Property Investment Software Explained — A Complete Guide for Australian Investors

Last updated: April 2026 · Financial year 2025-26

Property investment software helps Australian investors track the numbers that actually matter: rent, expenses, loans, equity, documents, and portfolio performance. The right platform replaces scattered spreadsheets, email attachments, and end-of-year guesswork with a single operating system for your properties.

That matters more in 2026 than it did a few years ago. Many investors now own property across multiple lenders, accounts, and entities. Interest costs can move quickly, record-keeping expectations are tighter, and it is no longer enough to find out whether a property is performing only when your accountant sends a year-end summary.

This guide explains what property investment software should do, how it differs from agency-style property management software, when spreadsheets break down, and how to compare tools without getting distracted by feature bloat. Use it alongside the PropBoss features overview and the Portfolio Return Calculator to test how a better system changes the quality of your decisions.

What Is Property Investment Software?

Property investment software is a platform designed to help investors manage the financial, reporting, and decision-making side of owning property. That usually includes rental income tracking, expense categorisation, loan visibility, document storage, portfolio dashboards, and reporting that is usable before tax time rather than after it.

It is different from a basic spreadsheet because the data is structured, repeatable, and easier to keep current. It is also different from software built mainly for property managers, which often focuses on inspections, maintenance requests, trust accounting, and tenant workflows for agency teams.

For an Australian investor, the real question is not "Do I need more software?" It is "Do I have a reliable system for seeing what each property and the whole portfolio are doing right now?" If the answer is no, the software category is relevant.

Worked Example — Comparing Manual Tracking With Purpose-Built Software

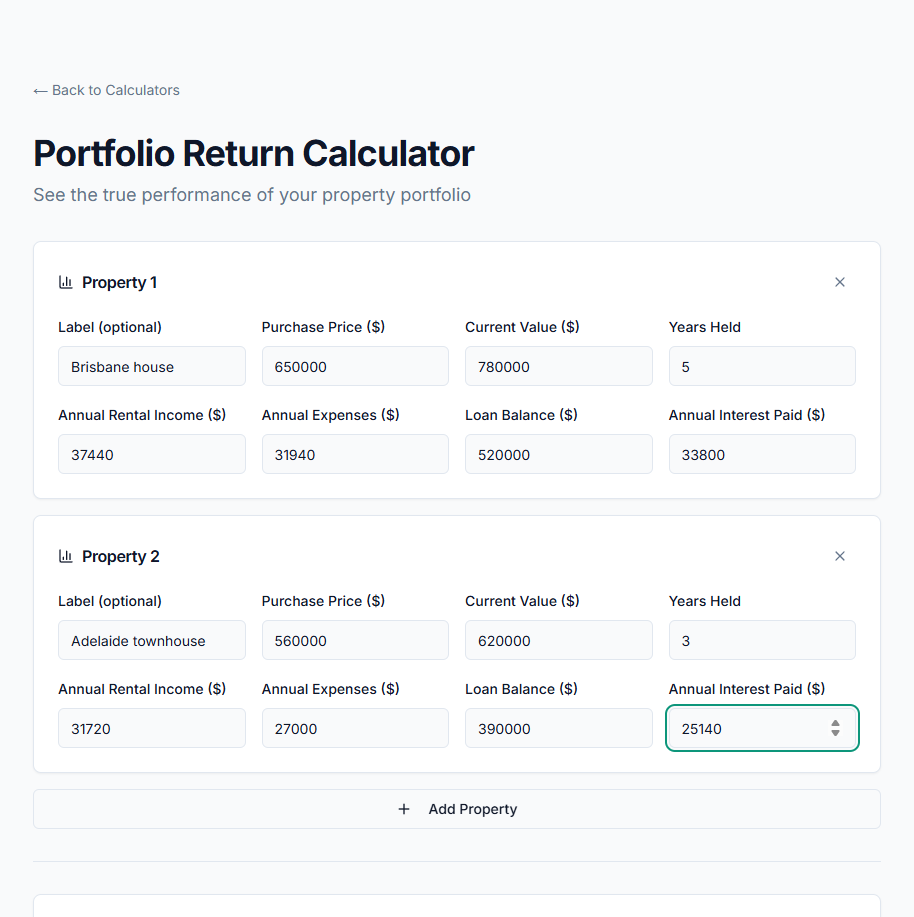

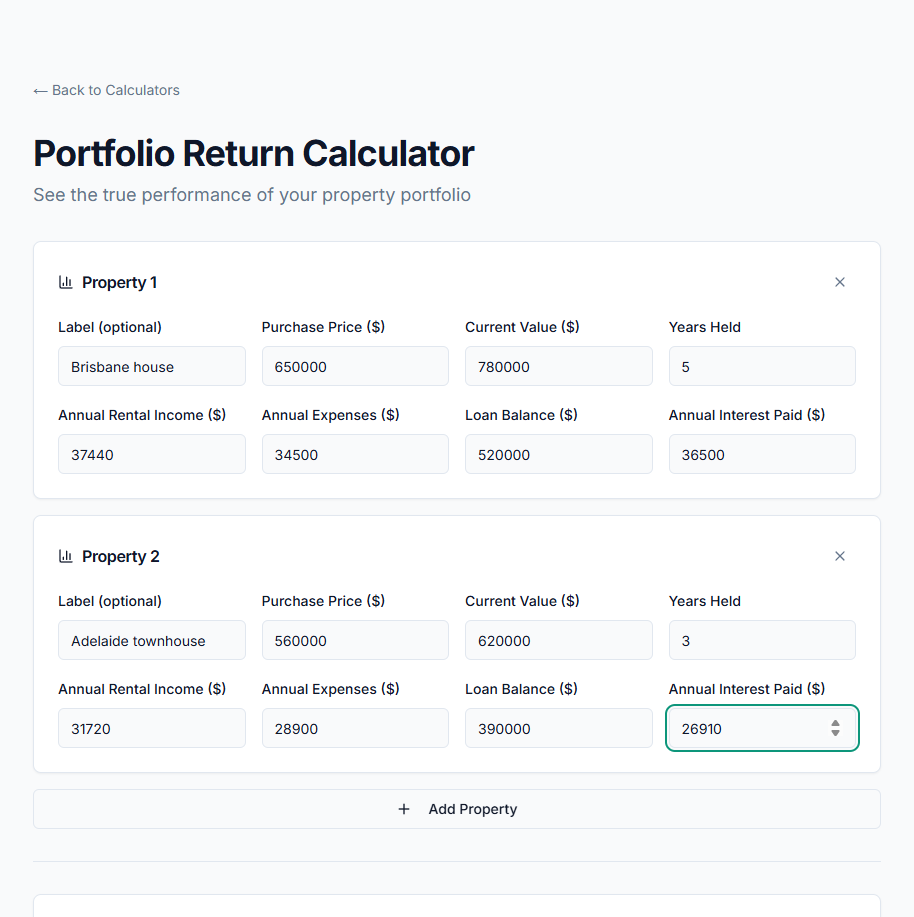

Assume an investor owns two residential properties:

- a Brisbane house worth $780,000 rented at $720 per week

- an Adelaide townhouse worth $620,000 rented at $610 per week

They currently use a spreadsheet, separate bank exports, and email folders to manage the portfolio.

| Item | Annual Amount |

|---|---|

| Gross rent collected | $69,160 |

| Interest, rates, insurance, strata, repairs, and management fees | -$58,940 |

| Pre-tax cash flow | $10,220 |

| Missed deductible expenses found late at EOFY | -$1,480 |

| Time spent reconciling transactions and statements | 30-40 hours |

| Duplicate or miscoded transactions requiring cleanup | 18 entries |

| Net position after cleanup and missed items | $8,740 |

Now compare that with a software-led workflow where bank feeds, recurring rules, and central document storage are already in place:

| Item | Annual Amount |

|---|---|

| Gross rent collected | $69,160 |

| Interest, rates, insurance, strata, repairs, and management fees | -$58,940 |

| Pre-tax cash flow | $10,220 |

| Missed deductible expenses found late at EOFY | -$180 |

| Time spent reconciling transactions and statements | 6-8 hours |

| Duplicate or miscoded transactions requiring cleanup | 3 entries |

| Net position after cleanup and missed items | $10,040 |

The improvement is not magic. It comes from fewer manual steps, cleaner categorisation, and better visibility during the year. Investors rarely switch to software because it is fashionable. They switch because error reduction and decision speed become worth more than the comfort of an old spreadsheet.

Test the portfolio side of this workflow in the PropBoss Portfolio Return Calculator, then compare holding costs in the Cash Flow Calculator.

How Property Investment Software Works

Step 1: Connect the portfolio data sources

Start with the core records: properties, ownership entities, linked accounts, loan balances, and recurring expenses. The software should make it obvious which property each transaction belongs to and whether it is income, holding cost, capital work, or admin.

Step 2: Standardise transaction rules

Recurring costs such as loan interest, insurance, rates, strata, and management fees should be categorised consistently. This is where spreadsheets often start to drift because naming conventions change and formulas get patched manually over time.

Step 3: Centralise evidence and documents

Leases, invoices, loan letters, settlement statements, and depreciation schedules should live with the property record, not across inboxes and desktop folders. A better system reduces the time it takes to answer basic questions such as "What did we spend?" and "Can we prove it?"

Step 4: Measure property and portfolio performance

A good platform shows more than total rent. It should help you read cash flow, debt, yield, and return by property, then show what changes when you refinance, lift rent, or buy the next asset.

Step 5: Use the numbers to make decisions

The end goal is not reporting for reporting's sake. It is better decisions around buying, holding, refinancing, improving, or selling. That is why investor software matters most when the portfolio becomes more complex, not less.

What Good Property Investment Software Should Track

| Item To Track | Why It Matters |

|---|---|

| Rental income by property and month | Shows whether the portfolio is actually paying the owner for the risk being taken. |

| Loan balances, repayments, and offset cash | Gives a real view of leverage and holding cost, not just gross rent. |

| Operating expenses | Prevents underestimating the drag from rates, insurance, repairs, strata, and management fees. |

| Documents and receipts | Makes accountant handover and audit-style evidence much easier. |

| Performance by property | Helps identify which asset is carrying the portfolio and which one is lagging. |

| Equity and valuation assumptions | Supports refinance and acquisition decisions with current numbers. |

| Tax categories and year-end summaries | Reduces cleanup work and improves reporting quality before EOFY. |

| Scenario comparisons | Lets investors test rent, vacancy, or rate changes before they happen. |

| Cross-property reporting | Essential once more than one property or one entity is involved. |

| Reminder workflows | Useful for lease renewals, insurance dates, loan repricing, and document requests. |

This is also where software selection becomes practical. If a platform cannot track these basics cleanly, extra marketing features do not matter. A portfolio tool should remove blind spots first.

In search terms, this is usually the difference between broad property investment software Australia queries and narrower comparison terms such as best property management software Australia, property management software for landlords Australia, property investment analysis software, or free property investment software Australia. Those searches all point to the same core user job: investors want software that makes the portfolio easier to run and easier to understand.

For investors still building a manual model, our companion post on Investment Property Spreadsheet: Track Costs & Cash Flow (2026) is a useful baseline.

Property Investment Software vs Spreadsheets

| Factor | Spreadsheet | Property Investment Software |

|---|---|---|

| Setup cost | Low | Usually recurring subscription |

| Data entry | Mostly manual | More automated once configured |

| Error risk | Higher | Lower if rules are maintained |

| Portfolio visibility | Limited | Stronger cross-property reporting |

| Scenario testing | Possible but fragile | Usually faster and easier |

| Document storage | Separate folders or links | Usually tied to the property record |

| Accountant handover | Can be messy | Cleaner if records stay current |

| Best suited for | One simple property and disciplined admin | Multi-property investors or anyone tired of manual cleanup |

Spreadsheets are not wrong. They are just unforgiving. They work best when the investor has one property, one loan, simple records, and the discipline to update the file every month.

The breaking point usually comes when the portfolio adds a refinance, multiple offset accounts, different ownership structures, or irregular costs that do not fit the original model. At that point the spreadsheet is no longer a lightweight tool. It becomes a fragile custom system that depends on one person's memory.

If you want to compare a manual workflow against a live portfolio view, read Property Portfolio Management Software Australia Guide 2026 and then benchmark the numbers in the Portfolio Return Calculator.

Is Property Investment Software Worth It in 2026?

For many Australian investors, yes, but not for the reason software vendors usually lead with.

The main value is not that software feels modern. The value is that investors are making more decisions under more complexity: higher debt balances than a few years ago, more moving parts across rent and costs, and more need to understand portfolio-level trade-offs before year-end.

Property investment software tends to be worth it when:

- you own more than one property

- you rely on multiple loans, offsets, or entities

- you still run year-end cleanup from bank CSV exports

- you want a live view of performance instead of a backward-looking tax pack

- you are comparing whether to hold, refinance, or buy again

It is less valuable when you have one straightforward property, very low transaction volume, and a spreadsheet that is consistently maintained. Even then, the software question tends to come back once the owner wants better visibility rather than just record storage.

The Role of Bank Feeds, Tax Categorisation, and Document Control

The most important sub-topic in this cluster is not the dashboard. It is data accuracy.

Many investors judge software by how polished the interface looks. That matters, but the real value comes from the plumbing underneath: bank-feed reliability, clean categorisation rules, and documents that stay attached to the right property and expense trail.

When this layer is weak, the reporting above it becomes unreliable. A beautiful dashboard built on incomplete or miscoded transactions is just a fast way to read the wrong answer.

When this layer is strong, three things improve:

- Monthly reporting becomes useful, not cosmetic.

- Accountant handover gets faster because the records are already organised.

- Decision-making improves because investors trust the inputs.

This is also where software starts to outperform generic accounting tools. General tools can track money. Investor software should track money in property context: per asset, per loan, per holding structure, and with enough evidence to support the conclusion.

Common Property Investment Software Mistakes

1. Buying agency software for an investor problem

Many tools are built for property managers, not investors. If most of the platform is about inspections, trust accounting, and agency workflows, a residential investor may end up paying for complexity without better decision support.

2. Keeping the spreadsheet anyway

Software only helps if it becomes the operating system. If the portfolio still depends on a shadow spreadsheet for the "real" numbers, the process has not improved enough.

3. Ignoring setup discipline

Even good software fails when properties, accounts, and categories are set up carelessly. The first week of clean structure saves many hours later.

4. Comparing on headline price only

The cheaper platform is not automatically the better value. If it lacks reporting, document storage, or usable automation, the owner may still be paying the hidden cost through manual work.

5. Confusing tax support with tax advice

Software should make the records cleaner, but it does not replace strategy on structures, treatment, or timing. Investors still need judgement when real tax questions arise.

6. Choosing features before deciding the job

Start with the job to be done: tracking one rental, managing a growing portfolio, replacing spreadsheets, or improving accountant handover. The right software for one job can be the wrong software for another.

How To Evaluate Property Investment Software

Use this sequence when comparing platforms:

- List the jobs you need solved right now.

- Confirm how many properties, accounts, and entities the software needs to support.

- Check whether the tool handles recurring costs, loan visibility, and document storage cleanly.

- Test whether the reporting is useful at both property and portfolio level.

- Compare how much manual work remains after setup.

Software value = time saved + errors avoided + better decisions made

Manual drag = repeated data entry + stale reporting + missing evidence + poor visibility

Worked Example — Choosing Between Three Options

| Option | Annual Cost | Main Strength | Main Weakness | Best Fit |

|---|---|---|---|---|

| Spreadsheet | $0 direct | Cheap and flexible | Manual upkeep, weak portfolio visibility | One simple property |

| Generic accounting app | $300-$900 | Good transaction ledgers | Not built for investor decisions | Owners focused mainly on bookkeeping |

| Investor software | $300-$1,500+ | Portfolio reporting, automation, property context | Needs disciplined setup | Multi-property investors and growth-stage owners |

Imagine an investor with three properties, two lenders, and one accountant who charges extra for cleanup. If investor software saves 20 hours of admin and reduces cleanup fees while improving buy-hold-refinance decisions, the subscription often pays for itself long before the marketing copy enters the conversation.

Use the Portfolio Return Calculator to test whether the cleaner workflow supports a better next decision, then review the broader features page for the platform workflow itself.

Frequently Asked Questions

What is the best property investment software in Australia?

The best software is the one that matches the complexity of your portfolio and the decisions you need to make. If your main problem is spreadsheet sprawl, choose a tool that centralises reporting and records. If your main problem is weak visibility into loans and returns, choose a platform that makes portfolio performance obvious rather than buried.

How does property investment software compare with spreadsheets?

Spreadsheets are flexible and cheap, but they are heavily dependent on manual upkeep. Software becomes more valuable once the portfolio has enough moving parts that accuracy and speed matter more than flexibility. Most investors do not outgrow spreadsheets because formulas stop working. They outgrow them because trust in the numbers starts slipping.

What features should Australian investors look for in property portfolio software?

Look for strong transaction handling, portfolio dashboards, property-level reporting, document storage, and workflows that make accountant handover easier. If the platform also helps with scenario modelling and ongoing visibility into debt and return, it is usually solving the right investor problem.

Is there free property investment software in Australia, and what are the trade-offs?

Free tools can be useful for trial use or simple portfolios. The trade-off is usually limited automation, fewer reports, weaker support, or a cap on how much of the portfolio can actually be tracked. A free product that still forces side spreadsheets may not be meaningfully cheaper in practice.

What is the difference between property investment software and property management software?

Property management software usually focuses on tenancy operations and agency tasks. Property investment software is more about ownership, performance, reporting, and strategy. Some overlap exists, but the investor should judge tools by whether they improve portfolio decisions rather than whether they look impressive to an agency team.

Can property investment software track rental property cash flow and tax deductions?

Yes. That is one of the clearest use cases. Good software helps investors see income and expenses in context, store evidence, and keep records current before EOFY. It should reduce friction, not create another layer of admin.

Which property software is best for self-managed landlords in Australia?

Self-managed landlords usually need simple but reliable workflows: income and expense tracking, reminders, supporting documents, and clear reporting. The right tool is not the one with the most enterprise features. It is the one that cuts manual work without forcing agency complexity into a one-owner workflow.

Can property investment software replace a property accountant?

No. It can improve records, reduce cleanup work, and make the accountant's job faster, but it does not replace professional judgement. Think of software as better infrastructure, not a substitute for tax or structuring advice.

Does property portfolio software support bank-feed automation and reporting?

Many investor platforms do, and that is often where the practical value starts. Bank feeds reduce manual entry, help maintain cleaner categories, and make monthly reporting more usable. Automation is most valuable when it leads to more trustworthy numbers.

Is commercial property management software relevant for residential property investors?

Usually only if the investor truly operates a commercial or mixed-use portfolio. Otherwise those platforms can be overbuilt for the task, with more operational complexity than most residential investors need. A residential investor should optimise for visibility and usability, not for enterprise feature count.

Track Your Property Investment Workflow Automatically With PropBoss

If your current system still depends on spreadsheets, bank exports, and year-end cleanup, that is usually the sign the portfolio has outgrown the process.

PropBoss helps investors centralise property data, track portfolio performance, and replace scattered manual admin with a clearer operating system built for Australian property ownership workflows.

Get Started Free

See PropBoss Features

Try the Portfolio Return Calculator

Related Guides & Tools

- Portfolio Return Calculator — model returns, equity, and overall portfolio performance.

- Cash Flow Calculator — test the holding-cost impact of loans, rates, and rent.

- Rental Yield Calculator — benchmark gross and net yield before adding another property.

- Investment Property Spreadsheet: Track Costs & Cash Flow (2026) — see the manual workflow this guide helps replace.

- Property Portfolio Management Software Australia Guide 2026 — supporting software-comparison article for investors.

- How to Build a Property Portfolio Australia Guide 2026 — connect software selection back to portfolio growth strategy.

Methodology, Sources, and Review Context

This guide was prepared using current Australian property investor workflows, live PropBoss product research, competitor software reviews, and practical software-selection criteria for cash flow tracking, portfolio reporting, document storage, tax record-keeping, and calculator support. It is written as general educational information for Australian property investors and is not personal financial, accounting, or tax advice.

Research for this guide was refreshed on 29 April 2026. The pages reviewed for comparison were mainly vendor landing pages, software directory listings, and introductory educational articles. This guide is designed to give investors a clearer framework for comparing tools, with worked examples and decision criteria.

Reviewed in the context of PropBoss product and investor workflows by Jonathan Zuvela, founder of PropBoss.

Replace scattered spreadsheets with a live portfolio workflow

Explore the PropBoss feature set, then test the impact of better visibility with the live portfolio and cash-flow calculators.