How to Avoid Capital Gains Tax in Australia: 9 Legal Strategies (2026)

A complete guide to legally reducing or avoiding capital gains tax on Australian investment property, with worked examples and current 2026 ATO rules.

How to Avoid Capital Gains Tax Australia: 9 Legal Strategies for Property Investors

You can legally avoid or significantly reduce capital gains tax (CGT) on property in Australia by using strategies like the 50% CGT discount, the main residence exemption, and the six year rule. The key is planning ahead -- most Australians pay more CGT than they need to because they sell without considering the timing, cost base additions, or concessions available to them.

Whether you're selling an investment property, renting out a former home, retiring, or dealing with a relationship breakdown, the ATO's CGT guidance allows legitimate ways to reduce the capital gains tax you pay when the rules are applied correctly.

The 50% CGT Discount -- How Capital Gains Tax (CGT) Rewards Patient Investors

The simplest way to reduce capital gains tax on investment property is holding the asset for at least 12 months before you sell. Individuals and trusts can receive a 50% discount on capital gains, while complying super funds receive a 33.3% discount.

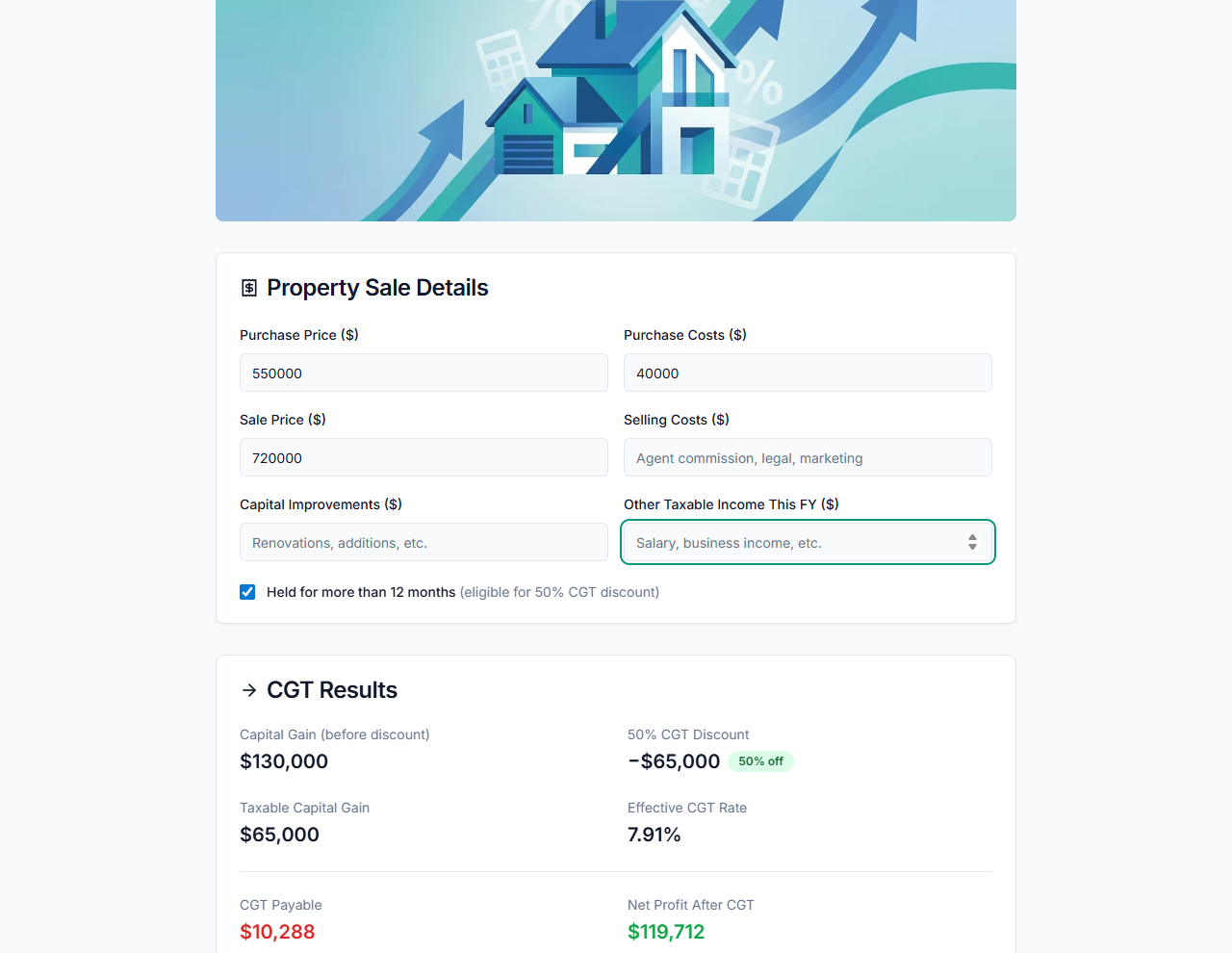

How the CGT Discount Works

The CGT calculation is straightforward: subtract your cost base from the sale price to determine gross profit, then apply the discount.

Worked example:

| Item | Amount |

|---|---|

| Purchase price (2019) | $550,000 |

| Sale price (2026) | $720,000 |

| Cost base (including costs) | $590,000 |

| Gross capital gain | $130,000 |

| 50% CGT discount applied | $65,000 |

| Taxable capital gain added to income | $65,000 |

| Tax payable (at 37% marginal rate) | $24,050 |

Without the discount, you'd pay $48,100 -- so the holding period saves $24,050 in this example. The 12 months is measured from the contract date of purchase to the contract date of sale, not settlement dates.

Main Residence Exemption -- Avoid Capital Gains Tax Completely

Your main residence -- your primary place of living -- is generally exempt from CGT entirely. This is the most powerful way to avoid capital gains tax in Australia.

Eligibility Criteria for the Main Residence Exemption

Your home is generally completely exempt from capital gains tax for the entire period you lived there, provided it wasn't used to earn rental income and sits on land of 2 hectares or less.

You must prove you lived there as your main residence -- evidence includes utility bills, electoral roll registration, and mail delivery records.

If a property has been both a main residence and an investment property, a partial exemption may apply, calculated based on the time it was used for each purpose. The market value at the time you first rented it out becomes relevant to the CGT calculation.

The Six Year Rule -- Avoid Capital Gains Tax on Investment Property

The six-year rule allows homeowners to treat their property as their main residence for tax purposes for up to six years after moving out and renting it, thus exempting them from capital gains tax on the property when they sell.

How the Six Year Rule Applies

If you lived in a home as your main residence, then after moving out started renting it, the following applies:

- Keep renting the rental property for up to six years while the CGT concession applies

- Move back into your home at any time to reset the clock

- Continue to claim deductions like interest, depreciation, and repairs -- these tax deductions still apply while the property earns investment income

This works powerfully for property investors deciding whether to sell or keep renting. If you've been renting out your former home for under six years, you may pay no CGT and keep all profit.

Important: You can only nominate one property as your main residence at a time. Overlap of up to 6 months is allowed when buying a new home. Read our complete guide to the CGT 6 year rule for more detail.

Partial CGT Exemption Under the Six Year Rule

If you've been renting the property for more than six years, CGT kicks in only on the gain beyond the six year window. Move back in at any time to reset the clock and start a new six year period.

The ATO calculates CGT based on the rental period exceeding six years relative to total ownership. You can only claim one property as your main residence at any given time.

Increase Your Cost Base to Reduce Capital Gains

Your cost base isn't just what you paid -- it includes costs for acquiring, holding, and improving the property. A higher cost base means a lower capital gain and less CGT to pay.

If you're not eligible to use the six year rule, you might be able to reduce your capital gains by having your property valued before renting it out. This allows you to calculate your cost base using the market value at the time it is first rented rather than the original amount you paid.

What Counts Toward Your Cost Base?

You can add these costs to your cost base:

- Purchase costs: stamp duty, conveyancing, inspections

- Capital improvements: renovations, extensions, fencing (not repairs)

- Holding costs: interest, council rates, land tax (only if not earning rental income)

- Selling costs: agent commissions, marketing, solicitor fees

Example: You bought a Brisbane investment property for $500,000. Adding $22,000 in stamp duty, $3,000 in solicitor fees, $45,000 in capital improvements, and $18,000 in selling costs brings your cost base to $588,000. On a $700,000 sale, your profit drops from $200,000 to $112,000 -- and that's before the 50% CGT discount.

Keep receipts for every capital expense. The ATO requires proof for each cost base addition if audited.

Use our Capital Gains Tax Calculator to estimate your CGT liability with all cost base adjustments included.

Offset Capital Gains with Capital Losses

Losses from selling assets below their cost base can offset capital gains -- either in the same year or carried forward to future years. This approach is called tax-loss harvesting, and the losses must be applied before the CGT discount.

How Tax-Loss Harvesting Works

How it works:

- Losses apply against capital gains before the 50% discount

- You must apply losses to gains in the same year first

- Unapplied losses carry forward until you have gains to offset

- You cannot use losses to reduce other types of taxable income like salary

Example: You sell a rental property with a $150,000 capital gain. You also sold shares at a $40,000 loss. Your net gain is $110,000. After the 50% CGT discount: $55,000 added to your tax return at your marginal tax rate.

Time Your Sale Strategically to Reduce CGT Impact

When you sell affects how much CGT you pay because capital gains are added to your assessable earnings for that tax year. Making a sale when your earnings are low means a lower marginal tax rate on the profit.

Sell in a Low-Income Year

Time the sale for a year when you're between jobs, retired, on parental leave, or have significant depreciation tax deductions reducing taxable amounts. These life events create windows where you pay CGT at a lower tax rate.

If your earnings are $40,000 and you add a $60,000 capital gain (after the 50% discount), you'll pay the 32.5% rate. But if your earnings are already $150,000, that same gain attracts 45% plus the Medicare levy.

CGT applies at the contract date (when you exchange), not settlement. Timing the sale of your property around the June/July boundary matters -- selling in June means the gain hits this year's return, while waiting until July defers it by 12 months.

Selling your asset at the start of the financial year gives you a further 12 months to implement any capital gains reduction strategies before your next return is due, allowing you to hold onto the money and invest it before needing to pay tax.

Use Superannuation to Minimise Capital Gains Tax

Assets held in a self-managed super fund (SMSF) attract a 10% CGT rate in accumulation phase when held over 12 months, compared with a personal marginal tax rate of up to 45%. In pension phase, SMSF property gains can be CGT-free.

You can build your super balance through salary sacrifice or concessional contributions to fund a property purchase inside the SMSF. SMSF compliance costs commonly run $2,000-$5,000 per year.

The property must meet the sole purpose test, you cannot live in it, and borrowing rules are strict.

Family Trusts and the CGT Discount

Holding an investment property in a discretionary family trust lets you distribute capital gains to beneficiaries in lower tax brackets. The CGT discount applies to trusts, unlike companies, and gains can be distributed to adult children or retirees.

Setup costs run $1,500-$3,000 with $1,000+ annual compliance, so weigh the CGT savings against the structure cost.

Pre-CGT Assets -- Complete CGT Exemption

Assets acquired before September 20, 1985, are generally exempt from capital gains tax in Australia. If you acquired property before this date, you don't pay CGT regardless of the profit you make when you sell.

For inherited properties, a pre-1985 main residence can remain CGT-free if the beneficiary sells within two years or does not use it to earn rental income after inheritance.

Calculate Your Capital Gains Tax Liability

Before making the decision to sell, calculate your actual CGT position. Our Capital Gains Tax Calculator lets you model different scenarios -- apply the 50% discount, offset losses, and see how timing the sale affects your profit.

Frequently Asked Questions

Do Retirees Pay Capital Gains Tax (CGT) in Australia?

Yes -- retirees pay CGT on investment property sales like any other Australian resident. However, retirees often pay less because retirement is one of those life events where earnings are lower, meaning the gain is taxed at a lower marginal tax rate.

Retirees benefit from the tax-free threshold ($18,200) and lower brackets. If your only earnings are from the capital gain, you'll pay significantly less than someone on a full salary.

The exception is property held within an SMSF in pension phase -- these sales are completely CGT-free, and you keep all profit.

How to Avoid Capital Gains Tax on Rural Property

The main residence covers land up to 2 hectares (5 acres). For larger rural properties, only a partial exemption can apply to the dwelling and adjacent land.

Small business CGT concessions may also apply if you're an active farmer meeting asset thresholds. Subdivision creates separate CGT events for each lot sold.

CGT rollover relief can defer capital gains tax when property transfers after a relationship breakdown or business restructure. Small business CGT concessions can also reduce or eliminate CGT for eligible business owners disposing of active assets.

How to Avoid CGT: Key Strategies Compared

| Strategy | CGT Reduction | Best For |

|---|---|---|

| 50% discount (hold 12+ months) | 50% of gain | Everyone |

| Main residence | 100% exempt | Owner-occupiers |

| Six year rule | Up to 100% | Homes being rented |

| Increase cost base | $10K-$100K+ | Renovators |

| Capital losses | Dollar-for-dollar | Portfolio investors |

| Time your sale | 10-20% rate saving | Pre-retirees |

| SMSF | 10% or 0% in pension | High-value assets |

| Family trusts | Variable | Mixed-income families |

| Pre-CGT | 100% exempt | Pre-1985 assets |

Start Planning to Reduce Your Capital Gains Tax

The most effective CGT strategies apply when you plan years ahead -- not when you're already making the sale. Your next steps: For a deeper look, see our capital gains tax on rental property.

- Calculate your estimated CGT liability using PropBoss's free calculator

- Review your cost base -- gather receipts for all capital improvements and purchase costs

- Check the 6 year rule if you once lived in your investment property

- Read our complete guide to CGT on property for the full picture

PropBoss helps Australian property investors track costs, calculate gains, and make informed decisions. Get started free and see how each strategy applies to your property portfolio.

General information only, not financial or tax advice.

For a deeper look, see our avoid capital gains tax on inherited property.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more