Mortgage Broker Investment Property Guide Australia 2026

A practical Australian guide to choosing a mortgage broker for investment property finance, with broker questions, worked repayment examples, tax considerations and portfolio checks.

A mortgage broker for an investment property should help compare lender policy, loan structure, borrowing capacity, cash flow and tax trade-offs before you apply. The right mortgage broker helps property investors choose an investment loan that fits the property, entity, rental income, deposit, offset account strategy and next investment property.

For Australian investors in 2026, this matters because lending policy is tight, the RBA cash rate target was 4.10% in March 2026, and many lenders still assess investment property loans with buffers above the advertised interest rate. A small difference in loan features can change how much you can borrow money for and how quickly your investment property portfolio can grow.

What Should Property Investors Expect From a Mortgage Broker?

A mortgage broker compares investment property loans across different lenders and helps match your financial situation to a suitable loan product. For an owner-occupier home loan, the focus is usually repayment comfort. For an investment property, the broker also has to consider rental income treatment, tax deductions, loan-to-value ratio, future borrowing capacity and whether the loan structure supports your investment strategy.

The broker's role should include:

- Mortgage brokers assist property investors by clarifying how much they can realistically borrow before making offers, using borrowing power calculators that consider income, debts, and expenses.

- Comparing a wider range of lenders, investment loan rates and fees across major banks and non-bank lenders.

- Explaining fixed rate, variable rate, interest only repayments and principal and interest options.

- Showing how lenders assess rental income, existing debt, living expenses and existing loans.

- Helping you decide whether to use an offset account, extra repayments or split loan structure.

- Coordinating documentation, pre-approval, valuation, formal approval and settlement.

- Reviewing the loan after settlement so the rate, lender exposure and structure still support future purchases.

A good mortgage broker should not simply ask, "What is the lowest rate?" The better question is, "Which right loan keeps this property affordable and leaves room for the next property?"

They should also explain where finance fits in the wider property investment process, from pre-approval and upfront costs through to settlement and post-settlement tracking.

Since January 2021, Australian mortgage brokers must act in the client's best interests and disclose how they are paid. Check that the broker holds an Australian Credit Licence or is a registered credit representative, which you can verify through ASIC's Professional Registers.

Why Investment Property Loans Are Assessed Differently

An investment property loan is assessed differently from a standard owner-occupier home loan because the property is meant to generate rental income, tax outcomes and capital growth. Lenders assess the expected rental income, but they rarely count 100% of it. Many shade rent to allow for vacancy, property management fees, insurance, repairs and other holding costs.

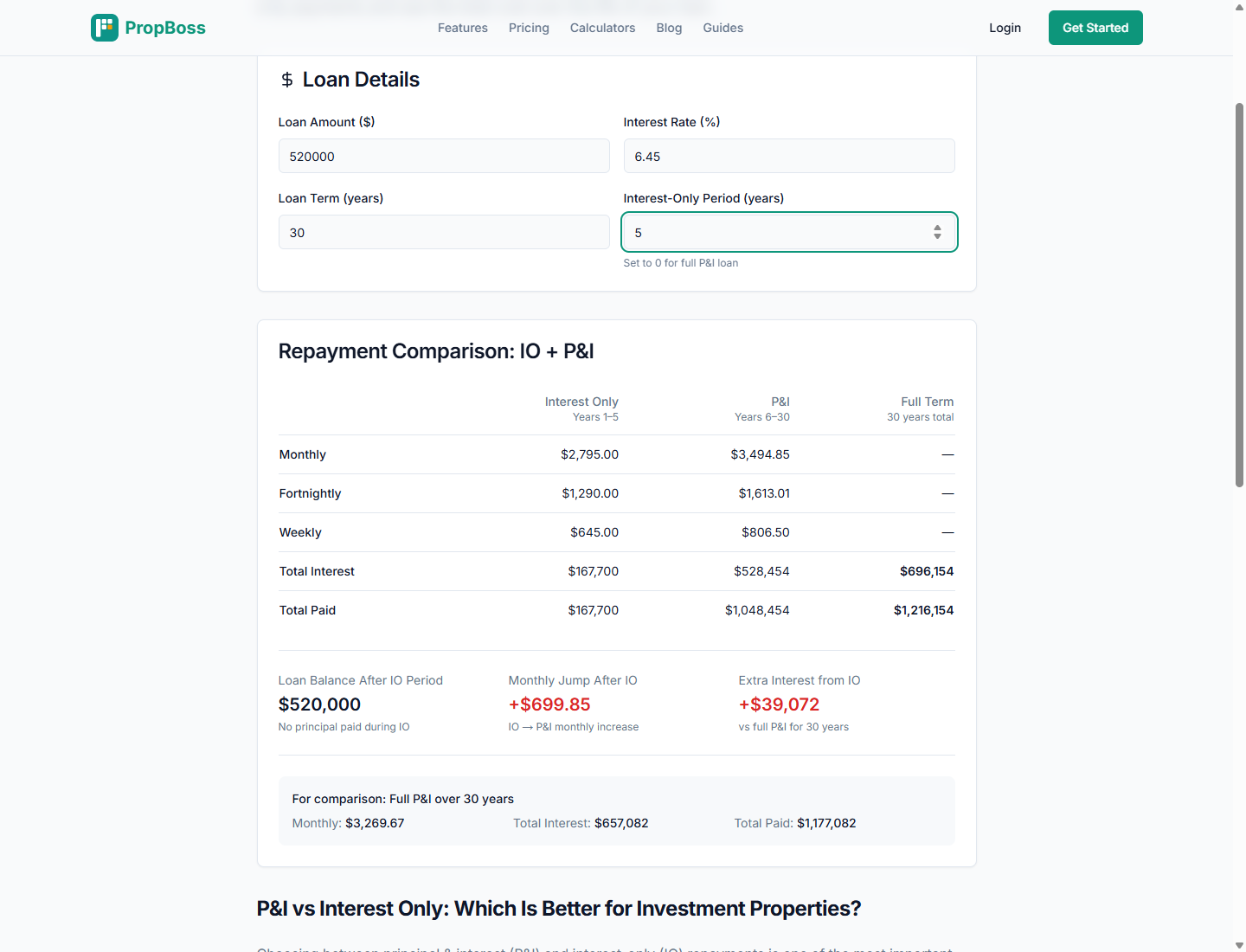

For example, assume you buy a $650,000 Brisbane townhouse with:

| Item | Amount |

|---|---|

| Purchase price | $650,000 |

| Loan amount at 80% LVR | $520,000 |

| Expected weekly rent | $650 |

| Gross annual rental income | $33,800 |

| Lender rental shading at 80% | $27,040 |

Even though the property may collect $33,800 in rental income, a lender might use only $27,040 in serviceability, close to the common 80% rental shading for vacancy and risk. If existing debt and living expenses are near the lender's limit, the same property can pass with one lender and fail with another.

Loan-to-value policy also matters. Many lenders may allow investment borrowers up to 90% LVR, and some scenarios can reach 95% with lender's mortgage insurance, but the higher leverage can reduce lender choice and increase cost.

This is where an investment property mortgage broker can add value. They should know which different lenders are more flexible with rental income, self-employed income, trust distributions, company borrowers, SMSF structures and existing loans.

How Lenders Assess Rental Income and Borrowing Capacity

When lenders assess rental income, they are trying to answer one question: can you make the loan repayments if rent falls, rates rise or expenses increase? They usually test your loan at an assessment rate above the actual interest rate. They also include living expenses, personal loans, credit card limits, existing home loan repayments and other debts.

Consider a couple with $190,000 combined gross income and one existing property:

| Scenario | Amount |

|---|---|

| Existing home loan balance | $610,000 |

| Proposed investment loan | $520,000 |

| Actual interest rate | 6.45% |

| Assessment buffer | 3.00% |

| Assessed rate | 9.45% |

| Assessed annual interest on new loan | $49,140 |

The actual interest payments might be closer to $33,540 in the first year if the investment loan is interest only, but the lender may assess the application at a much higher repayment. This is why serviceability can be the real constraint even when the property looks cash flow positive on paper.

PropBoss handles this automatically -- the loan repayment calculator helps model interest rate changes, loan repayments and cash flow scenarios across your entire portfolio before you speak with a lender.

Property Investing Questions to Ask a Mortgage Broker

Before choosing a mortgage broker investment property specialist, ask questions that reveal whether they understand property investing, not just residential lending.

Ask About Investment Loan Experience

Ask how many investment property loans they settle each month and what types of borrowers they regularly support. A broker who mostly handles first home buyer applications may still be competent, but an investor with multiple properties needs deeper policy knowledge.

Check Lender Policy and Broker Reviews

A broker should provide access to a wider range of lenders, identifying products with favourable investment terms, lower interest rates or specific features. They should also compare lenders based on how they assess investment borrowers, because different policies can change borrowing limits and approval outcomes.

Broker due diligence matters too. When selecting a broker, it is important to consider their experience with investment strategies, lender diversity, and a track record of positive reviews. A mortgage broker helps property investors navigate the loan application process by making sure documents are prepared and submitted correctly to avoid delays.

Useful questions include:

- Which lenders are currently strong for investment property loans?

- Which lenders assess rental income most favourably?

- How do you model borrowing capacity for the next investment property?

- Do you work with trusts, companies or SMSF borrowers?

- How do you compare interest only repayments against principal and interest repayments?

Ask About Loan Structure

Loan structure can affect tax, cash flow and future flexibility. Your mortgage broker should explain how to separate deductible and non-deductible debt, why redraw can create tax complications, and when an offset account may be cleaner than redraw.

For example, using an offset account against an investment loan can preserve the loan balance while reducing interest payments. Redrawing extra repayments for private spending can make part of the interest non-deductible. The ATO expects investors to trace what borrowed money is used for, so mixing purposes inside one loan can create avoidable record keeping problems.

Ask About the Right Loan for Your Portfolio

The right loan is not always the cheapest loan. For a single property, a basic variable loan may be fine. For an investment property portfolio, the right investment loan may need offset accounts, split facilities, flexible valuations, strong cash-out policy and lender appetite for future lending.

That is why the right loan structure should be documented before you apply, not reverse-engineered after settlement.

Ask your broker to show at least two options:

- A lowest-cost loan option for the specific investment property.

- A portfolio-aware option that protects borrowing capacity and future strategy.

If the second option has a slightly higher interest rate but better loan features, it may still be the right loan for a property investor planning to buy again.

For a growing portfolio, the broker should test whether restructuring existing loans could free up equity without forcing every property under one lender. A quality mortgage broker will structure loans to allow for future property purchases, focus on long-term portfolio growth, and use ongoing reviews to keep rates competitive while avoiding cross-collateralisation.

Investment Loan Rates and Loan Features to Compare

Investment loan rates are important, but the rate is only one part of the loan product. A broker should compare the total cost and the features that affect your investment strategy.

Loan Options to Compare Beyond the Headline Rate

Good brokers should show how investment property loans differ on fees, offset access, repayment rules, cash-out policy and stricter criteria for self-employed investors, trust borrowers or investors with multiple securities.

The right lender should fit your financial goals, personal circumstances and long term wealth plan. For most investors, the best investment loan rates matter only after the structure protects borrowing capacity, tax records and the next purchase.

If you are investing in property with an investment portfolio, ask where the loan process could cost more money or weaken negative gearing. The point is to make the trade-offs visible before you commit.

Interest Rate and Comparison Rate

The interest rate determines regular interest payments. The comparison rate includes some fees and can be useful for comparing standard loan products. It is less useful when you are comparing offset packages, split loans, interest only periods or loans with different features.

In 2026, stress test any investment loan at least 2 percentage points above the advertised rate. A $520,000 loan at 6.45% interest only costs about $33,540 per year; at 8.45%, it costs about $43,940. That $10,400 difference can turn a manageable property into a stressful process.

Interest Only or Principal and Interest

An interest only loan can improve short-term cash flow because you pay only interest during the interest only period. Principal and interest repayments reduce the loan balance but increase monthly repayments.

Fixed rate investment loans give repayment certainty but can limit extra repayments and refinancing during the fixed term. Variable rate investment loans can fluctuate with market conditions, offering greater flexibility but less certainty in repayment amounts over time. Different repayment structures, such as interest-only or principal and interest repayments, can significantly affect monthly cash flow for property investors, impacting their overall financial strategy.

Principal and interest (P&I) investment loans involve repayments that cover both the principal and interest, gradually reducing the loan balance over time, resulting in higher monthly payments compared to interest-only loans.

For a $520,000 investment property loan at 6.45%, the repayment difference is material:

| Structure | Approx monthly repayment | Year one cash effect |

|---|---|---|

| Interest only | $2,795 | Lower repayments |

| Principal and interest over 30 years | $3,270 | Higher repayments |

The interest only option frees about $475 per month, but it does not reduce the loan balance. Your broker should explain whether the repayment jump still fits your cash flow.

Offset Account and Extra Repayments

An offset account can reduce interest while keeping cash accessible. Extra repayments can also reduce interest, but redraw treatment needs care when the property is an investment property. If you redraw for private spending, the interest on that portion may not be deductible.

This is why the "best investment loan" is not always the one with the lowest rate. A slightly higher rate with a full offset account can be better if you hold emergency cash, future deposits or tax money.

Cash flow is especially important in the early years of ownership, when maintenance, insurance, council rates, property management fees and vacancy can arrive before rent increases. Underestimating those ongoing costs can strain the property and reduce future borrowing ability.

Loan Structure for Tax Deductions and Cash Flow

Investment property loans interact with tax because interest expenses may be deductible when the borrowed money is used to buy or maintain a rental property. The ATO's rental property guidance explains that investors can claim eligible expenses, but the purpose of the borrowing matters.

This does not mean every interest payment is deductible. If part of the loan is used for private expenses, that part may not support a tax deduction. If you refinance and increase the loan amount, you need to track what the new borrowing was used for.

Example: Clean Investment Loan Structure

Emma buys a $720,000 investment property in Adelaide. She contributes a $144,000 deposit and borrows $576,000. The loan is used only for the property purchase and settlement costs. Her broker sets up:

- One investment loan for the property purchase.

- One offset account for surplus rent, tax savings and emergency funds.

- No redraw for private spending.

- Separate accounts for personal living expenses.

This is a clean structure. The loan purpose is clear, the tax return is easier, and the cash flow is easier to reconcile.

Example: Messy Loan Structure

Daniel has a $500,000 investment loan. He makes extra repayments, then redraws $55,000 for private spending. His loan is still secured against the investment property, but part of the borrowed money was used privately.

That makes tax reporting harder. A better broker would have explained this at the very beginning and suggested an offset account instead of redraw for flexible cash.

Protecting Your Investment Property Portfolio Borrowing Power

The first investment property is rarely the last for serious property investors. A broker should consider how today's loan affects tomorrow's borrowing capacity.

Future borrowing power can be affected by:

- Which lender you use first.

- Whether the loan is fixed rate or variable.

- Whether the property is cash flow positive or negatively geared.

- How much existing debt remains.

- Whether you cross-collateralise properties.

- Whether the lender takes actual or assessed repayments for existing loans.

- Whether the bank treats rental income, bonuses and self-employed income favourably.

Cross collateralisation can look convenient because one lender takes multiple properties as security. It can also reduce flexibility. If you want to refinance, sell one property or extract equity, one lender controls more of the portfolio.

An investor-focused mortgage broker should be able to explain whether keeping securities separate is better for your investment property portfolio.

When a Broker May Not Be the Right Fit

Not every mortgage broker is suitable for every investor. A broker may not be the right fit if they:

- Push one lender without explaining alternatives.

- Focus only on the lowest advertised interest rate.

- Cannot explain how lenders assess rental income.

- Avoid discussing loan structure, tax implications and future borrowing power.

- Do not document assumptions in writing.

- Cannot compare investment loan rates against loan features.

- Treat your first investment property as if it were a home buyer purchase.

Also be careful if a broker is tied too closely to a property buyer's agent, developer or investment seminar. The loan advice should stand on its own. Moneysmart warns investors to understand property investment risks, costs and borrowing commitments before they proceed.

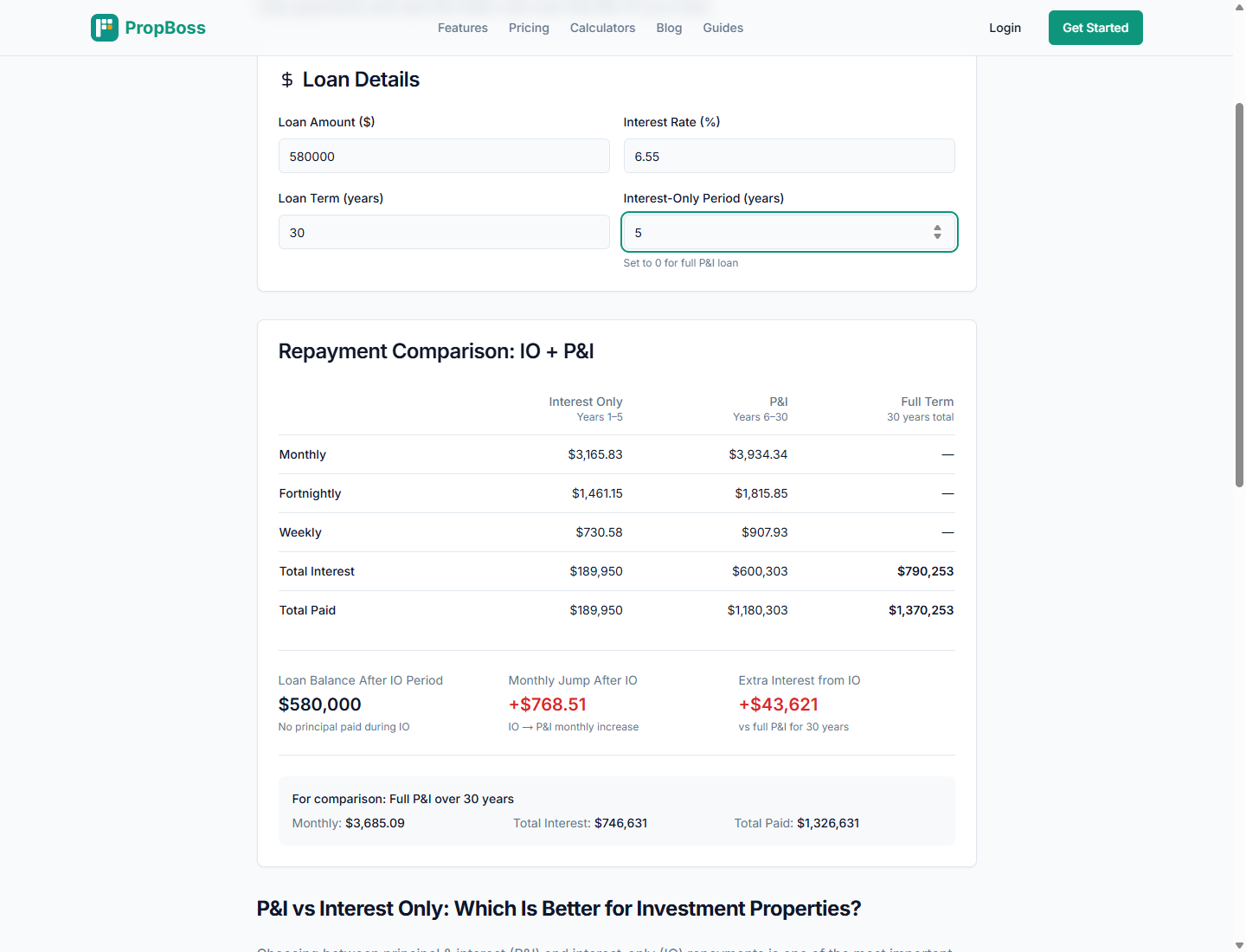

Worked Example: Choosing the Right Loan

Sarah and Michael own their home in Sydney and want to buy a $680,000 investment property in Brisbane. They have $170,000 in savings and want to keep $40,000 aside for repairs, vacancy and tax.

The purchase price of an investment property is only one part of the overall cost; investors should also account for upfront costs such as stamp duty, legal fees and inspections, plus ongoing expenses like council rates, insurance, maintenance and property management fees.

Their property investment plan:

- Purchase price: $680,000.

- Deposit and costs available: $130,000.

- Proposed loan amount: $580,000.

- Expected rent: $680 per week.

- Expected gross rental income: $35,360 per year.

- Interest rate: 6.55%.

- Holding costs excluding interest: $9,200 per year.

Option 1: Lowest Rate Basic Loan

The basic loan has a 6.39% interest rate and no offset account. Interest only repayments are about $3,089 per month. Annual interest is about $37,062.

This looks attractive, but their spare $40,000 emergency fund sits in a separate savings account. If that account earns 4.50% before tax, the after-tax benefit may be lower than the interest saving they could get from offsetting the investment loan.

Option 2: Slightly Higher Rate With Offset

The offset loan has a 6.55% interest rate and a full offset account. Interest only repayments on the full loan would be about $3,166 per month, but the $40,000 offset reduces interest charged.

Approximate annual interest after offset:

| Item | Amount |

|---|---|

| Loan balance | $580,000 |

| Offset balance | $40,000 |

| Net interest-charged balance | $540,000 |

| Interest rate | 6.55% |

| Approx annual interest | $35,370 |

Despite the higher rate, the offset structure may cost less while keeping cash available. It can also keep the loan purpose cleaner than redraw.

Option 3: Split Loan Structure

The broker also models a split loan: 60% variable with offset and 40% fixed rate. This gives some repayment certainty while preserving flexibility for surplus cash.

For Sarah and Michael, the right loan may be option 2 or option 3, not the lowest-rate basic loan. The decision depends on cash flow, risk tolerance, future deposits and whether they plan to buy another property within two years.

How to Prepare Before Speaking With a Broker

You will get better advice if you prepare before the first meeting. Complete documents also help the broker manage the loan application process and avoid approval delays.

Prepare:

- Payslips, tax returns or business financials.

- Existing home loan and investment loan statements.

- Credit card limits, car loans and personal loans.

- Rental income statements.

- Council rates, insurance, strata and property management costs.

- Savings, offset account balances and deposit evidence.

- Your target purchase price and preferred suburbs.

- Your investment goals for the next three to five years.

Use the investment property cash flow guide to understand likely income, interest payments and holding costs before you ask for lender options.

Mortgage Broker Fees and Commissions

Most Australian mortgage brokers are paid by the lender if the loan settles. They may receive an upfront commission and an ongoing trail commission. Some brokers also charge a client fee, especially for complex investment property lending, commercial structures or SMSF borrowing.

Ask for the credit proposal disclosure and commission details. A transparent broker should explain:

- Whether you pay a fee.

- Which lenders are on their panel.

- How they are paid.

- Whether one lender pays more than another.

- Why the recommended loan product is suitable.

Commission does not automatically mean poor advice, but you should understand incentives. If two loans are similar, ask why the broker prefers one.

Red Flags in Investment Property Lending Advice

Be cautious when the advice sounds too simple. Investment property finance should include trade-offs.

Red flags include:

- "Just use the maximum loan amount because property always goes up."

- "Interest only is always best for investors."

- "Principal and interest is always safer."

- "The lowest rate is the best loan."

- "Use one lender for every property because it is easier."

- "You do not need to worry about tax until later."

There is rarely one right investment loan for every investor. A first investment property, a negatively geared apartment, a regional cash flow property and a multi-property portfolio can each need a different loan structure.

External Checks Investors Should Make

Before relying on a broker recommendation, check the assumptions against official sources:

- Reserve Bank monetary policy and cash rate target: RBA monetary policy.

- ATO rental property income and deductions: ATO rental properties.

- Moneysmart property investment risks: Moneysmart property investment.

Use these sources to check interest rate risk, deductions and property investment risk.

FAQ

Is a mortgage broker worth it for an investment property?

A mortgage broker can be worth it if they understand lender policy, rental income, loan structure and portfolio borrowing capacity. The value is finding a loan that supports your goals and next property.

What is the best investment loan structure?

The best structure depends on cash flow, tax position, risk tolerance and future borrowing plans. Compare interest only, principal and interest, fixed rate, variable rate, split loans and offset accounts.

Should I choose interest only repayments?

Interest only repayments can help cash flow because monthly repayments are lower, but the loan balance does not reduce. Plan for the repayment increase when the interest only period ends.

Can a broker help me borrow money for multiple properties?

Yes, if they model the whole portfolio. They should check existing loans, rental income, lender exposure limits, borrowing capacity and whether one lender is becoming too concentrated.

Is there a tool that automates mortgage broker investment property planning?

PropBoss automates portfolio tracking. It gives cleaner numbers before and after the loan is set up: income, expenses, interest, cash flow, repayments and portfolio performance.

Stop Managing Spreadsheets

Use the loan repayment calculator to model repayments, rate changes and cash flow before speaking with a broker. Then use PropBoss to track the property, bank feeds, rental income, expenses and portfolio performance.

[Start your free trial]( Also read our investment loan repayment calculator. /register/owner) from /register/owner. Plans start from 1/property/month, so loan records, cash flow and tax reporting stay organised.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more