrive.

PropBoss handles this automatically -- cash flow tracking compares rent, expenses, loan interest and tax timing across your portfolio so you can see the monthly cash position before it becomes a problem.

How to find cash flow positive property

Finding cashflow properties is not just chasing high rental yield. A suburb with high rental yield can still produce poor cash flow if insurance, repairs, vacancy rates or management costs are high.

Start with rental income quality

Look for rental income that is supported by tenant demand, not a single optimistic rental appraisal. Check comparable leases, advertised rents, vacancy rates and days on market.

A strong property might have:

- Multiple tenant segments, such as health workers, students, families or trades

- Limited competing rental stock

- Rent below market value with a realistic increase rent pathway

- Low seasonal vacancy risk

- A floor plan that suits long-term tenants

Compare capital growth and cash flow

Cash flow positive property often appears in regional areas, rural areas, mining towns, outer suburbs, dual-income dwellings or properties with a granny flat. These can produce high rental income but may carry lower capital growth, tenant concentration risk or higher maintenance. Some investors use the 1% rule, where monthly rent is compared with 1% of the purchase price, as a quick screen; in Australia it should be a rough filter, not a purchase rule.

Capital growth is still important. The goal is not to chase income at any price. The goal is to know the trade-off.

Check due diligence before you buy property

Due diligence should test whether the income is durable. Before you buy property, verify:

- Current rent, lease end date and market rent evidence

- Insurance quotes for the actual address

- Council rates, strata minutes and special levies

- Flood, bushfire and building risk

- Recent repairs and likely capital works

- Local employment concentration

- Agent fees, reletting costs and vacancy assumptions

The best cash flow real estate decisions are made before contract, not after settlement.

Commercial property and cash flow

Commercial property can offer stronger income than residential property, but it has different risks. It can also have longer vacancy periods, incentive payments, GST treatment and more complex leases.

For cash flow, review the lease before reviewing the headline yield. A commercial property with an 8% yield and a weak tenant may be riskier than a residential rental property with a 4.8% yield and strong tenant demand.

Important commercial property checks include:

- Lease term, option periods and rent review clauses

- Outgoings recovery and who pays which costs

- Tenant quality and industry exposure

- Make-good obligations

- Vacancy allowance based on months, not weeks

- Capital expenditure for compliance or fit-out

Commercial property can help a portfolio, but the internal rate of return depends on both income and exit value.

Positive vs negative cash flow

Positive cash flow is attractive because it reduces the amount of personal income needed to hold the property. Investors often describe cash flow as the fuel of a portfolio because it helps the investment stay sustainable over the long term. Negative cash flow is not automatically bad if the investor can afford it and expects enough capital growth or tax benefits to justify the shortfall.

The risk is accidental negative cash flow. Negative cash flow happens when rental income is insufficient to cover operating expenses and debt service, leading to a deficit that can be unsustainable over time. It can also happen when an investor expected a neutral property but forgot costs like vacancy, repairs, insurance, strata, land tax or interest rate resets.

When positive cash flow helps

Positive cash flow can help investors who want:

- More borrowing resilience

- Less pressure on annual income

- Extra money for maintenance and buffers

- A portfolio that can hold through rate rises

- Passive income as a long-term goal

When negative cash flow can still make sense

Negative cash flow can be acceptable where the investor has enough surplus income, the market has strong capital growth prospects and the loss is understood before purchase. Negative gearing may also reduce taxable income, but investors should never rely on a tax refund to make a weak deal work.

The ATO expects rental property claims to be connected to income-producing use and properly documented. Keep records for rent, interest, repairs, management fees, depreciation and capital works so the tax position can be explained.

How to improve investment property cash flow

Improving cash flow is usually a mix of income, cost control and loan structure.

Increase rental income carefully

Review rent against comparable properties before each lease renewal. A rent increase should consider state notice rules, tenant retention and market evidence. Losing a strong tenant for four vacant weeks can erase the benefit of a higher monthly rent.

Other income options may include pet rent where lawful, separately metered utilities, a furnished lease, storage lockers, parking or adding a granny flat where planning rules and numbers support it. Creating additional revenue streams, such as converting unused space into storage lockers or paid parking, can significantly boost cash flow for property investors, but check tenancy law, strata rules and tenant demand before adding them to a forecast.

Reduce expenses without cutting quality

Cost savings should not create bigger risks. Compare insurance, review property management fees, fix small maintenance issues early and check whether council rates or land tax assessments are correct.

Repairs and maintenance can be deductible when they remedy wear, damage or deterioration from rental use. Improvements, replacements and capital works may be treated differently. The ATO repair and maintenance guidance is worth checking before assuming every repair creates an immediate tax deduction.

Adjust the loan structure

Interest only loans can improve short-term cash flow but usually increase total interest over time. Principal and interest repayments build equity faster but place more pressure on monthly cash.

Investors should model both repayment types, plus a higher interest rate scenario. A property that only works at today's rate may become a negative cash flow property after a reset, especially when inflation and lending conditions shift; the RBA's CPI explainer is a useful reference for understanding inflation measures that affect rent, expenses and rates.

Cash flow forecasting across multiple properties

One property can be analysed in a spreadsheet. Multiple properties become harder because rent, expenses, tax, depreciation, loan repayments and repairs arrive at different times.

For a broader cash flow method, compare this approach with the existing PropBoss guide to calculating investment property cash flow.

Creating a cash flow management strategy involves measuring incoming and outgoing funds regularly, using detailed budgets or simpler tracking methods depending on the investor's preference. It also helps to separate bad debt tied to non-income-producing assets from good debt connected to an investment property capable of producing income.

For a portfolio, forecast:

- Monthly cash flow per property

- Total portfolio cash flow

- Emergency buffers per property

- Annual tax deductions and tax refund timing

- Repairs and capital expenditure by year

- Equity position and loan to value ratio

- Scenario tests for vacancy, interest rates and rent changes

This is where many investors lose visibility. They know annual income, but not the month where three insurance premiums, rates notices and a vacancy land together.

FAQ

Is cash flow real estate a good strategy in Australia?

Cash flow real estate can be a good strategy when the numbers are tested properly. It suits investors who want income resilience, serviceability support and less pressure on wages. It is weaker when investors chase high rent without checking vacancy rates, repairs, insurance and long-term capital growth.

What is a good cash flow for a rental property?

A good result depends on the investor's goals, loan size and risk. As a practical rule, a property that stays positive after vacancy, repairs, interest, management fees and insurance is stronger than one that only looks positive before expenses. Even $100 to $200 per month can matter across multiple properties.

How do I calculate whether a property is cash flow positive?

Add annual rental income, subtract vacancy, subtract loan interest and operating expenses, then estimate the after-tax position. You can use the PropBoss cash flow calculator to compare scenarios before you buy.

Is there a tool that automates cash flow tracking?

PropBoss tracks cash flow across all your investment properties with automated bank feeds, depreciation schedules and ATO-compliant reporting. It handles rental income, expenses, loan interest and portfolio cash flow tracking so you don't need spreadsheets. You can start from the owner signup page.

Does positive cash flow mean the property will build wealth?

Not always. Positive cash flow improves income, but wealth also depends on capital growth, debt reduction, tax, purchase price, holding costs and exit value. The better question is whether the property improves your full portfolio position.

What external records should investors keep?

Keep lease agreements, rent statements, bank records, loan statements, invoices, property manager reports, insurance schedules, depreciation schedules and settlement documents. The ATO rental property guidance expects claims to be supported by records, especially where expenses are partly private, capital or spread across several years.

Stop managing spreadsheets

Stop managing spreadsheets. PropBoss tracks cash flow automatically across every property in your portfolio.

Use the cash flow calculator to test a property before you buy, then use PropBoss to track rent, expenses, depreciation, bank feeds and tax-ready reports from $1/property/month with a free trial.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more