Interest Only vs Principal and Interest: Investment Property Guide

A complete comparison of interest only vs principal and interest loan structures for Australian property investors, with worked examples, tax implications, and when each strategy makes sense.

Interest Only vs Principal and Interest: Investment Property Guide

Choosing between an interest only home loan and principal and interest repayments is not just a repayment preference. For an Australian property investor, it changes monthly cash flow, tax deductions, lending capacity, and the repayment shock you face when the interest only term ends.

The short version: interest only can suit investors who need surplus cash, deductible interest, and flexibility. Principal and interest can suit investors who want debt reduction, lower lifetime interest, and a cleaner path to retirement.

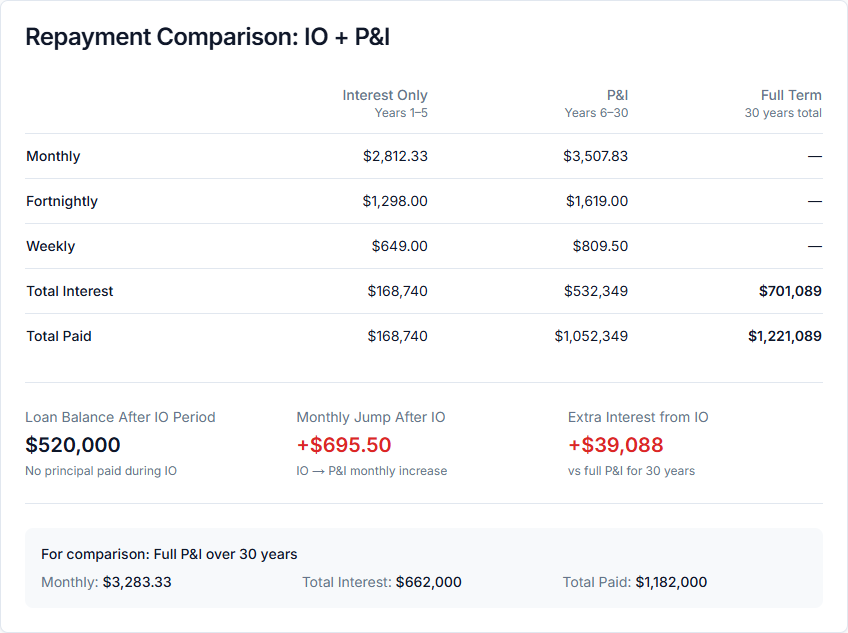

Interest Only vs P&I

What interest only means

With an interest only loan, your repayments cover only the interest charged on the loan balance during a set term. Most investor interest only periods run for 1 to 5 years, although some lenders may consider longer terms.

On a $520,000 investment loan at 6.49%, the monthly interest only repayment is about $2,812. After five years, the loan balance is still $520,000 because no principal has been repaid.

What principal and interest means

With a principal and interest loan, every repayment covers the interest due plus a principal component that reduces the debt.

On the same $520,000 loan at 6.19% over 30 years, principal and interest repayments are about $3,183 per month. After five years, the balance may fall to roughly $487,000, depending on the exact rate and repayment schedule.

Quick Repayment Comparison

Worked example assumptions

Use a $650,000 Brisbane apartment with an 80% loan-to-value ratio, giving a $520,000 loan. Compare an interest only rate of 6.49% with a principal and interest rate of 6.19%.

These are example rates for modelling, not a lender quote. Always compare the comparison rate, fees, offset rules, and refinance costs.

Monthly repayments

| Metric | Interest Only | Principal and Interest |

|---|---|---|

| Loan amount | $520,000 | $520,000 |

| Example rate | 6.49% | 6.19% |

| Monthly repayment | $2,812 | $3,183 |

| Annual repayments | $33,744 | $38,196 |

| Cash flow difference | +$371/month | Baseline |

The interest only structure frees up $371 per month, or $4,452 per year. For an investor holding two similar properties, that repayment gap becomes $742 per month.

Five-year balance

Interest only keeps the full loan balance outstanding during the IO term. Principal and interest gradually reduces the loan, so the investor may owe about $487,000 after five years.

That trade-off is the whole decision: interest only improves near-term surplus, while principal and interest improves debt reduction.

Home loan repayment checklist

Keep the home loan settings consistent when comparing repayment types: home loan amount, home loan balance, home loan interest rates, home loan fees, loan term, remaining loan term, and monthly repayments.

Compare interest only home loan repayments with principal and interest repayments over the same home loan term. If one quote uses a shorter home loan term, the repayment amount will look higher even when the rate is competitive.

An interest only home loan covers just the interest component during the set period. At the end of the interest only period, the loan reverts and you start repaying both the principal amount and interest payable.

A principal and interest loan includes both the principal and interest portion from day one. That usually means higher repayments now, but less more interest over the life of the loan.

For a clean comparison, record every existing home loan, investment loans for each property, owner occupiers' debts, variable rate offers, fixed rate loan fees, minimum repayment rules, and credit approval conditions.

Ask the lender to show the home loan rate, home loan comparison rate, home loan fees, home loan monthly payments, and home loan switching cost. For an interest only home loan, confirm interest only home loan eligibility, interest only home loan interest rates, and whether repayments change after the fixed period.

Interest Only Home Loan Rates

Rate premium

Interest only home loan rates are usually higher than principal and interest rates because the lender carries more risk when the debt is not reducing.

In 2026 investor examples, the premium is commonly around 0.20% to 0.40%. A borrower might see 6.49% for interest only and 6.19% for principal and interest on the same scenario.

Comparison rate

The advertised interest rate is not enough. A loan with a lower headline rate can cost more if it has high annual fees, package fees, discharge fees, or offset account costs.

Compare the comparison rate and model the monthly repayment using the PropBoss loan repayment calculator.

Tax Implications

Deductible interest

The ATO interest expense rules generally allow investors to claim interest on a loan used to buy an income-producing rental property.

The principal component is not deductible. That means interest only repayments can preserve a higher deductible interest amount during the interest only period.

Year one tax example

| Item | Interest Only | Principal and Interest |

|---|---|---|

| Annual interest | $33,748 | $32,100 |

| Tax value at 37% | $12,487 | $11,877 |

| Extra IO tax benefit | $610 | - |

The tax difference is not the main reason to choose interest only, but it matters when cash flow is tight or the property is negatively geared.

Negative gearing impact

Assume rent of $560 per week, or $29,120 per year. Add $33,748 of interest and $8,200 of other holding costs.

The net rental loss is about $12,828. At a 37% marginal tax rate, that loss may produce a tax benefit of about $4,746, subject to the investor's full tax position.

When Interest Only Makes Sense

Portfolio building

Interest only can suit investors planning to buy another property within 1 to 3 years. Lower repayments preserve cash for deposits, buffers, and lender servicing.

The $371 monthly saving in the worked example can be directed into an offset account instead of disappearing into mandatory principal repayments.

Non-deductible home debt

If you still have a private home loan, extra cash may be more valuable there because owner-occupier interest is usually not tax deductible.

One strategy is to keep the investment loan interest only while paying down the non-deductible home loan faster.

High tax bracket

The higher your marginal tax rate, the more valuable deductible interest becomes. An investor on a 37% marginal rate receives more tax value from each deductible dollar than someone on a lower rate.

This does not make interest only automatically better. It simply changes the after-tax comparison.

Growth-focused investing

If your strategy is capital growth, you may prefer flexibility over debt reduction in the first few years.

That only works if you have a clear exit plan before the interest only term ends.

When Principal and Interest Makes Sense

Positive rental surplus property

If rental income already covers the loan and expenses, the lower interest only repayment may not be necessary.

Principal and interest repayments can build equity faster and reduce long-term interest.

Retirement planning

Investors within 10 years of retirement often prefer reducing debt over maximising deductions.

A lower loan balance gives more options later: sell, refinance, live off rent, or reduce portfolio risk.

One-property investor

If you do not plan to buy more properties, borrowing capacity may not matter as much.

Principal and interest can be simpler because every repayment moves you closer to owning more of the asset.

Interest Only Period Ends

Repayment shock

The biggest risk is the jump when the interest only period ends. If a $520,000 loan has a 30-year loan term and the first 5 years are interest only, the remaining loan term is 25 years.

In the worked example, repayments can move from about $2,812 per month to about $3,508 per month. That is a $696 monthly increase.

Extension options

Some lenders allow a new interest only term if your loan-to-value ratio, income, expenses, and credit position still qualify.

You may also refinance, switch to principal and interest early, or build an offset buffer before the reset date.

Six-month review

Set a reminder at least 6 months before the interest only term ends. Waiting until the final month reduces your refinance and extension options.

PropBoss can help track repayment changes across multiple properties so the reset date does not become a budget surprise.

Offset Account Strategy

Why investors use offset

An offset account can reduce interest charged without reducing the investment loan balance.

If you hold $50,000 in offset against a $520,000 interest only loan at 6.49%, the interest saving is about $3,245 per year.

Offset versus redraw

Offset accounts can be cleaner for tax recordkeeping than redraw because the loan balance is not mixed by taking principal back out.

Read more in our guide to offset accounts for investment properties.

Borrowing Power

Assessment repayments

Lenders usually assess your ability to repay using principal and interest repayments, even if you apply for interest only.

They may also add a serviceability buffer above the actual interest rate. That means interest only does not automatically increase maximum borrowing capacity.

Real surplus

Even when assessed capacity is similar, real surplus is different. Lower interest only repayments can make a portfolio easier to hold through vacancies, repairs, and rate rises.

That is why the decision should include both lender servicing and your own cash buffer.

Eligibility Criteria

Common lender rules

Many lenders prefer investor interest only loans below 80% LVR. Higher LVR loans may need lenders mortgage insurance or may be declined.

They also test income, expenses, credit history, loan purpose, and whether you can afford repayments after the interest only term.

Fixed or variable

Variable interest only loans usually offer more flexibility for offset accounts, refinancing, and extra repayments.

Fixed rate loans can help with budgeting, but may limit extra repayments or create break costs if you refinance early.

Cash Flow Example

Two-property investor

Assume two investment loans of $520,000 each. Interest only repayments are about $5,624 per month combined, compared with $6,366 on principal and interest.

That $742 monthly gap can decide whether the investor can keep both properties during a vacancy or large maintenance bill.

Use your own numbers

Your numbers will depend on loan size, rent, vacancy, tax rate, fees, and expenses.

Run both repayment types in the PropBoss cash flow calculator before refinancing or applying for a new loan.

Common Mistakes

Ignoring the expiry date

Interest only is a temporary structure, not a permanent discount. The end date should be tracked from day one.

Choosing P&I by habit

Paying down debt is useful, but not always the best first priority if you have non-deductible home debt.

Chasing the lowest rate

A loan with a low rate but no offset account may be worse than a slightly higher rate with better investor features.

Forgetting annual reviews

Review the structure every year. Income, rates, rent, tax position, and portfolio goals all change.

Decision Framework

Choose interest only if

You need surplus cash, have non-deductible home debt, plan to buy again within 3 years, or hold negatively geared property.

Interest only works best when the saved cash has a clear job, such as offset savings, deposits, or debt recycling.

Choose principal and interest if

You want lower long-term interest, faster equity growth, simpler repayments, or less debt before retirement.

P&I also suits investors who are not trying to grow the portfolio further.

Frequently Asked Questions

Is interest only tax deductible?

Interest on an investment loan is generally deductible when the loan is used to earn rental income. Principal repayments are not deductible.

Can I switch from P&I to interest only?

Usually yes, if the lender approves a new assessment. You may need acceptable LVR, income, expenses, and credit history.

How long can an interest only loan run?

Many lenders offer up to 5 years at a time for investment loans, with possible extensions if you still qualify.

Does interest only increase lending capacity?

Not necessarily. Lenders commonly assess repayments on a principal and interest basis with a buffer.

Is fixed or variable better?

Variable usually offers more flexibility. Fixed can help budgeting but may restrict extra repayments, redraw, or refinancing.

Compare Your Loan Options

Calculator CTA

Use the PropBoss Loan Repayment Calculator to compare interest only and principal and interest repayments with your own loan amount, rate, and term.

Portfolio CTA

Already managing investment properties? Create your free PropBoss account to track repayments, tax deductions, and portfolio performance in one place.

For a deeper look, see our investment property mortgage rates. You can also read our investment loan repayment calculator. If you want broker-specific guidance, read our mortgage broker for investment property guide.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more