Can I Afford an Investment Property? A Complete Guide for 2026

A practical guide to working out whether you can afford an investment property in Australia, covering deposit requirements, borrowing power, ongoing costs, and strategies to get started sooner.

Can I Afford an Investment Property? A Complete Guide for 2026

You can probably afford an investment property sooner than you think — but only if you understand the full picture of what it actually costs. Most Australians overestimate the deposit they need and underestimate the ongoing expenses that determine whether an investment property builds wealth or drains your savings.

This guide breaks down every cost, from the deposit and stamp duty to the monthly repayments and property management fees. By the end, you'll know exactly where you stand and what steps to take next.

How Much Deposit Do You Need to Buy an Investment Property?

The minimum deposit required for an investment property in Australia is typically 10% of the purchase price, though most lenders prefer 20%.

If you buy a $500,000 investment property with a 10% deposit ($50,000), you'll pay Lenders Mortgage Insurance (LMI) — a one-off fee that protects the lender if you default. LMI at 90% LVR typically costs $8,000 to $12,000. To avoid LMI, you need a 20% deposit ($100,000 on a $500,000 property).

Deposit options at a glance:

| Deposit % | Amount on $500K | LMI Cost | Monthly Repayments (6.2% IO) |

|---|---|---|---|

| 10% | $50,000 | $8,000-$12,000 | $2,325/mo |

| 15% | $75,000 | $3,000-$5,000 | $2,163/mo |

| 20% | $100,000 | $0 | $2,067/mo |

Some lenders accept deposits as low as 5% for investment properties, though interest rates and LMI costs increase substantially at higher LVR levels.

Using Your Existing Equity to Buy an Investment Property

If you already own a home, your equity could fund the entire deposit — and sometimes even the buying costs.

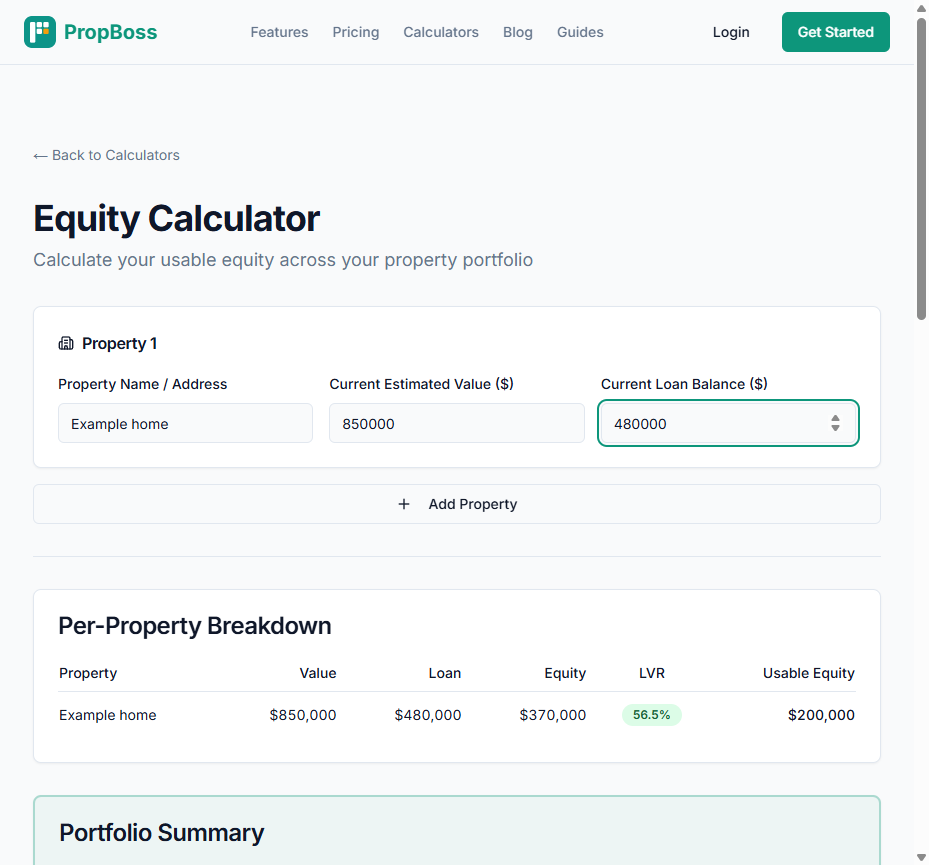

Equity is the difference between your property's current market value and what you still owe on your home loan. For example, if your home is worth $800,000 and you owe $450,000, you have $350,000 in equity. Lenders typically let you access up to 80% of your property's value minus your loan balance — so in this case, about $190,000 in usable equity.

That $190,000 is more than enough to cover a 20% deposit plus buying costs on an investment property up to $750,000, without touching your savings account.

To access your existing equity, you'll need to either refinance your current home loan or set up a separate investment loan facility. Talk to a mortgage broker who specialises in investment lending — they can structure the loans to maximise your tax deductions and keep your borrowing costs low.

Use our equity calculator to find out exactly how much usable equity you have right now.

How to Calculate What You Can Borrow for a Property Investment

Determining if you can afford an investment property requires assessing your cash flow, existing debt, and available equity. Lenders will evaluate your income, debt, and credit history to determine borrowing capacity. A strong credit score is crucial for obtaining better interest rates and access to loan products. A Debt-to-Income (DTI) ratio of 36% or lower is typically desirable for lending approval.

Under APRA's serviceability rules, lenders add a buffer of at least 3% on top of the actual rate. If the current investment loan rate is 6.2%, the bank assesses whether you can afford repayments at 9.2%.

A household earning $150,000 with a $400,000 existing mortgage can typically borrow $400,000 to $550,000 for an investment property — but this varies between lenders. Use our loan repayment calculator to run the numbers at both rates.

The Real Costs of Buying an Investment Property

The purchase price is just the starting point. Hidden upfront expenses can add 5-7% to the purchase price of a property, including stamp duty and legal fees. Understanding the various costs associated with owning and managing an investment property is critical before you commit.

On a $550,000 investment property in NSW, your upfront costs look like this:

- Stamp duty: $20,797 — stamp duty is a state government tax based on the property's value, which can significantly add to upfront costs

- Conveyancing and legal fees: $2,300-$4,000

- Building and pest inspection: $500-$800

- Loan application and registration fees: $300-$1,100

Total buying costs: approximately $24,000-$26,700 on top of your deposit. Use the stamp duty calculator to get the exact figure for your state — rates vary significantly across Australia. You should also budget for landlord insurance, which typically costs $1,200-$2,000 per year and covers building damage, liability, and loss of rental income. Land tax may apply depending on your state and the total value of your investment properties — thresholds and rates differ significantly between states.

Ongoing Expenses That Affect Your Property Investment Cash Flow

The real test of affordability isn't whether you can buy the property — it's whether you can hold it comfortably month after month. Ongoing expenses for an investment property include council rates, property management fees, landlord insurance, water rates, and maintenance. These costs can quickly add up and significantly impact your overall investment returns.

Here are the typical ongoing expenses you'll pay for a $550,000 investment property renting at $550 per week ($2,383/month). Tenants pay rent, but as the owner you pay everything else:

| Expense | Monthly Cost |

|---|---|

| Loan repayments (6.2%, IO, 80% LVR) | $2,273 |

| Property manager fees (7.5% + GST) | $197 |

| Council rates | $150 |

| Water rates | $75 |

| Strata fees (if applicable) | $300 |

| Landlord insurance | $100 |

| Maintenance and repairs | $200 |

| Total monthly expenses | $3,295 |

With rental income of $2,383/month, you're looking at a monthly shortfall of approximately $912. That's the cash you need to fund from your own pocket each month before tax deductions. Property management fees are typically charged at 7-10% of rental income plus GST, and you should also factor in vacancy periods — most properties experience 2-4 weeks without tenants each year, which adds to your annual costs. Property depreciation can offset some of these expenses at tax time, with newer properties offering the highest deductions through Division 40 (plant and equipment) and Division 43 (capital works) allowances.

After claiming tax deductions for interest, depreciation, and expenses, the actual out-of-pocket cost on a $120,000 salary drops to roughly $450-$550 per month. That's the number that determines whether you can hold the investment property over time. The good news: as tenants pay more rent each year and your expenses stay relatively flat, the gap narrows over time.

Using a Guarantor Loan to Buy an Investment Property with No Deposit

You can't buy an investment property with literally no money, but a guarantor loan comes close.

A family member (usually a parent) uses equity in their own property to guarantee part of your loan. This eliminates the need for a cash deposit and avoids LMI entirely. The guarantor doesn't hand over money — they provide their property as additional security until you've built enough equity to release them.

Guarantor loans for investment properties are available from several major lenders, though criteria are stricter than for owner-occupied purchases. The main risk is for the guarantor — if you default, the lender can claim against their property. Get independent legal and financial advice before proceeding.

Getting Home Loan Pre Approval Before You Buy an Investment Property

Getting pre approval tells you exactly how much a lender will let you borrow before you start looking. It's free and usually takes 1-3 business days.

Lenders often require borrowers to have 6-12 months of mortgage payments in reserve for investment properties. They also assess rental income at only 70% to 80% of expected amounts when determining your repayment ability. You'll need payslips from the last 2-3 months, tax returns from the last 2 financial years, bank statements, details of existing debts (home loan, car loan, credit cards), and rental estimates for the property type you're targeting. Before investing in property, consider speaking with a financial advisor to ensure it aligns with your overall financial goals.

Pre approval is valid for 90 days. Getting it early lets you move quickly when you find the right property investment opportunity and shows selling agents you're serious. A mortgage broker can submit to multiple lenders simultaneously, often securing better interest rates than going direct to your bank. It is important to calculate your expected rental income against your ongoing expenses to determine if you can cover any potential shortfall from your regular income, and to set aside an emergency fund for unexpected repairs or extended vacancy periods.

How Interest Rates Affect Your Investment Property Affordability

Every 0.25% rate rise adds approximately $70 per month to repayments on a $450,000 loan. Over a year, that's $840 — which can be the difference between comfortable cash flow and financial stress.

In April 2026, investment property interest rates sit between 6.0% and 6.8% depending on the lender, your LVR, and whether you choose interest-only or principal and interest repayments.

On a $440,000 loan at 6.2%, the difference between interest-only and principal and interest repayments is significant:

- Interest only: $2,273/month

- Principal and interest (30 years): $2,695/month

- Monthly saving: $422

Most investors start with a 5-year interest-only period then switch. This builds equity through capital growth while keeping holding costs manageable.

Capital Growth, Negative Gearing, and What to Prioritise When You Buy an Investment Property

When you buy an investment property, you're balancing two returns: capital growth (the property increasing in value) and rental yield (the income it generates relative to its price).

Researching the property market is essential to determine the best location for an investment property, as different areas can yield varying returns. High-growth properties in capital cities often have lower rental yields (2.5-3.5%) but stronger long-term appreciation. Regional properties with low vacancy rates can offer yields of 5-7% but may grow more slowly. Proximity to amenities such as public transport, shops, and schools can enhance the attractiveness of a property location to potential tenants. For affordability, higher rental income means a smaller gap to fund each month.

If the property is negatively geared — meaning expenses exceed rental income — you can claim the loss against your other income at tax time. On a $120,000 salary, the ATO effectively subsidises roughly 34.5 cents of every dollar you're out of pocket.

Most successful Australian investors prioritise capital growth markets and use negative gearing and depreciation to manage the cash flow shortfall. Over time, as tenants pay higher rent and the property builds value, the investment becomes self-funding. Many investors find that properties they initially pay money to hold eventually generate positive cash flow within 5-7 years.

Worked Example: Can You Afford a $550,000 Investment Property?

Let's run the numbers for a real scenario.

Your situation: - Household income: $130,000 before tax - Existing home value: $750,000 - Existing mortgage: $380,000 - Available equity: $220,000 (80% of $750K minus $380K) - Target property: $550,000 unit in Brisbane

Upfront costs: - Deposit (20%): $110,000 (funded from equity) - Stamp duty (QLD): $10,600 - Conveyancing and legal fees: $2,500 - Inspections and settlement costs: $1,500 - Total: $124,600 (covered by your $220,000 usable equity)

Monthly cash flow: - Rental income ($530/week): $2,297/month - Loan repayments (IO, 6.2%, $440K): -$2,273/month - Property manager, rates, insurance, strata, maintenance: -$920/month - Monthly shortfall: -$896

After tax benefits (34.5% marginal rate, ~$8,000/year depreciation): - Real out-of-pocket cost: approximately $356/month ($82/week)

That's $82 per week — the money you pay to build a $550,000 asset while tenants cover most of the costs and the property grows in value over time.

An investment property calculator estimates the costs associated with owning an investment property by combining cash outflows (loan repayments, expenses) against rental income. The cash flow is determined by subtracting monthly loan repayments and expenses from your rental income, and you can adjust monthly rental income by inputting a growth rate for potential rent increases over time.

PropBoss handles this entire calculation automatically — the feasibility calculator lets you model different purchase prices, deposit levels, and interest rates across your entire portfolio so you can see the real impact before you buy.

Frequently Asked Questions

How Much of an Investment Property Can I Afford?

As a rule of thumb, your total property investment debt (including your home) shouldn't exceed 6 times your gross household income. Take the time to calculate this before you spend money on inspections and applications. On a $130,000 income, that's about $780,000 in total debt. If you owe $380,000 on your home, you can borrow up to $400,000 for an investment property. But always get formal pre-approval from a lender — every situation is different.

Can I Buy an Investment Property as My First Home?

Yes, buying an investment property as your first home purchase is legal and increasingly common. This approach is called rentvesting — you rent where you want to live and buy an investment property where the numbers make sense. The trade-off is you won't qualify for first home buyer stamp duty exemptions or grants in most states.

Is There a Tool That Automates Investment Property Affordability Analysis?

PropBoss tracks your investment property finances automatically with bank feeds that categorise your rental income and expenses across all your properties. The equity calculator models different purchase scenarios, and the cash flow dashboard shows your real returns after all costs and tax deductions. It handles the complex calculations — deposit, borrowing power, stamp duty, ongoing costs, and tax benefits — so you don't need spreadsheets.

Start Calculating Your Investment Property Affordability

Stop guessing whether you can afford an investment property. Use PropBoss to model the real numbers — deposit, borrowing power, costs, rental income, and tax benefits — in minutes instead of hours with spreadsheets.

Try PropBoss free or use the equity calculator to find out how much usable equity you have right now. Plans start from $1/property/month.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more