How to Avoid Capital Gains Tax on Inherited Property (2026)

A practical guide to CGT on inherited property in Australia -- covering exemptions, the two-year rule, cost base calculations, and strategies to legally minimise your tax bill.

How to Avoid Capital Gains Tax on Inherited Property in Australia

Inheriting property in Australia doesn't trigger capital gains tax (CGT) -- but selling that inherited property almost certainly will, unless you qualify for specific exemptions. Australia has no inheritance or estate taxes, so the tax implications arise when you sell the property, not when you receive it.

Here is the part most families miss: the first tax decision is usually a timing decision, not a clever structure. If the Australian residential property qualifies and you sell within two years, the CGT problem may disappear. These CGT rules are simple on paper but unforgiving in practice.

When Is Capital Gains Tax Payable on Inherited Property?

You normally pay tax on inherited property when something happens to the title: you sell, transfer ownership, or gift the property. The answer then comes back to a few plain facts: when the deceased bought it, whether it was their home, and how quickly the estate deals with it after death.

Pre-CGT assets (acquired before 20 September 1985): The property's cost base resets to market value at date of death. If your parent bought a house in 1975 and it was worth $850,000 when they died, the deceased's cost base becomes $850,000 -- sell for $900,000 and you'd pay CGT on only $50,000.

Post-CGT assets (acquired after 20 September 1985): You inherit the deceased's original purchase price as your cost base, plus [stamp duty](/glossary/stamp-duty), legal fees, and capital improvements. A rental property purchased for $220,000 in 1995 and sold for $680,000 in 2026 could produce a capital gain of $460,000 before the CGT discount.

The 20 August 1996 threshold: For properties the deceased acquired between 20 September 1985 and 20 August 1996, the main residence exemption applies even if the property was used to produce income -- a more generous rule than assets acquired after that date.

The Two-Year Rule: A Full CGT Exemption

If you want to avoid paying CGT on inherited property, the two year rule is your best friend. When the deceased person's property was their main residence (or a pre-CGT asset) and you sell within two years of the deceased's death, you walk away paying zero capital gains tax (CGT). No partial calculation, no apportionment -- full exemption.

To be eligible, the inherited property must have been the deceased's main residence, it wasn't producing income at the date of death, and you sell it within two years. Be warned: renting out inherited assets immediately after the deceased's death can disqualify you from this exemption.

If probate drags on or the family cannot agree on a sale, do not assume the two-year deadline is automatically lost. The legal personal representative of the deceased estate can ask the ATO for more time, but the request needs a clear written explanation and evidence of what caused the delay.

Main Residence Exemption for Inherited Property

Even if you don't sell within two years, you may still be eligible for a full or partial CGT exemption depending on the property's use.

Full CGT exemption applies when the property was the deceased's main residence for the entire ownership period, was never used to produce income, and sits on 2 hectares or less. The beneficiary must also not use it to produce income before selling.

Partial CGT exemption applies when the property was a main residence for only part of the ownership period. Say the deceased lived in it for 10 years then rented it out for 5 -- you'd pay CGT on the income-producing portion only. The 6-year CGT rule may also apply if the deceased moved out and rented the property within six years.

Understanding Cost Base and Market Value

Your cost base directly determines your CGT liability. The formula: capital gain = sale price minus cost base minus selling costs. Your cost base includes:

- Original purchase price (or market value at date of death for pre CGT assets)

- Stamp duty and transfer duty costs

- Legal fees for both purchase and estate settlement

- Capital improvements -- renovations, extensions, structural repairs (not maintenance)

- Building inspections, survey costs, and title searches

For pre-CGT assets, obtain a professional valuation at the date of death -- this provides a defensible cost base for calculating your CGT obligations.

Keep records of all capital improvements and any income-producing use. A $45,000 kitchen renovation or $28,000 deck addition reduces your capital gain. Include these on your tax return when you lodge.

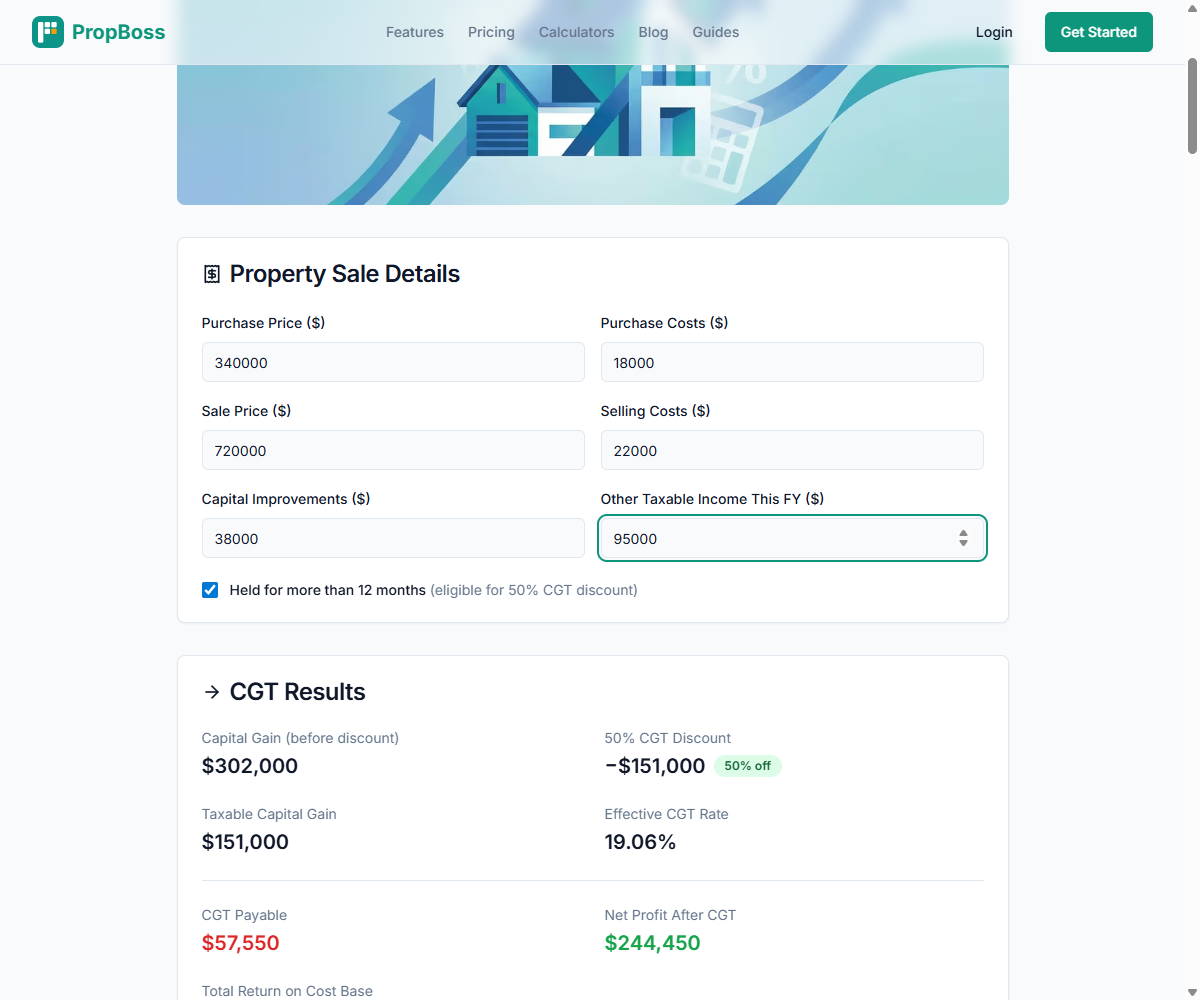

Worked Example: Calculating CGT on an Inherited Property

Sarah inherits her mother's investment property in Brisbane. Here's how to calculate the costs:

| Item | Amount |

|---|---|

| Original purchase price (2003) | $340,000 |

| Stamp duty at purchase | $11,200 |

| Kitchen renovation (2015) | $38,000 |

| Legal fees (purchase + estate) | $6,800 |

| Total cost base | $396,000 |

| Sale price (2026) | $720,000 |

| Selling costs (agent, marketing) | $22,000 |

| Net capital gain | $302,000 |

| 50% CGT discount (12+ months) | -$151,000 |

| Taxable capital gain | $151,000 |

With taxable income of $95,000, the $151,000 is added on top. The 2025-26 tax brackets make a significant difference:

- $95,001-$135,000 at 30%: $12,000

- $135,001-$190,000 at 37%: $20,350

- $190,001-$246,000 at 45%: $25,200

- Total CGT costs: $57,550 -- an effective rate of 19.06%

Use the PropBoss Capital Gains Tax Calculator to calculate your own numbers.

CGT on Inherited Investment Property

The tax outcome is different when you inherit an Australian property that was producing rental income as an income stream at the time of death -- specifically an inherited investment property where the deceased person's estate passes on different tax obligations. See our complete guide to CGT on property for a broader overview. CGT applies differently for inherited investment properties:

- No two year rule -- the property was income-producing, so the full exemption doesn't apply

- No main residence exemption -- it wasn't the deceased person's home

- You inherit the deceased's cost base (for post-CGT assets)

- The 50% CGT discount applies if the combined holding period exceeds 12 months

If the property was partly owner-occupied and partly rented, a partial exemption applies. Keep evidence of when the property shifted between uses so you calculate the correct profit.

Joint Ownership and Inherited Property

When inherited property is held between siblings or other beneficiaries, each person owns a proportional share and pays CGT on their portion individually. Foreign beneficiaries cannot claim the 50% CGT discount and may have withholding obligations.

If two siblings inherit equally and sell the property for a $300,000 profit, each reports a $150,000 capital gain. Each can claim the 50% CGT discount independently, and each person's marginal tax rate determines the tax outcome. One sibling might pay significantly more depending on their other income.

Strategies to Avoid Capital Gains Tax on Inherited Property

Sell the Property Within Two Years

If the inherited property qualifies (main residence or pre-CGT asset), selling within two years of death eliminates capital gains tax entirely. Weigh any expected price growth against the CGT liability you'd cop by waiting.

Move Into the Property as Your Main Residence

If you don't want to sell the property within two years, consider moving in as your primary home. Once it's genuinely your main residence, the exemption extends to your ownership period -- potentially making it CGT-free well beyond two years.

Maximise Your Cost Base to Reduce CGT

Gather every receipt for capital improvements the deceased made. Check with their accountant for depreciation schedules -- they often contain records of capital works costs you can add to the cost base. You'd be surprised how much this can knock off your CGT bill. Keep all records for at least five years after selling.

Time the Sale and Claim the 50% Discount

CGT is added to your taxable income, so selling in a lower-income year reduces the marginal rate. The 50% CGT discount applies automatically when the combined holding period exceeds 12 months. Note: the discount is not available to companies or foreign residents.

Watch the $750,000 Withholding Threshold

If the inherited property sells for $750,000 or more, the buyer must withhold 15% under foreign resident withholding rules -- even if you're Australian. Apply for an ATO clearance certificate before settlement to avoid having funds withheld.

PropBoss helps manage this automatically -- the portfolio dashboard tracks your cost base, capital improvements, and estimated CGT across all your investment properties so you can plan ahead and calculate your obligations before tax time.

When to Seek Professional Advice on Property Inheritance

Inherited property can get messy quickly, particularly when siblings disagree, the home was rented for part of the ownership period, or a trust sits in the middle. Paid advice is usually cheaper than guessing. A good tax accountant can test the exemption, check the timing, and stop you paying tax on a gain that should have been reduced.

Seek professional advice when:

- The property includes both income-producing and private-use periods

- Multiple family members are making decisions about the estate

- You're considering trusts to manage the inheritance

- Estate administration delays are affecting the two year deadline

- You need help understanding pre-CGT asset eligibility

FAQs About Capital Gains Tax on Inherited Property

Do You Pay CGT When You Inherit a Property?

No. You don't pay capital gains tax on inherited property when you receive it. Australia has no inheritance tax. That distinction helps families plan timing and manage costs.

How Long Do You Have to Sell Inherited Property to Avoid CGT?

Two years from the date of death. If the property was the deceased person's main residence and wasn't producing income, selling within this two year period provides a full CGT exemption.

See the ATO inherited assets guide and main residence exemption rules for more information.

Is There a Tool That Automates CGT Tracking for Investment Properties?

Yes. PropBoss helps you manage and calculate capital gains tax across all your investment properties with automated bank feeds, cost base tracking, and ATO-compliant reporting. It records capital improvements as you make them and provides real-time CGT estimates -- so you don't need spreadsheets when it's time to sell the property.

Start Tracking Your Property Portfolio's CGT Position

Stop managing spreadsheets. PropBoss tracks depreciation, cost base, and CGT automatically across your portfolio. Try the free Capital Gains Tax Calculator to calculate your CGT now, or sign up from $1/property/month.

Written by Jonathan Zuvela, Founder of PropBoss. Last updated: April 2026. This article gives general information only; get personalised advice for your situation.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more