Investment Property Mortgage Rates Australia 2026: Compare & Save

A comprehensive guide to investment property mortgage rates in Australia for 2026, covering fixed and variable rates, comparison rates, interest only options, borrowing power, and strategies to secure the lowest rate on your investment loan.

Investment property mortgage rates in Australia currently sit between 6.09% and 7.50% depending on your lender, loan type, and loan to value ratio -- roughly 0.25% to 0.60% higher than owner-occupier home loan rates.

That premium might sound small, but on a $600,000 investment loan over 30 years, even a 0.30% difference adds up to more than $40,000 in extra interest.

Getting the right rate on your investment property home loan matters.

This guide breaks down what investment property mortgage rates look like in 2026, how to compare them properly using the comparison rate, and practical strategies to lock in the best investment home loan rates Australia has to offer right now.

Current Investment Home Loan Rates in 2026

Investment home loan rates have shifted considerably since the Reserve Bank of Australia began its easing cycle in late 2025.

As of April 2026, the RBA cash rate sits at 3.60% after two consecutive 25-basis-point cuts, and lenders have passed on varying portions of those cuts to investment property loan holders.

Here is what the big four banks and major non-bank lenders are currently offering on investment property home loans:

Variable Investment Loan Rates

| Lender | Variable Rate | Comparison Rate | Max LVR | Offset Account |

|---|---|---|---|---|

| CBA | 6.44% | 6.47% | 90% | Yes |

| ANZ | 6.39% | 6.41% | 80% | Yes |

| Westpac | 6.49% | 6.51% | 90% | Yes |

| NAB | 6.44% | 6.47% | 80% | Yes |

| Macquarie | 6.29% | 6.31% | 70% | Yes |

| ING | 6.19% | 6.22% | 80% | No |

| Athena | 6.09% | 6.12% | 70% | No |

| Pepper Money | 6.59% | 6.89% | 90% | Yes |

*Rates as at April 2026.

Actual rates depend on your loan amount, loan to value ratio, and credit history.

Always check with the lender directly.*

Non-bank lenders like Athena and ING offer the sharpest variable interest rates, but they come with trade-offs -- lower maximum LVR, no offset account features, and tighter serviceability requirements.

The big four banks and other major financial institutions charge a premium on their variable home loan interest rates but offer more flexible loan features and higher LVR options.

Each financial institution sets its own discounted interest rate based on your loan size, LVR, and relationship -- so the advertised rate is rarely the rate you actually pay.

Fixed Rate Investment Loans

Fixed rate home loans lock in your interest rate for a set fixed rate period -- typically one to five years.

For property investors, a fixed rate provides certainty on your home loan repayments, making it easier to forecast cash flow on your investment property.

| Fixed Rate Period | Big Four Average | Non-Bank Best | Comparison Rate Range |

|---|---|---|---|

| 1 year fixed | 5.89% | 5.69% | 6.20%-6.45% |

| 2 year fixed | 5.79% | 5.59% | 6.15%-6.40% |

| 3 year fixed | 5.94% | 5.74% | 6.18%-6.42% |

| 5 year fixed | 6.24% | 5.99% | 6.25%-6.48% |

Fixed rate loans currently sit below variable rates, reflecting the market expectation that the RBA will continue cutting.

However, when the fixed rate period expires, your investment loan reverts to the lender's standard variable rate -- which is usually higher than advertised rates.

Budget for this reversion in your financial situation planning.

Keep in mind that fixed rate loans typically don't allow extra repayments beyond a capped amount (usually $10,000-$20,000 per year), and they charge early repayment fees if you break the loan during the fixed period.

Understanding the Comparison Rate

The comparison rate is your best friend when comparing investment home loan rates across lenders.

While the advertised interest rate tells you the base cost of the home loan, the comparison rate factors in most fees and charges associated with the investment property loan -- application fees, ongoing monthly fees, and standard charges.

By law (under the National Consumer Credit Protection Act 2009), every Australian lender holding an Australian Credit Licence must display a comparison rate alongside their advertised rate.

The comparison rate is calculated on a standardised $150,000 loan over 25 years.

This means the comparison rate gives you a more accurate picture of what your home loan actually costs compared to the headline interest rate alone.

However, the comparison rate has limitations.

It does not account for features like an offset account, redraw facilities, or the ability to make additional repayments.

A home loan with a comparison rate of 6.45% but a full offset account could actually cost you less than one with a comparison rate of 6.20% but no offset -- depending on how much cash you keep in the offset.

How to Read the Comparison Rate

When comparing investment property mortgage rates, watch for these red flags:

- Big gap between rate and comparison rate: If the advertised interest rate is 6.19% but the comparison rate is 6.89%, the lender is charging significant fees. That 0.70% gap means hundreds of dollars per year in fees that the headline rate hides.

- Low comparison rate but no features: A basic variable home loan with no offset account and no redraw might show a low comparison rate, but you lose flexibility that could save more money in practice.

- Comparison rate on IO loans: The comparison rate for interest only loan products can be misleading because the calculation assumes principal and interest repayments over the full 25 years. Always compare like-for-like.

Every lender with an Australian Credit Licence is required to display comparison rates, so use them as your starting point.

But don't stop there -- model your actual costs using a loan repayment calculator with your specific loan amount, term, and repayment type.

Investment Home Loans vs Owner-Occupier Home Loans

Investment home loans cost more than owner-occupier home loans.

That is a universal truth across every lender in Australia.

The gap exists because lenders consider investment property loans riskier -- investors are more likely to default under financial pressure because the investment property is not their primary residence.

Here is how investment home loans differ from owner-occupier products:

Interest Rate Premium on Investment Loans

Investment property loan rates typically carry a 0.25% to 0.60% premium over owner-occupier rates.

On a $500,000 loan, that is $1,250 to $3,000 more per year in interest charges.

The premium applies to both variable and fixed rate products.

LVR and Lenders Mortgage Insurance

Most lenders cap investor loans at 80% LVR without lenders mortgage insurance (LMI).

Some will go to 90% LVR, but you will pay lenders mortgage insurance -- a one-off cost that can exceed $15,000 on a $600,000 property.

LMI is one of the biggest upfront costs for investor loans with high LVR, so factor this into your total borrowing cost.

You can often add the LMI premium to your loan balance, but that means you pay interest on it for the life of the loan.

Loan Features and Flexibility

Investment loans generally offer the same loan features as owner-occupier products -- offset accounts, redraw, extra repayments -- but the interest rate for each feature level is higher across the board.

Serviceability Requirements

Lenders assess your borrowing capacity more conservatively for investment loans.

They typically shade your rental income by 20-30% (assuming vacancy and expenses), meaning less of your expected rent counts toward servicing the loan.

Your debt to income ratio also comes under closer scrutiny for investment lending.

Tax Deductions on Investment Loan Interest

Unlike your home, the interest on an investment property loan is tax deductible.

This is a significant advantage -- at a marginal tax rate of 37%, a $30,000 annual interest bill effectively costs you $18,900 after the tax deductions.

This is the foundation of negative gearing, where your deductible investment property expenses (including home loan interest) exceed your rental income.

When you eventually sell, the profit is subject to capital gains tax -- but holding the property for more than 12 months gives you a 50% capital gains tax discount, which makes the long-term investment mortgage strategy even more attractive.

Interest Only Investment Loan vs Principal and Interest

One of the biggest decisions for property investors is choosing between an interest only investment loan and principal and interest repayments.

Each has distinct advantages depending on your investment strategy and financial situation.

Interest Only Repayments

With an interest only loan, you only pay the interest charges on your loan balance for a set interest only period -- usually one to five years.

You don't reduce the loan principal during this time, which means lower home loan repayments.

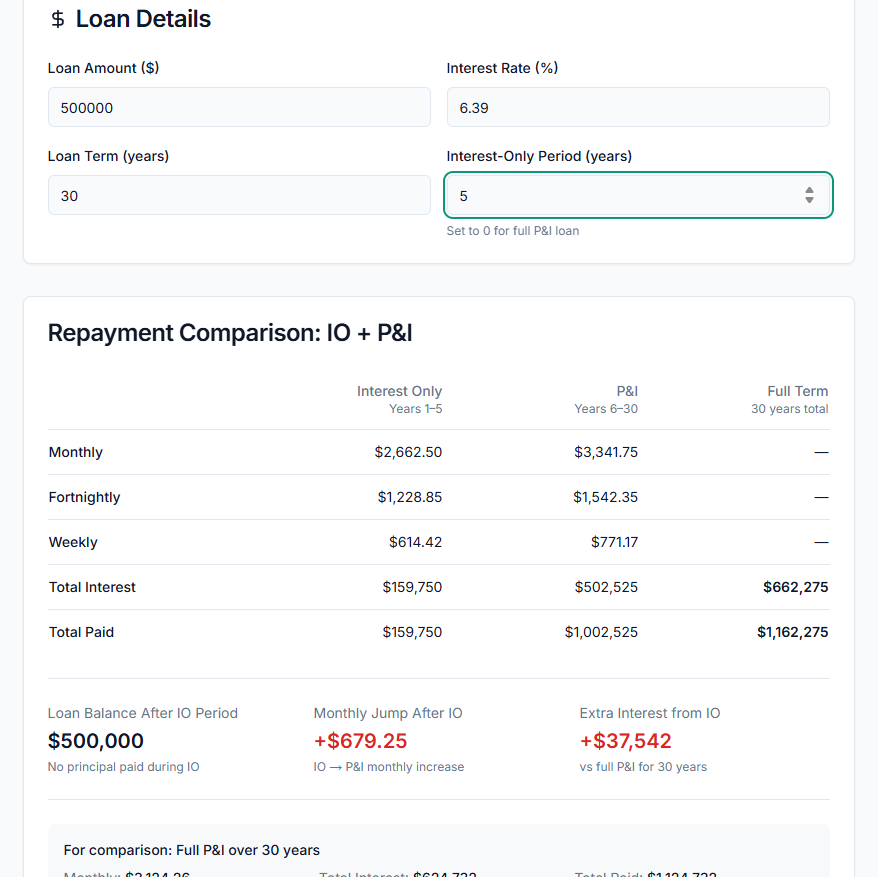

Example: On a $500,000 investment loan at 6.39%:

- Interest only repayments: $2,663/month

- Principal and interest repayments: $3,124/month

- Monthly saving: $462/month ($5,541/year)

Interest only payments make sense when you want to maximise cash flow from your investment property, keep more cash in an offset account against your owner-occupied home loan (which is not tax deductible), or when you are building a portfolio of multiple investment properties and need to preserve borrowing power.

However, interest only loans come at a cost.

The interest rate on interest only investment loans is typically 0.10% to 0.30% higher than principal and interest loans.

And when the interest only period ends, your loan reverts to principal and interest repayments calculated on the remaining term -- which means significantly higher monthly payments for the rest of the loan.

Principal and Interest Repayments

Principal and interest repayments reduce your loan balance over time, building equity in the investment property.

Your home loan repayments are higher, but you benefit from:

- Lower interest rates (lenders reward principal interest repayments with better rates)

- A reducing loan balance, which improves your loan to value ratio over time

- Faster equity growth, enabling earlier access to equity for your next property purchase

- More interest paid over the loan term with interest only loans (even though short-term payments are lower)

For most property investors, a strategy of starting with an interest only period for cash flow management, then switching to principal and interest repayments once the property is positively geared, offers the best of both approaches.

How Rental Income Affects Your Investment Loan

Your expected rental income plays a direct role in how much you can borrow for an investment property loan and which interest rates lenders will offer you.

Higher rental income improves your serviceability, potentially giving you access to better investment home loan rates.

How Lenders Shade Your Rental Income

Lenders typically assess rental income at 70-80% of the market rent -- this is called "shading." If your property rents for $600 per week ($31,200/year), the lender will count $21,840 to $24,960 toward your borrowing capacity.

The remaining 20-30% accounts for vacancy periods, property management fees, maintenance, and other investment property expenses.

Here is how rental income interacts with your mortgage at different property value levels:

| Property Value | Weekly Rent | Annual Rent (80%) | Investment Loan Rate | Annual Interest | Net Position |

|---|---|---|---|---|---|

| $500,000 | $450 | $18,720 | 6.39% | $31,950 | -$13,230 |

| $600,000 | $550 | $22,880 | 6.39% | $38,340 | -$15,460 |

| $750,000 | $650 | $27,040 | 6.29% | $47,175 | -$20,135 |

After-Tax Holding Cost Analysis

These negative positions represent the pre-tax holding cost.

After tax deductions for loan interest, depreciation, land tax, insurance, and property management fees, the actual out-of-pocket cost is substantially lower.

For example, the $500,000 property with a net position of -$13,230 before tax could have $5,000 in depreciation deductions and $2,000 in other deductible expenses, bringing the total deduction to around $20,230.

At a 37% marginal tax rate, the tax refund is approximately $7,485 -- reducing the true out-of-pocket cost to approximately $5,745 per year, or $110 per week.

Meanwhile, the property is (ideally) growing in value through capital growth, building long-term wealth.

Borrowing Power: How Lenders Assess Investment Loans

Your borrowing power -- also called borrowing capacity -- determines how large an investment loan you can obtain and directly affects which interest rates you qualify for.

Lenders assess several factors when determining your borrowing power for an investment property home loan.

Income Assessment

Lenders look at your total income from all sources: salary, rental income from existing investment properties, business income, dividends, and other regular earnings.

They then apply buffers:

- Interest rate buffer: Lenders add 2.5% to 3.0% above the current interest rate when assessing whether you can afford the home loan repayments. If the actual rate is 6.39%, they test your repayments at 8.89%-9.39%.

- Rental income shading: As mentioned, only 70-80% of rental income counts toward borrowing capacity.

- Existing debts: All existing loan repayments, credit card limits (not balances -- the full limit), HECS/HELP debts, and other liabilities reduce your borrowing power.

The Debt to Income Ratio

The debt to income ratio has become increasingly important since APRA's macroprudential guidance.

Most lenders now cap total borrowing at 6-7 times your gross annual income.

If you earn $120,000 and already have a $500,000 home loan, your remaining capacity might be limited to $220,000-$340,000 for an investment property loan, regardless of what the serviceability calculation shows.

Getting Your Investment Loan Approved

To maximise your chance of getting an investment loan approved at the best investment home loan rates:

- Reduce credit card limits -- even unused limits reduce borrowing power

- Pay down personal debts -- car loans, personal loans, and buy-now-pay-later all count against you

- Provide strong rental evidence -- a signed lease agreement or a current rental appraisal from a property manager supports your application

- Consider a mortgage broker -- a good mortgage broker who specialises in investment property lending can access over 30 lenders and negotiate rates you won't find on comparison sites. The mortgage broker's fee is typically paid by the lender (through a trailing commission), so there is usually no direct cost to you

- Keep your deposit above 20% -- a loan to value ratio of 80% or below avoids lenders mortgage insurance and gives you access to the best interest rates

How Many Investment Loans Can You Get?

A common question for property investors building a portfolio: how many investment loans can you have simultaneously?

Technically, there is no legal limit.

You can hold as many investment property loans as your borrowing power supports.

In practice, most lenders will assess each additional investment loan against your total debt to income ratio and overall serviceability.

Some lenders have internal policy limits -- for example, certain banks will only lend for a maximum of 4-6 investment properties.

Beyond that, you may need to work with specialist lenders or commercial lending divisions that understand larger property portfolios.

Each additional investment loan affects your borrowing capacity for the next one.

The key factors are:

- Rental income coverage: Does the existing rental income from your portfolio cover a reasonable portion of the loan repayments?

- Cash reserves: Lenders want to see that you can handle periods of vacancy or unexpected maintenance across multiple properties

- Cross collateralisation: Some lenders will want to cross collateralise your properties (using multiple properties as security for one loan). This simplifies their risk but limits your flexibility. Most experienced property investors avoid cross collateralisation and keep each investment property loan as a standalone facility

PropBoss handles this complexity automatically -- the portfolio dashboard tracks loan balances, rental income, and cash flow across all your investment properties in one place, so you always know your true financial position before approaching a lender for your next investment loan.

Investment Loan Features to Compare

When comparing investment home loans, don't just look at the interest rate and comparison rate.

The loan features can make a bigger difference to your bottom line over the life of the investment loan.

Offset Account

An offset account is a transaction account linked to your home loan.

The balance in the offset account reduces the loan balance that interest is calculated on.

If you have a $500,000 investment loan and $50,000 in the offset account, you only pay interest on $450,000.

For investment property owners, an offset account is particularly powerful because: - Your loan balance stays the same on paper (important for maintaining maximum tax deductions on interest) - Your actual interest charges reduce, improving your cash flow - You maintain liquidity -- the cash is accessible at any time

Not all investment home loans include an offset account.

Some lenders charge a monthly fee ($10-$15/month) for the offset account feature.

Others only offer partial offset (where only a percentage of the balance counts).

Always check whether the offset account is 100% offset with no caps.

Redraw Facility

A redraw facility lets you make extra repayments on your investment loan and then withdraw those funds later if needed.

While similar to an offset account in practice, there are important tax implications -- the ATO may consider redrawn funds as a new borrowing purpose, potentially affecting your tax deductions.

Consult your accountant before using redraw on an investment property loan.

Extra Repayments

The ability to make additional repayments without penalty is a valuable loan feature.

For variable home loans, most lenders allow unlimited extra repayments.

For fixed rate loans, extra repayments are typically capped at $10,000-$20,000 per year, with early repayment fees if you exceed the limit or break the fixed rate period.

Split Loans

A split loan lets you divide your investment property loan into a fixed rate portion and a variable portion.

This hedges your risk -- you get the certainty of a fixed interest rate on part of the loan while keeping the flexibility of a variable interest rate on the rest.

Common splits are 50/50 or 60/40 (fixed/variable).

Tips for Property Investors to Get Better Rates

Securing the best investment home loan rates requires more than just comparing headline interest rates.

Here are proven strategies that property investors use to negotiate better deals:

1. Negotiate With Your Existing Lender

Your current lender would rather keep your investment loan than lose it to a competitor.

Call your lender's retention team and ask for a rate review.

Have competitor rates ready -- if another lender is offering 6.19% and you're paying 6.49%, your lender will often match or come close.

This negotiation can save you thousands without the hassle of refinancing.

2. Consider Refinancing

If your lender won't budge, refinancing to a new lender can lock in a lower interest rate. The upfront costs of refinancing -- discharge fees, application fees, and potentially new valuation fees -- typically total $500-$1,500. If the rate improvement saves you $2,000+ per year, those upfront costs pay for themselves within months. Read our complete guide to refinancing your investment property loan for a step-by-step breakdown.

3. Increase Your Deposit or Pay Down the Loan Balance

Interest rates drop significantly at key loan to value ratio thresholds. Moving from 90% LVR to 80% LVR can save 0.20%-0.40% on your interest rate AND eliminate the need for lenders mortgage insurance. If you are close to a threshold, making extra repayments to cross it -- or bringing a larger deposit -- can unlock meaningfully better investment property mortgage rates.

4. Package Your Loans

If you have both an owner-occupier home loan and an investment property loan, packaging them with the same lender often unlocks professional package rates -- typically 0.10%-0.15% below standard rates. The annual package fee ($395-$495/year) is usually offset by the rate discount within a few months.

5. Use a Mortgage Broker

A mortgage broker with an Australian Credit Licence who specialises in investment property lending can access wholesale rates from 30+ lenders. The mortgage broker does the comparison work and handles the credit approval process for you. Because the mortgage broker is paid by the lender, there's usually no direct cost to you as the borrower.

Broker-originated investor loans frequently come with sharper rates than what you'd find by walking into a bank branch, because lenders compete for broker business with discounted interest rate offers that aren't available directly. Many investor loans sourced through brokers also come with reduced upfront costs, including waived application fees and free property valuations.

Home Loan Interest: How to Minimise What You Pay

Reducing the total home loan interest you pay over the life of your investment property loan has a massive impact on your returns as a property investor. Here are the most effective strategies:

Use an Offset Account Aggressively

Park all available cash -- rental income, salary, tax refunds -- in your offset account.

Every dollar in offset reduces your interest charges without reducing your deductible loan balance.

On a $600,000 investment loan at 6.39%, keeping an average of $30,000 in offset saves approximately $1,917 per year in interest charges.

Over 10 years, that is over $19,000 saved.

Our guide to offset accounts for investment properties breaks down the exact savings.

Make Fortnightly Repayments

Paying half your monthly repayment every two weeks results in 26 half-payments (13 full payments) per year instead of 12. That extra payment goes entirely to reducing your loan balance, cutting years off your loan term and saving thousands in interest charges on your home loan.

Review Your Rate Annually

Interest rates change constantly. Set a calendar reminder to review your investment property mortgage rates every 12 months. Even a 0.10% improvement on a $500,000 loan saves $500 per year.

Match Your Strategy to Your Loan Type

If you are negatively gearing, an interest only investment loan with maximum tax deductions might save you more (after tax) than aggressively paying down the loan principal. If you are positively geared, switching to principal and interest repayments to build equity faster could be the better move. The right approach depends on your overall investment strategy, marginal tax rate, and financial situation.

Use the PropBoss home loan repayment calculator to model different scenarios -- compare interest only vs principal and interest, fixed vs variable, and different loan terms to see the exact impact on your repayments and total interest paid. A home loan repayment calculator lets you see how even small rate changes affect your monthly payments and total interest over the life of the investment mortgage.

What About the Reserve Bank Cash Rate?

The Reserve Bank of Australia sets the official cash rate, which directly influences what lenders charge on home loan products. When the Reserve Bank cuts the cash rate, lenders typically pass on some or all of the reduction to borrowers -- though investment property loan rates tend to see slightly smaller reductions than owner-occupier rates.

As of April 2026, the Reserve Bank cash rate is 3.60%. Market forecasts suggest one to two further cuts in 2026, which would bring the cash rate to 3.10%-3.35%. If those cuts materialise and lenders pass them on, investment property mortgage rates could fall to the 5.70%-6.10% range for the best variable rate products by late 2026.

However, predicting interest rates is notoriously unreliable. The initial interest rate you lock in today is what you should base your investment decision on. Factor any potential cuts as upside rather than building them into your base financial model.

When the Reserve Bank adjusts rates, variable home loan holders see the change in their next billing cycle. Fixed rate loans are unaffected until the fixed period expires -- which is both the advantage and the risk of a fixed rate. If rates fall further, you are locked in at the higher fixed interest rate.

Eligibility Criteria for Investment Property Home Loans

Before applying for an investment property loan, make sure you meet the standard eligibility criteria that lenders assess:

- Age: Must be 18+ (some lenders have maximum age limits at loan maturity)

- Residency: Australian citizen, permanent resident, or eligible visa holder. Some lenders accept temporary residents for investment property loans at higher interest rates

- Income: Stable employment income (minimum 6-12 months with current employer) or consistent business/self-employment income (minimum 2 years tax returns for self-employed applicants)

- Credit history: Clean credit history with no defaults, judgments, or bankruptcies. Minor issues like late payments may be acceptable with some lenders at higher rates

- Deposit: Minimum 10-20% of the property purchase price. Some lenders accept 5% with lenders mortgage insurance (LMI), but interest rates are significantly higher

- Existing debts: Total debt servicing must fall within the lender's serviceability model after applying interest rate buffers and rental income shading

- Property type: Standard residential property in metropolitan or major regional areas. Rural properties, small apartments (under 50sqm), or unusual constructions may face restrictions or higher rates. Note that construction loans for building a new investment property carry different rates and terms -- they are drawn down in stages and typically revert to a standard investment mortgage on completion

Pre Approval: Lock in Your Rate

Getting pre approval for your investment loan before you start property shopping achieves two things: it confirms your borrowing capacity (so you know your budget), and some lenders will lock in the current interest rate for 60-90 days during the pre approval period. The investment home loan application process is straightforward -- your financial institution will assess your income, debts, and the property details before issuing conditional approval. This protects you if rates rise while you are searching for the right investment property.

Pre approval also signals to real estate agents and vendors that you are a serious buyer with credit approval in principle, which can strengthen your negotiating position in a competitive market.

Also read our investment loan repayment calculator.

Frequently Asked Questions

What are the current investment property mortgage rates in Australia?

As of April 2026, variable investment property mortgage rates range from 6.09% to 7.50% across Australian lenders. Fixed rate investment home loans range from 5.59% to 6.50% depending on the fixed rate period. The best rates are available to borrowers with a loan to value ratio of 80% or below and strong borrowing capacity.

Are investment property loan rates higher than owner-occupier rates?

Yes. Investment property home loan interest rates are typically 0.25% to 0.60% higher than owner-occupier rates with the same lender. This premium reflects the higher risk that lenders associate with investment lending. However, the interest on your investment property loan is tax deductible, which partially offsets the higher rate.

Should I choose a fixed rate or variable rate for my investment loan?

It depends on your financial situation and investment strategy.

Fixed rate loans offer repayment certainty and currently sit below variable rates (as of April 2026).

Variable rate home loans offer more flexibility -- including full offset account access and unlimited extra repayments.

Many property investors use a split loan to get the best of both.

Model both scenarios using a loan repayment calculator with your specific numbers.

How can I get the best investment home loan rates?

Maintain a loan to value ratio of 80% or below, keep a clean credit history, reduce unnecessary debts (especially credit card limits), and compare rates from at least three to five lenders. Using a mortgage broker with an Australian Credit Licence who specialises in investment lending gives you access to wholesale rates across 30+ lenders.

Is there a tool that automates investment loan tracking?

PropBoss tracks your investment loan repayments, interest charges, and total portfolio performance automatically. With automated bank feeds, it categorises every loan repayment, calculates your deductible interest, and generates ATO-compliant reports at EOFY -- so you don't need spreadsheets or manual tracking. Try PropBoss free to see your actual investment property loan costs in real time.

What is a comparison rate and why does it matter?

The comparison rate includes the interest rate plus most standard fees and charges on the home loan, calculated on a $150,000 loan over 25 years. It gives a truer picture of the total cost of an investment property loan than the advertised interest rate alone. Every lender with an Australian Credit Licence must display the comparison rate by law.

How many investment loans can I have?

There is no legal limit on the number of investment property loans you can hold. The practical limit is determined by your borrowing power, debt to income ratio, and each lender's internal policies. Some banks limit investment lending to 4-6 properties, while specialist lenders and commercial divisions can accommodate larger portfolios.

Take Control of Your Investment Property Mortgage

Getting the right investment property mortgage rates is one of the highest-leverage decisions you can make as a property investor. A 0.30% rate improvement on a $600,000 investment loan saves over $1,800 per year -- and that compounds as your portfolio grows across multiple investment properties.

If you want lender options compared side by side, read our mortgage broker investment property guide.

Stop managing loan tracking in spreadsheets. PropBoss automatically tracks your investment loan repayments, interest charges, and home loan performance across your entire portfolio -- with automated bank feeds and ATO-ready reporting from $1/property/month. Use the loan repayment calculator to model your next investment property loan scenario now.

*This guide is for general information only and does not constitute financial advice.

Investment property lending is regulated under the National Consumer Credit Protection Act 2009.

Lenders must hold an Australian Credit Licence issued by ASIC.

Always obtain independent financial advice tailored to your personal financial situation before making investment decisions.

Rates shown are indicative and subject to change -- confirm current rates with your lender or mortgage broker.*

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more