Interest-Only Loans Explained for Australian Investors

Last updated: April 2026 · Financial year 2025-26

Home / Guides / Interest-Only Loans Explained

What Is an Interest-Only Loan?

An interest-only loan is a home or investment loan where your minimum repayment covers only the interest for a fixed period, usually one to five years. Many investors search for an "interest only loan" or "interest only home loan" when comparing structures, but the mechanics are the same: because you are not repaying principal during that period, your loan balance stays flat unless you make extra repayments or hold cash in an offset account.

For Australian property investors, interest-only lending sits inside a bigger loan-management decision. It affects your monthly cash flow, your tax deductions, your serviceability, and the size of the repayment jump once the loan switches back to principal and interest.

That is why the right question is rarely "Is interest only good or bad?" The better question is whether the structure fits your current portfolio stage, risk buffer, and plan for the next three to five years. Used well, it can improve flexibility. Used badly, it can leave you with a nasty repayment shock.

Worked Example - 12 Parkview Street, Chermside West QLD 4032

| Item | Annual Amount |

|---|---|

| Purchase price | $820,000 |

| Loan balance | $650,000 |

| Interest rate | 6.40% |

| Gross rent ($760/week x 52) | $39,520 |

| Interest-only loan cost | -$41,600 |

| Council rates and water | -$3,900 |

| Insurance | -$1,850 |

| Property management (7%) | -$2,766 |

| Repairs and maintenance allowance | -$1,500 |

| Net cash position before tax | -$12,096 |

This is the kind of scenario many investors face in 2026: the rent is healthy, but the loan still dominates the numbers. That makes loan structure, rate review, and repayment planning just as important as the property itself.

How Does an Interest-Only Investment Loan Work?

Here is the practical flow most investors deal with.

-

You choose a repayment type. If you select interest only, your minimum repayment covers only interest. If you select principal and interest, every repayment also reduces the loan balance.

-

The lender sets an interest-only term. Most lenders will approve an interest-only period for a defined window, often one to five years, with stricter rules once you already have several loans or a higher loan-to-value ratio.

-

Your tax and cash-flow profile changes. Interest-only repayments are lower, which can help cash flow. On an investment property, the interest portion is usually deductible, so many investors use interest only while they prioritise buffers, other debt, or another acquisition.

-

Your serviceability is still stress-tested. Even if your actual repayment is lower, lenders often assess you on a harsher repayment profile. That means interest only can help your real cash flow while doing less for borrowing power than investors expect.

-

The loan eventually reverts. When the interest-only term ends, the same balance must be repaid over the shorter remaining loan term. That is where repayment shock appears.

Calculate your exact repayment change with our free Loan Repayment Calculator.

What Is the Tax Impact by Income Bracket?

Interest-only loans matter more to investors on higher marginal rates because the deductible interest bill is larger in dollar terms and more valuable after tax.

Tax Savings by Income Bracket - $41,600 Annual Interest Cost (2025-26 FY)

| Taxable Income | Marginal Rate | Annual Tax Saving | Effective After-Tax Interest Cost |

|---|---|---|---|

| $18,201 - $45,000 | 16% | $6,656 | $34,944 |

| $45,001 - $135,000 | 30% | $12,480 | $29,120 |

| $135,001 - $190,000 | 37% | $15,392 | $26,208 |

| $190,001+ | 45% | $18,720 | $22,880 |

The deduction helps, but it does not magically make a weak property perform. You still need enough rent, enough buffer, and a plan for the day rates stay high longer than expected.

Use the Loan Repayment Calculator alongside the Cash Flow Calculator so you can see the loan and the property together instead of looking at repayments in isolation.

What Can You Do to Manage an Investment Loan Better?

The best loan-management moves are usually operational, not glamorous.

| Action | What It Does |

|---|---|

| Stay interest only for a fixed period | Preserves short-term cash flow while keeping the loan balance unchanged. |

| Switch to principal and interest early | Builds equity faster and reduces lifetime interest cost. |

| Use an offset account | Cuts interest charged without reducing the deductible debt balance. |

| Make extra repayments selectively | Lowers future interest, but can reduce flexibility and complicate tax use if you redraw later. |

| Split fixed and variable debt | Gives partial rate certainty while keeping some offset and redraw flexibility. |

| Refinance after a pricing review | Lowers rate, changes features, or resets a weak product structure. |

| Extend the interest-only term | Can preserve cash flow, but usually requires a fresh serviceability review. |

| Tighten serviceability inputs | Closing card limits and reducing consumer debt can improve borrowing capacity. |

If you want to explore the repayment side first, start with the Loan Repayment Calculator. If you want to test whether a lower rate justifies a change, use the Refinance Calculator.

Useful supporting reads for this cluster include:

- Investment Loan Repayment Calculator

- Extra Loan Repayment Calculator Australia Guide 2026

- Interest-Only Home Loan Calculator Guide 2026

- Interest-Only Investment Loan Guide 2026

- IO vs PI Investment Property Guide 2026

Interest Only vs Principal and Interest

| Factor | Interest Only | Principal and Interest |

|---|---|---|

| Monthly repayment today | Lower | Higher |

| Loan balance during the term | Usually unchanged | Reduces with each repayment |

| Total interest over full term | Higher | Lower |

| Repayment shock later | Higher risk | Lower risk |

| Tax deductibility on an investment property | Larger ongoing interest bill | Smaller interest bill over time |

| Equity built from repayments | Minimal | Meaningful |

| Buffer strategy | Works well with offset | Works well with offset or direct debt reduction |

| Best fit | Growth and flexibility phase | Consolidation and debt reduction phase |

The important point is not that one is always better. It is that they solve different investor jobs. Interest only is a cash-flow and flexibility tool. Principal and interest is a debt-reduction tool.

Is Interest Only Still Worth It in 2026?

In April 2026, many Australian investors are still dealing with rates that feel high relative to the last cycle. That means interest-only lending is still relevant, but the reason to use it needs to be stronger than "the repayment is smaller."

Interest only can still be worth it when you are deliberately preserving cash flow for an offset strategy, paying down non-deductible home debt first, or keeping flexibility before a refinance or portfolio expansion. It can also make sense when rental growth is still catching up to loan costs and you want breathing room without selling.

It is weaker when you have no buffer, no offset balance, no plan for reversion, and no reason to preserve the higher deductible debt. In that situation, the lower repayment can hide a poor long-term debt outcome rather than improve it.

The best investor use case in 2026 is usually intentional: interest only for a period, plus a clear exit path into a stronger position. That exit path might be a larger offset balance, a refinance, higher rent, or a switch to principal and interest after another debt is gone.

The Role of Serviceability in Loan Management

Serviceability is the factor most competitors barely explain, but it often decides what investors can do next. You can have strong equity and a decent deposit and still fail the next application because your lender does not believe the cash flow stacks up.

Lenders do not just look at the rate on your statement. They typically assess your loan at a higher rate, factor in existing debts, trim rental income, and include living-expense assumptions. In practice, a borrower paying interest only today may still be assessed as though the debt must survive a principal-and-interest repayment at a stressed rate.

That is why investors who want to grow need to manage serviceability like a real asset. Lowering unnecessary credit limits, keeping clean transaction histories, reducing personal debt, and improving actual rental income can matter as much as chasing another $10,000 in savings.

Serviceability Stress Example - $650,000 Loan Over 30 Years

| Actual Rate | Assessment Rate | Assessed Monthly P&I Repayment |

|---|---|---|

| 6.10% | 9.10% | $5,231 |

| 6.40% | 9.40% | $5,355 |

| 6.70% | 9.70% | $5,481 |

If you are preparing for another purchase, model the current repayment in the Loan Repayment Calculator, then compare it with your wider strategy using the Equity Calculator and Cash Flow Calculator. A loan serviceability calculator can give you a rough planning estimate, but lenders will still use their own assessment rate, debt shading, and living-expense model.

Common Interest-Only Loan Mistakes to Avoid

1. Treating the lower repayment as a profit boost

Lower monthly repayments are not the same as a better loan. If the cash you free up is not being directed into an offset, emergency buffer, or another high-value debt move, you may just be paying more interest for no strategic benefit.

2. Forgetting the reversion date

The risk is not the interest-only period itself. The risk is getting to the end of it without a plan. Investors who ignore the expiry date often get hit with a repayment increase at the same time rates, vacancies, or personal costs are already under pressure.

3. Making extra repayments when an offset would be cleaner

Extra repayments reduce the principal. That can be fine, but it also changes the debt balance directly. For many investors, an offset account keeps more flexibility and cleaner tax treatment.

4. Assuming interest only improves borrowing power automatically

Real cash flow may improve, but lender assessment often stays conservative. If your goal is another purchase, you still need to manage serviceability rather than assuming the lower actual repayment solves it.

5. Mixing personal and investment debt

Redrawing from an investment loan for private purposes can create messy tax outcomes. Keep the purpose of the debt clear and use separate structures where possible.

6. Not reviewing the rate every year

A stale investor rate can quietly cost thousands. Banks reward new business more than loyal borrowers, so annual repricing or refinance checks are part of good loan management, not an optional extra.

How Do You Calculate Interest-Only Loan Repayments?

The base formula is simple.

Interest-only monthly repayment = Loan balance x Annual interest rate / 12

Principal-and-interest repayment = Standard amortisation repayment across the remaining term

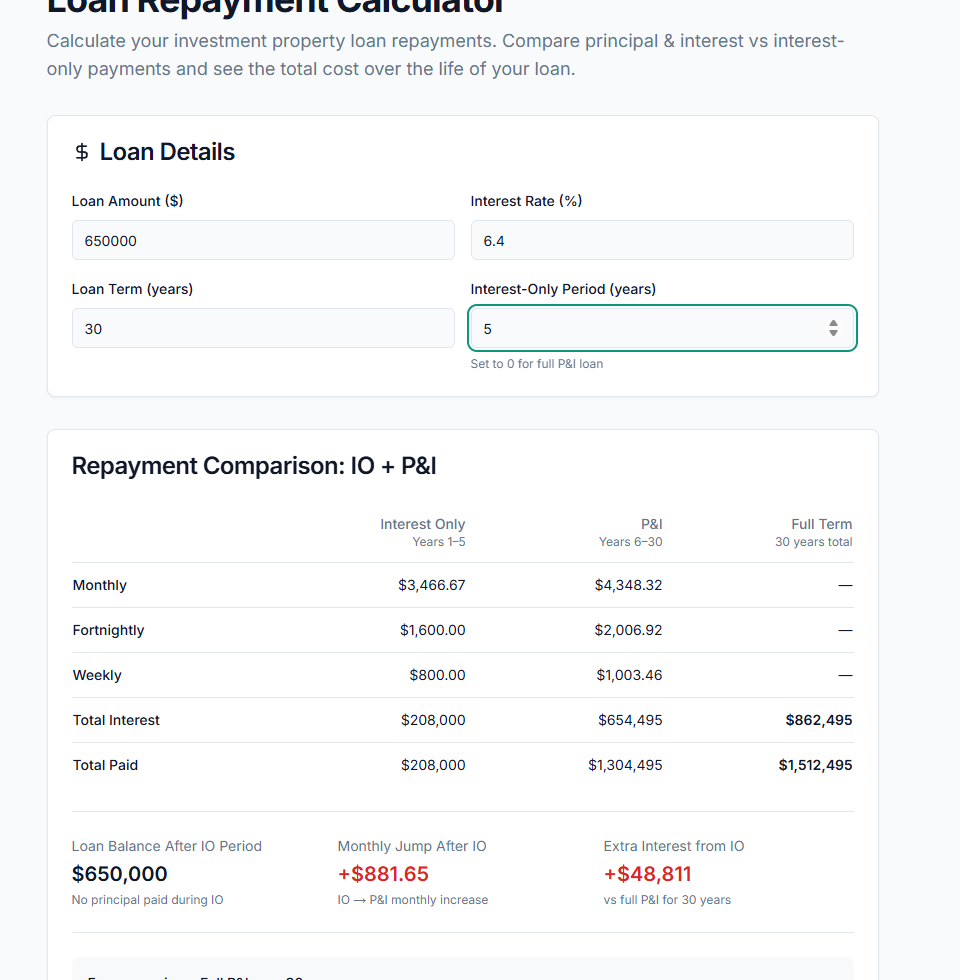

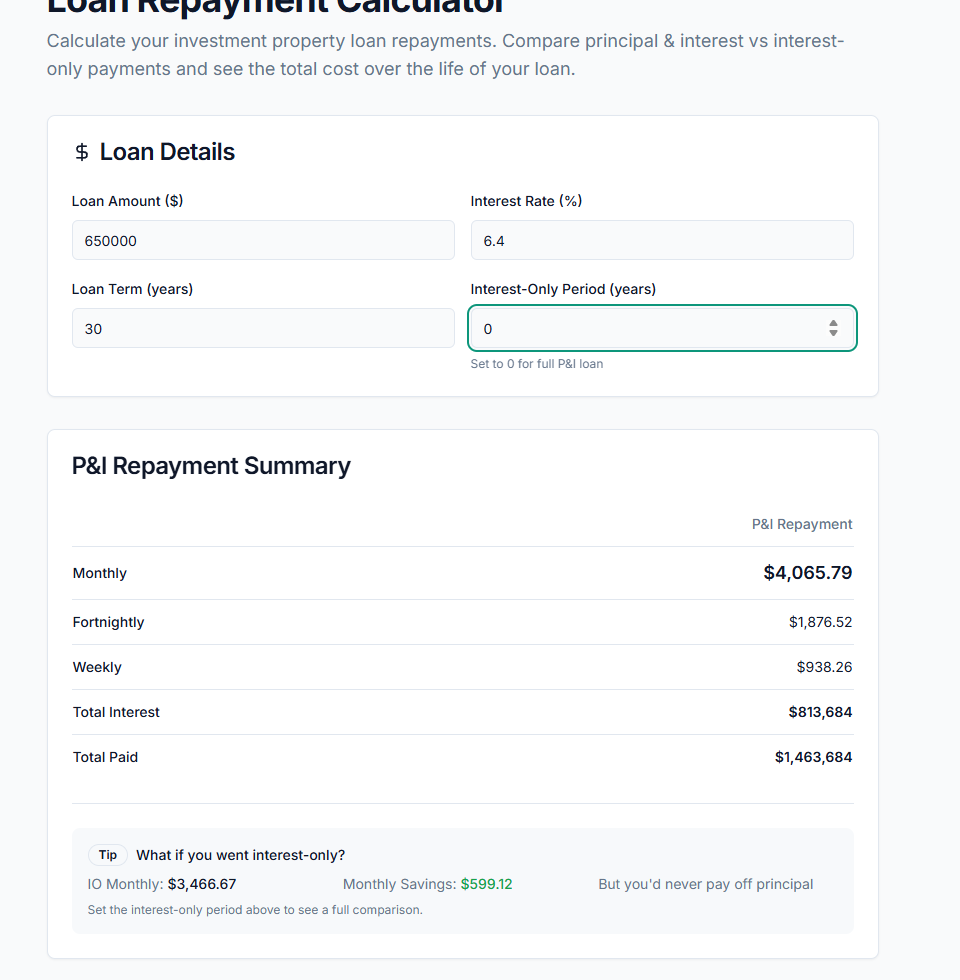

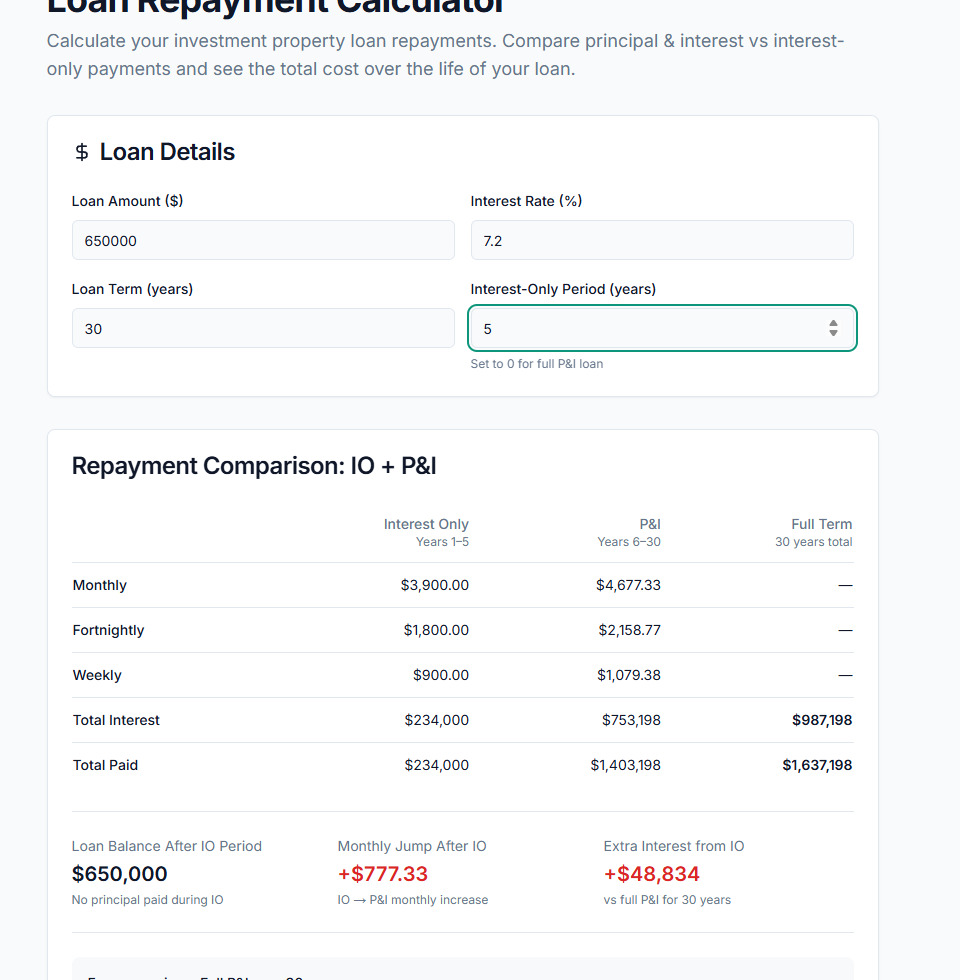

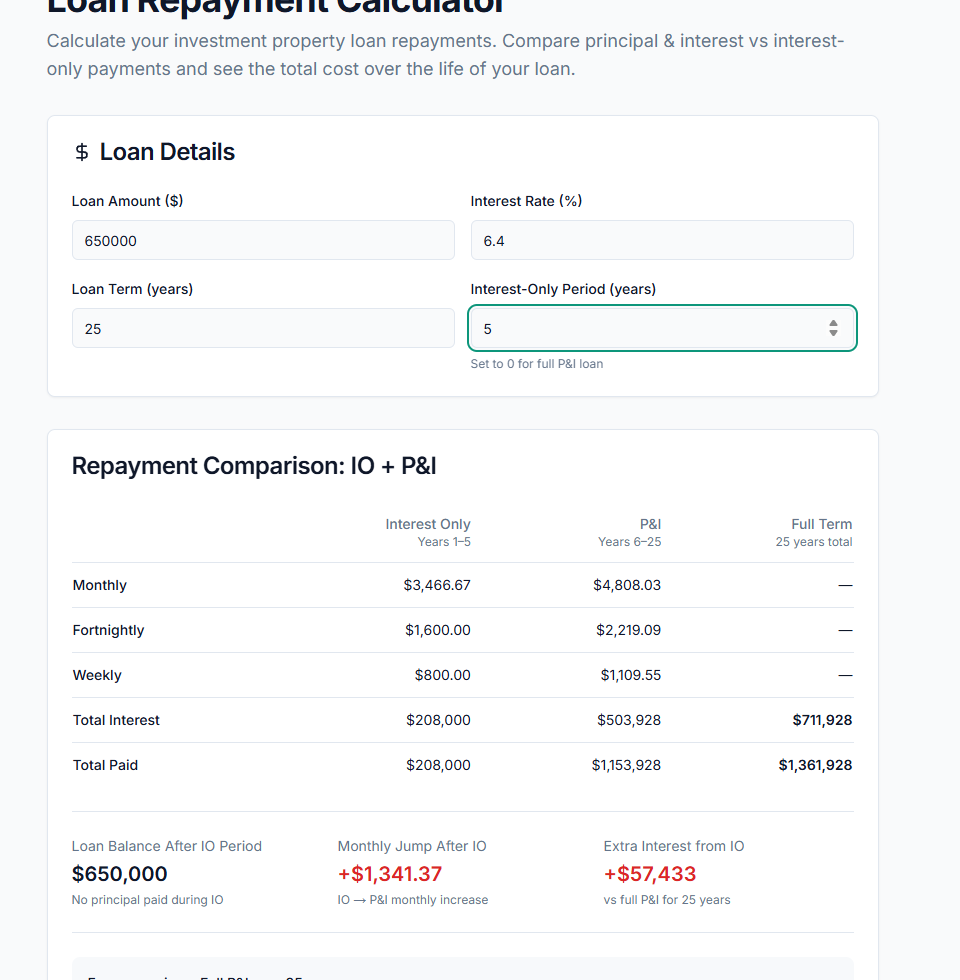

Worked Example - $650,000 at 6.40% Over 30 Years

| Step | Calculation | Result |

|---|---|---|

| Monthly interest rate | 6.40% / 12 | 0.5333% |

| Interest-only repayment | $650,000 x 0.005333 | $3,466.67 |

| Principal-and-interest repayment | 30-year amortised repayment | $4,066.69 |

| Monthly difference | $4,066.69 - $3,466.67 | $600.02 |

| Annual difference | $600.02 x 12 | $7,200.24 |

Worked Example - What Happens After a 5-Year Interest-Only Period

| Item | Amount |

|---|---|

| Starting balance | $650,000 |

| Balance after 5 years interest only | $650,000 |

| Remaining term | 25 years |

| New repayment at 6.40% on P&I basis | about $4,368/month |

| Approximate repayment jump | about $901/month |

That repayment jump is the number investors should plan around. If you cannot absorb it from rent growth, wages, or offset savings, the structure is too aggressive. If you came here looking for an interest only home loan calculator or an interest only loan repayment calculator, this is the exact comparison the PropBoss tool is designed to surface.

Read more on repayment planning in:

- Investment Loan Repayment Calculator

- Extra Loan Repayment Calculator Australia Guide 2026

- IO vs PI Investment Property Guide 2026

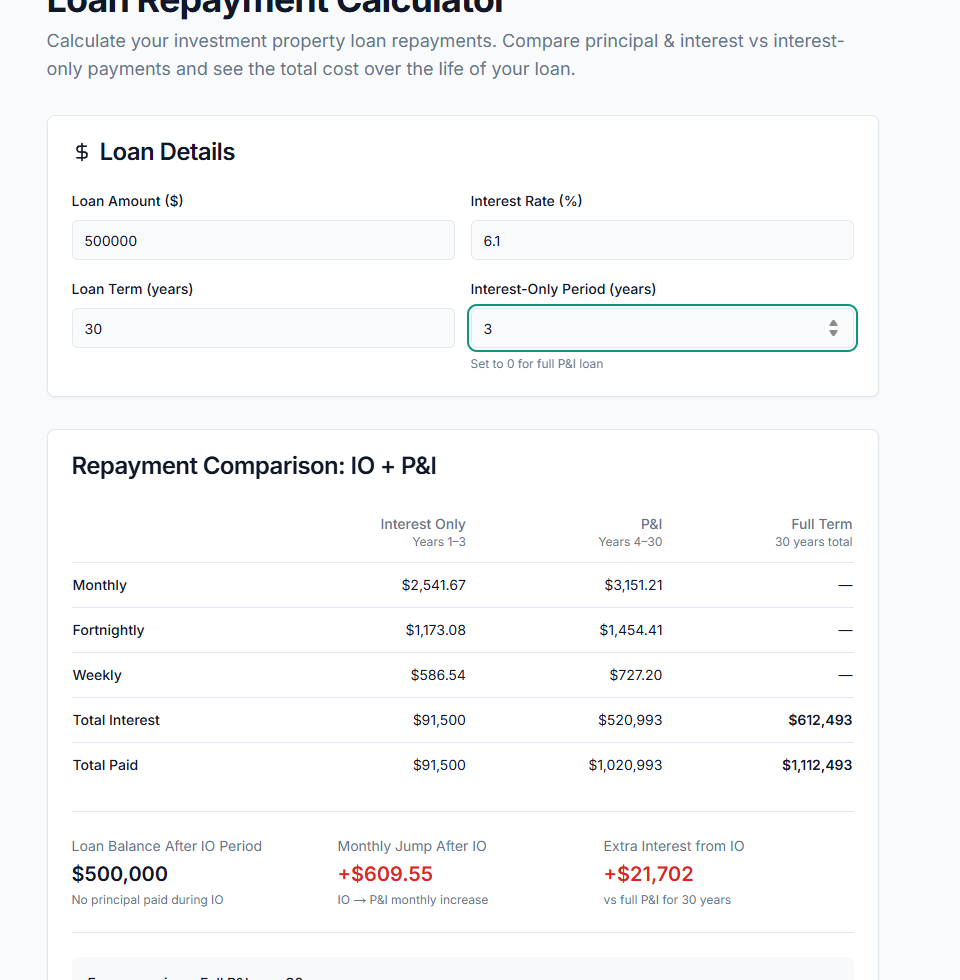

Calculator Proof Screenshots

Frequently Asked Questions

What is an interest-only home loan?

An interest-only home loan is a loan where your minimum repayment covers only the interest for a set period, commonly one to five years. During that period, the principal does not reduce, so the balance stays the same unless you make additional payments or hold money in an offset account. For investors, that lower repayment can improve short-term cash flow, but it also means you need a clear plan for what happens when the loan reverts to principal and interest.

What is principal and interest?

Principal and interest means each repayment covers both the cost of borrowing and part of the loan balance itself. That reduces the debt steadily over time, builds equity, and normally lowers total interest paid over the life of the loan. It is the cleaner long-term debt structure, but it asks more of your monthly cash flow from day one.

Interest only vs principal and interest: which is better for property investors?

It depends on the investor's job right now. Interest only is often better when you want flexibility, stronger short-term cash flow, and a larger deductible interest bill while you build buffers or pay down non-deductible debt elsewhere. Principal and interest is better when you want faster debt reduction, stronger long-term serviceability, and less exposure to reversion shock. Many investors use interest only early, then switch once the portfolio moves from growth mode to consolidation mode.

How do interest-only loan repayments work?

They are based on the outstanding balance and the current rate, without any compulsory principal reduction during the interest-only term. That keeps repayments lower, but it also means the debt itself is not shrinking. Once the term ends, the loan is usually recalculated over the shorter remaining period, which pushes the monthly repayment higher.

How do you calculate interest-only loan repayments?

A rough monthly estimate is loan balance multiplied by annual rate, divided by 12. On a $650,000 loan at 6.40%, that is about $3,466.67 per month before fees. That rough figure is useful, but investors should still compare it with a principal-and-interest repayment and the later reversion repayment in the Loan Repayment Calculator before making a decision.

What are interest-only home loan rates in Australia?

They are usually a little higher than comparable principal-and-interest rates because the lender carries more balance risk for longer. In April 2026, investors will often see interest-only rates in the mid-6% range depending on LVR, product features, and whether the loan is owner-occupied or investment. That extra margin matters, so even a 0.20% pricing difference is worth negotiating or refinancing for.

What is loan serviceability?

Serviceability is the lender's test of whether you can keep up with repayments after your income, expenses, existing debts, rental income, and credit limits are all assessed together. In practice, it is one of the biggest constraints on property investors because lenders rarely assess your loan at face value alone. They usually add a rate buffer and haircut rental income, which reduces maximum borrowing.

How does loan serviceability affect borrowing power?

It affects borrowing power by changing how much monthly debt the lender is willing to let you carry. Large card limits, short remaining loan terms, high living expenses, and other debts reduce capacity quickly. Better rent, stronger surplus income, and lower consumer debt improve it. That is why closing an unused card or clearing a personal loan can sometimes do more for your next purchase than saving a little extra deposit.

What is an investment loan repayment calculator?

An investment loan repayment calculator estimates repayments using your loan amount, rate, term, and repayment type. A good one lets you compare interest only with principal and interest, test extra repayments, and see what a rate change does to monthly cash flow. That makes it a practical decision tool rather than just a maths shortcut.

Can you make extra repayments on an interest-only loan?

Often yes, especially on variable products, but the flexibility depends on the lender and whether the loan is fixed. Investors should be careful because extra repayments directly reduce the loan balance, while an offset account reduces interest without changing the deductible principal. If tax flexibility matters, the offset route is often cleaner.

Methodology, Sources, and Review Context

This guide is general information only and should not be treated as personal credit, tax, or legal advice. The worked examples use April 2026 assumptions, current Australian investor workflows, and live PropBoss calculator outputs to show how repayment structure changes the numbers in practice.

The lender settings, serviceability treatment, rate pricing, and tax outcomes discussed here can change by bank, product, borrower profile, and financial year. Investors should confirm the final lending position with their broker or lender and the tax position with a qualified adviser before acting.

This guide was reviewed in the context of PropBoss product and investor workflows by Jonathan Zuvela, founder of PropBoss.

Track Your Loan Strategy Automatically with PropBoss

PropBoss helps investors track repayments, interest costs, offset savings, and portfolio cash flow in one place, so your loan strategy is based on live numbers instead of guesswork.

Get Started Free | Try the Loan Repayment Calculator

Related Guides & Tools

| Loan Repayment Calculator - Model interest-only, P&I, and reversion shock | Offset Calculator - See how cash parked against the loan changes your interest bill |

| Refinance Calculator - Test whether a lower rate is worth switching for | Equity Calculator - Check how much usable equity your portfolio has built |

| Cash Flow Calculator - Compare repayment choices against real property cash flow | Negative Gearing Guide - Understand how deductible interest fits into the wider tax strategy |

Model the repayment structure before you commit

Compare interest-only and principal-and-interest repayments, test repayment shock, and see how rate changes affect cash flow before the next refinance or purchase.