Land Tax Explained - A Complete Guide for Australian Investors

Last updated: April 2026 - Financial year 2025-26

Land tax is one of the most misunderstood holding costs in Australian property investing. Many buyers focus on the deposit, interest rate, and stamp duty, then get blindsided by an annual land tax bill that was never built into the original cash flow model. That mistake is easy to make because every state uses different thresholds, different rates, different assessment dates, and different rules for trusts, companies, and absentee owners.

That complexity matters for Australian investors. A land value that attracts no tax in one state can trigger a recurring bill in another. A portfolio that looks safe on a per-property basis can become taxable once the state's aggregation rules combine all your holdings. And a structure chosen for asset protection can become materially more expensive once trust or foreign-owner surcharges are added.

This guide explains how land tax works in Australia, how to estimate it properly, what you can usually claim, how ownership structure changes the outcome, and why land value discipline matters as much as rental yield. It also gives you a national comparison table, a worked investor example, formula-based calculations, and direct links to the relevant PropBoss tools.

General information only: This guide is educational content for Australian property investors. It is not personal tax, legal, or financial advice. Before acting on a land-tax strategy, confirm current rules with the relevant state revenue office and your accountant.

Methodology note: The thresholds and examples here are written for the 2025-26 guide cycle and checked against current revenue-office references during this run, including NSW threshold guidance updated on 25 September 2025, Victoria guidance updated on 7 April 2026, and Western Australia guidance updated on 20 February 2026. Use the live PropBoss calculators before making purchase or holding decisions.

What Is Land Tax?

Land tax is an annual state or territory tax on taxable land you own. It is generally based on the unimproved or site value of the land rather than the full market value of the property with the dwelling on it. That distinction is critical. A house might be worth $1.2 million, but if the assessed land value is $420,000, the land-tax calculation starts from that $420,000 figure and the state's threshold and rate schedule.

For investors, land tax usually applies to residential investment properties, commercial property, vacant land, and holiday homes. Your main home is usually exempt, but the rules vary where land is partly rented, partly used for business, or held in a more complex structure. Every state except the Northern Territory imposes some form of land tax, and the ACT effectively taxes investment land from the first dollar through its own system.

The practical takeaway is simple: land tax is not a one-off acquisition cost. It is a recurring drag on returns. If you do not budget for it up front, your property analysis is incomplete.

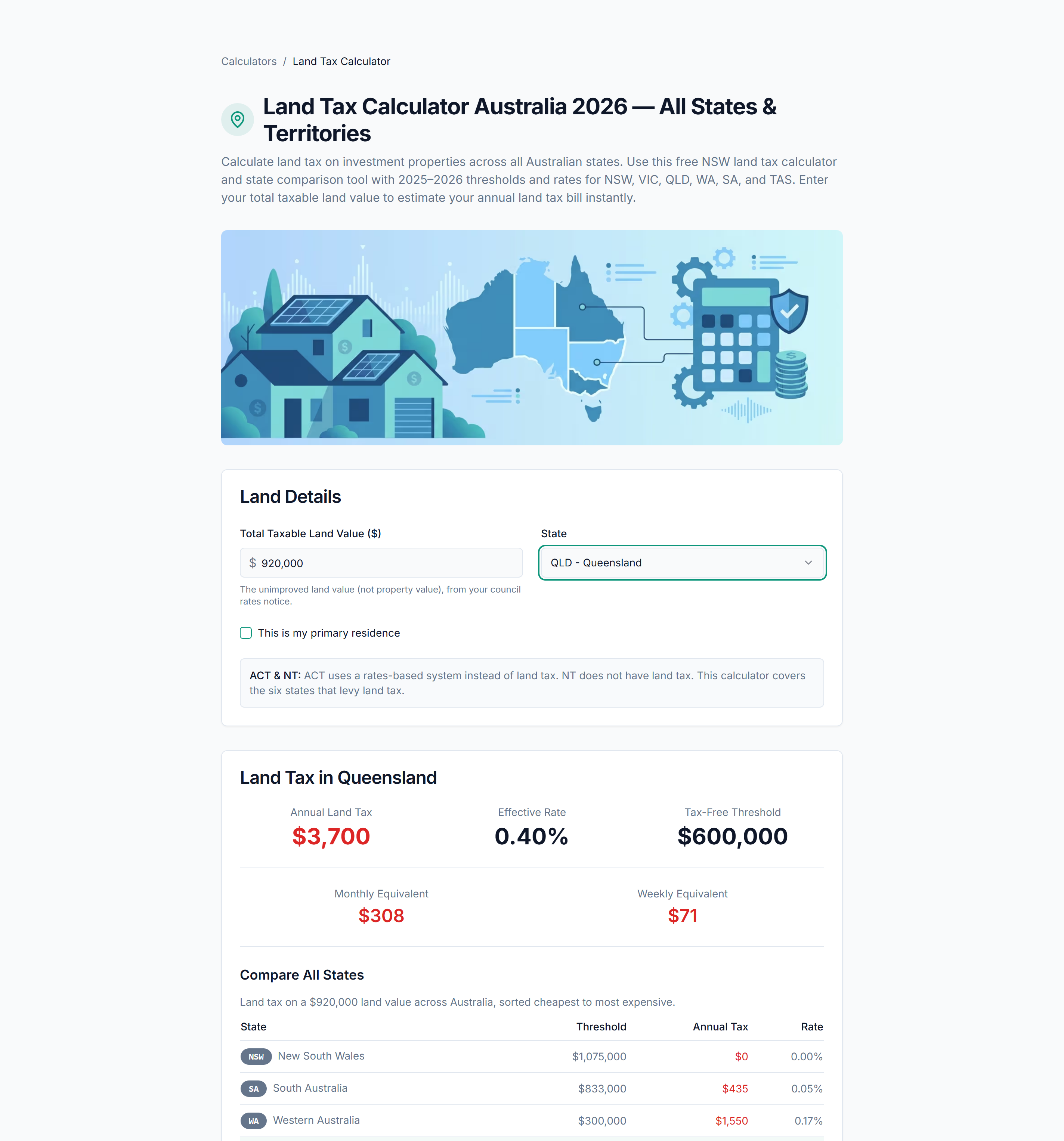

Worked Example Table

Assume an investor owns two Queensland investment properties with a combined taxable land value above the individual threshold and wants to understand the annual cost before tax deductions.

Example Scenario: Two Brisbane Investments

| Item | Annual Amount |

|---|---|

| Combined taxable land value | $920,000 |

| Individual threshold | -$600,000 |

| Value above threshold | $320,000 |

| Indicative base amount | $500 |

| Indicative marginal tax component | $3,200 |

| Indicative annual land tax | $3,700 |

This is not a substitute for a live state calculation, because rates change by owner type and bracket. It is a planning example designed to show why a portfolio that felt "under the radar" at one property can become materially less attractive once a second property pushes the owner's total land value above the threshold.

Use the Land Tax Calculator to calculate your exact land tax with your current state and land-value assumptions.

How Land Tax Works

1. The state decides the land value

Each state uses its valuation authority to determine the taxable land value. That figure is usually the unimproved or site value, not the price you paid and not the full market value of the dwelling plus land.

2. Your holdings are aggregated within a state

Land tax is usually assessed on the total taxable land you own in that state, not on each property in isolation. That means two moderate properties can trigger tax even if neither would have crossed the threshold by itself.

3. Your ownership type matters

Individuals, companies, and trustees are not always treated the same way. Some states apply lower thresholds or extra charges to trusts, and foreign or absentee owners can face large surcharges.

4. The threshold is applied

If your taxable land value is below the relevant threshold, your annual bill may be zero. Once you move above it, tax usually starts as a base amount plus a marginal rate on the value above the threshold.

5. The assessment date controls the year

This is a common trap. States assess land tax by reference to land ownership on a taxing date, such as 31 December or 30 June. If you own the land on the taxing date, the bill may apply for the whole year even if you later sell the property.

Tax Bracket Table

Land tax is not an income tax, but investors still need an after-tax view because land tax on an income-producing property is usually deductible. That means the real economic cost varies by marginal tax rate.

| Marginal tax rate | Land tax paid | Potential tax saving | After-tax cost |

|---|---|---|---|

| 16% | $3,700 | $592 | $3,108 |

| 30% | $3,700 | $1,110 | $2,590 |

| 37% | $3,700 | $1,369 | $2,331 |

| 45% | $3,700 | $1,665 | $2,035 |

This is why investors should not stop at the gross bill. The pre-tax cash outflow is real, but the effective cost can be materially lower once the deduction is claimed correctly.

Calculator CTA

Calculate your exact land tax with our free Land Tax Calculator.

If you are working state by state, use the dedicated calculators for NSW, VIC, QLD, WA, SA, TAS, ACT, and NT.

What You Can Claim Or Do

The table below covers the investor actions and treatments that matter most in practice.

| Item | What it means for investors |

|---|---|

| Land tax on a rental property | Usually deductible as a rental expense if the property is income producing. |

| Land tax on your home | Usually not deductible because it is a private expense. |

| Apportionment | May be required if the property was only partly income producing during the year. |

| Objection to valuation | If the assessed land value looks too high, an objection may reduce future bills. |

| Ownership-structure review | Useful before purchase because trust and company settings can change thresholds and surcharges. |

| Cross-state diversification | Can reduce the chance that one state's aggregation rules push you into a higher bill. |

| Apartment versus house comparison | Apartments often carry a lower land component than detached houses, which can soften land-tax exposure. |

| Live modelling before purchase | Essential. Estimate land tax before you sign, not after the assessment notice arrives. |

For broader EOFY planning, use the Tax Deduction Checklist and compare the impact on whole-property returns with the Cash Flow Calculator.

Ownership Structure Snapshot

Land tax can change materially depending on how you hold the asset. The same property can look acceptable in your personal name and much less attractive once a trust surcharge or lower company threshold is applied.

| Ownership type | Common land-tax effect |

|---|---|

| Individual owner | Usually gets the standard individual threshold and rate schedule. |

| Company owner | Often faces a lower threshold than an individual in some states, so tax can start earlier. |

| Trustee / trust owner | Can face lower thresholds or surcharge treatment depending on the state and trust type. |

| Foreign or absentee owner | Can face a separate surcharge from the first dollar in some states, which can dominate the normal bill. |

This is why ownership structure should be modelled before purchase, not justified after settlement. A legal structure that helps with asset protection or estate planning can still be a poor economic choice if land tax becomes materially worse.

Comparison Table: Land Tax vs Council Rates

Investors often confuse land tax with council rates. They are both recurring property costs, but they are not the same thing.

| Factor | Land tax | Council rates |

|---|---|---|

| Charged by | State or territory government | Local council |

| Main basis | Taxable land value | Local rating method on the property |

| Typical target | Investors, owners of taxable land, some commercial holdings | Nearly all property owners |

| Threshold | Usually yes, except special systems such as ACT treatment | Usually no threshold in the same sense |

| Main-home exemption | Usually yes | Usually no full exemption just because you live there |

| Portfolio aggregation | Usually yes within a state | No, charged per property |

| Tax deductibility for rentals | Usually deductible | Usually deductible where income producing |

The investor mistake is to budget for rates because they arrive more regularly, but ignore land tax because it feels less immediate. In reality, land tax can be the larger annual surprise.

Is It Worth It?

Whether a property is "worth it" after land tax depends on more than the state threshold. The real question is whether the property still works after finance costs, rates, insurance, vacancies, maintenance, and land tax are all loaded into the model.

In 2026, this matters more because many investors are already carrying tight buffers. A property with weak rental yield and a high land component can look acceptable on a headline gross-yield basis, then turn mediocre once land tax is layered in. This is especially relevant in states where thresholds are low or trust surcharges are meaningful.

The better framing is not "Can I afford the land tax bill?" but "Does this property still clear my return hurdle once land tax is treated as a recurring cost that can rise with land values?" If the answer is no, you are not looking at a minor admin issue. You are looking at a structural problem in the deal.

The Key Factor: Land Value, Not Purchase Price

The single most important sub-topic in land-tax planning is the land value itself. Investors spend a lot of time comparing suburb growth, rent, and borrowing power, but far less time comparing land-value intensity between asset types.

A detached house on a large block can carry a high land value relative to total purchase price. An apartment in the same suburb may have a similar market value but a lower attributable land component. That difference can radically change annual land-tax exposure. Two $900,000 properties can produce very different land-tax outcomes if one has a $620,000 land value and the other has a $190,000 land value.

That is why land tax should be part of asset selection, not just end-of-year compliance. Before buying, compare likely land values, not just prices. Before expanding, compare whether the next acquisition pushes your existing state total into a worse bracket. Before restructuring, model whether a trust or company improves the commercial picture or makes it worse.

Common Mistakes

1. Modelling each property separately

Many investors miss the state aggregation rule and assume each asset gets its own threshold test. That is often wrong.

2. Using purchase price instead of land value

Land tax usually tracks the taxable land component, not the contract price. If you model from the wrong base, the estimate is unreliable.

3. Ignoring trust or company settings

A structure that looks elegant for legal or estate reasons can still be expensive for land tax.

4. Treating the bill as a one-year anomaly

Land tax is a recurring cost. If land values rise, the bill can rise too.

5. Forgetting the deduction

Some investors overstate the long-term burden by ignoring the deduction on income-producing property. The gross bill is not the whole story.

6. Waiting for the notice before checking the numbers

The best time to model land tax is before purchase, not when the revenue office is already asking for payment.

How To Calculate Land Tax

The generic investor formula is:

Land tax = base amount + (marginal rate x taxable land value above threshold)

Work through it like this:

Step 1: Identify the taxable land value

Use the state's assessed land value, not your purchase price.

Step 2: Group properties by state

Do not combine NSW and Queensland holdings into one number for calculation. Each state assesses its own holdings under its own rules.

Step 3: Add up the taxable land in that state

If you own multiple taxable properties in the same state, combine them.

Step 4: Apply the threshold and bracket

Subtract the threshold. Then apply the relevant base amount and rate for that ownership type.

Step 5: Check the after-tax effect

If the property is income producing, estimate the post-deduction cost as well.

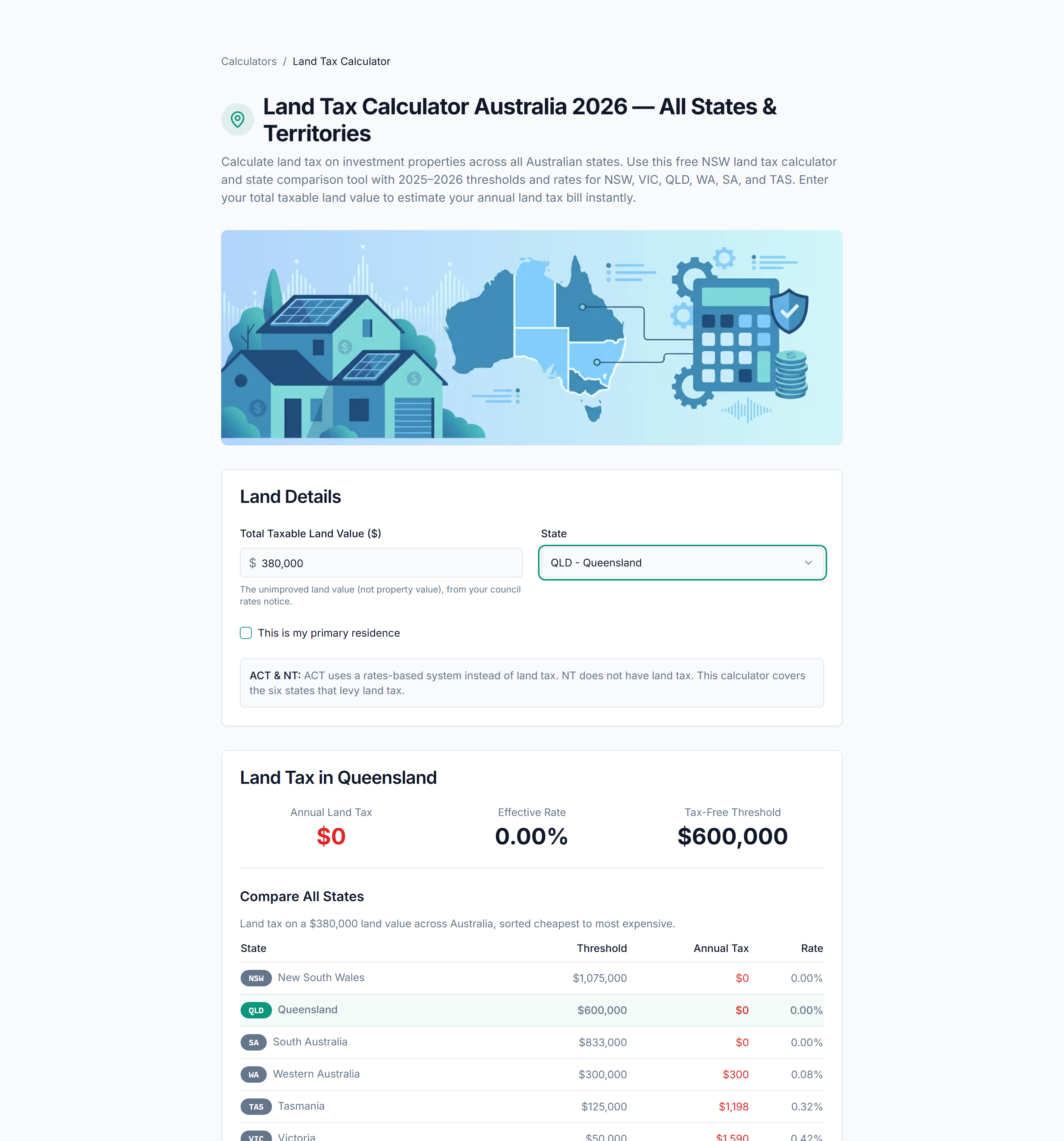

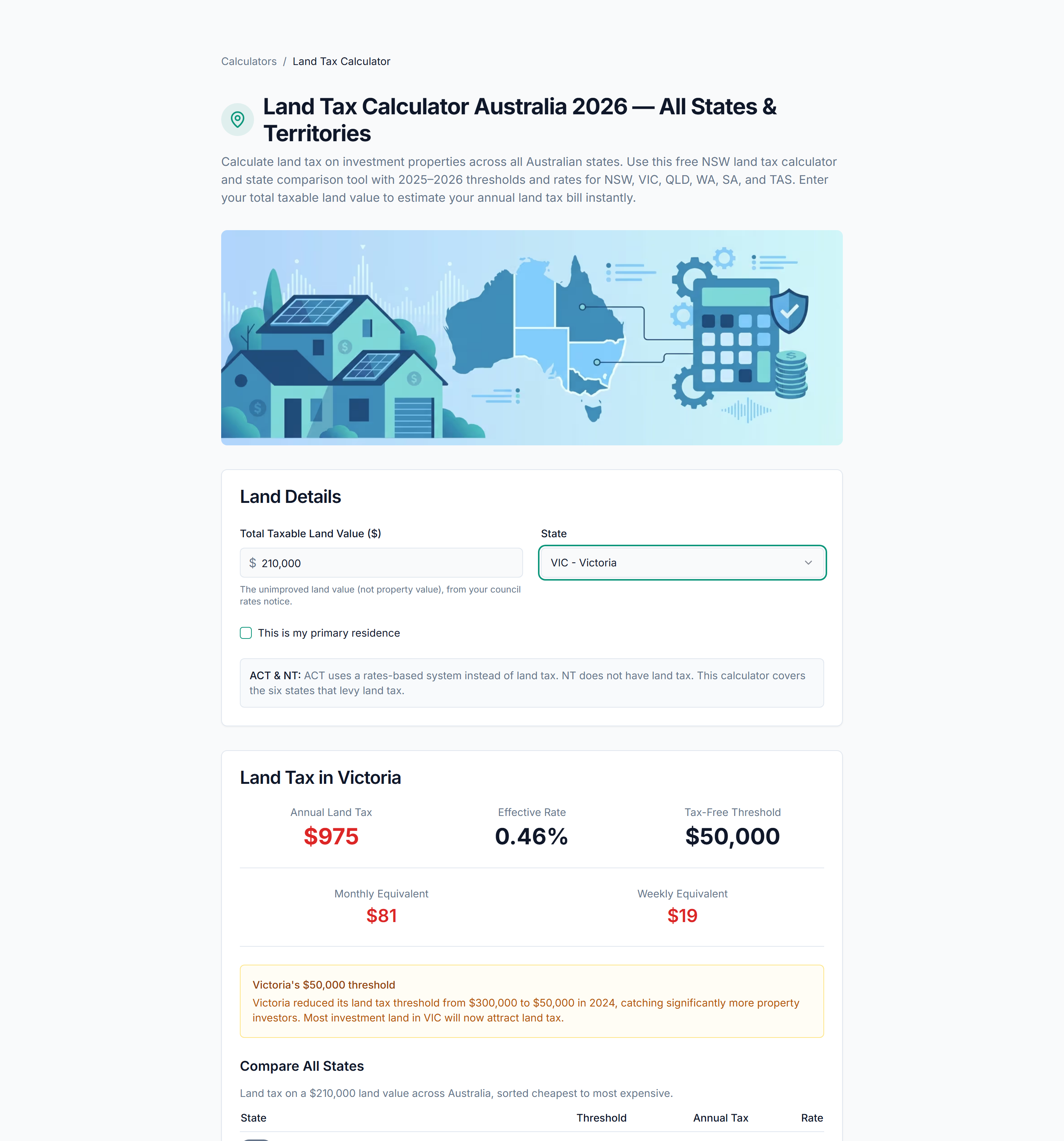

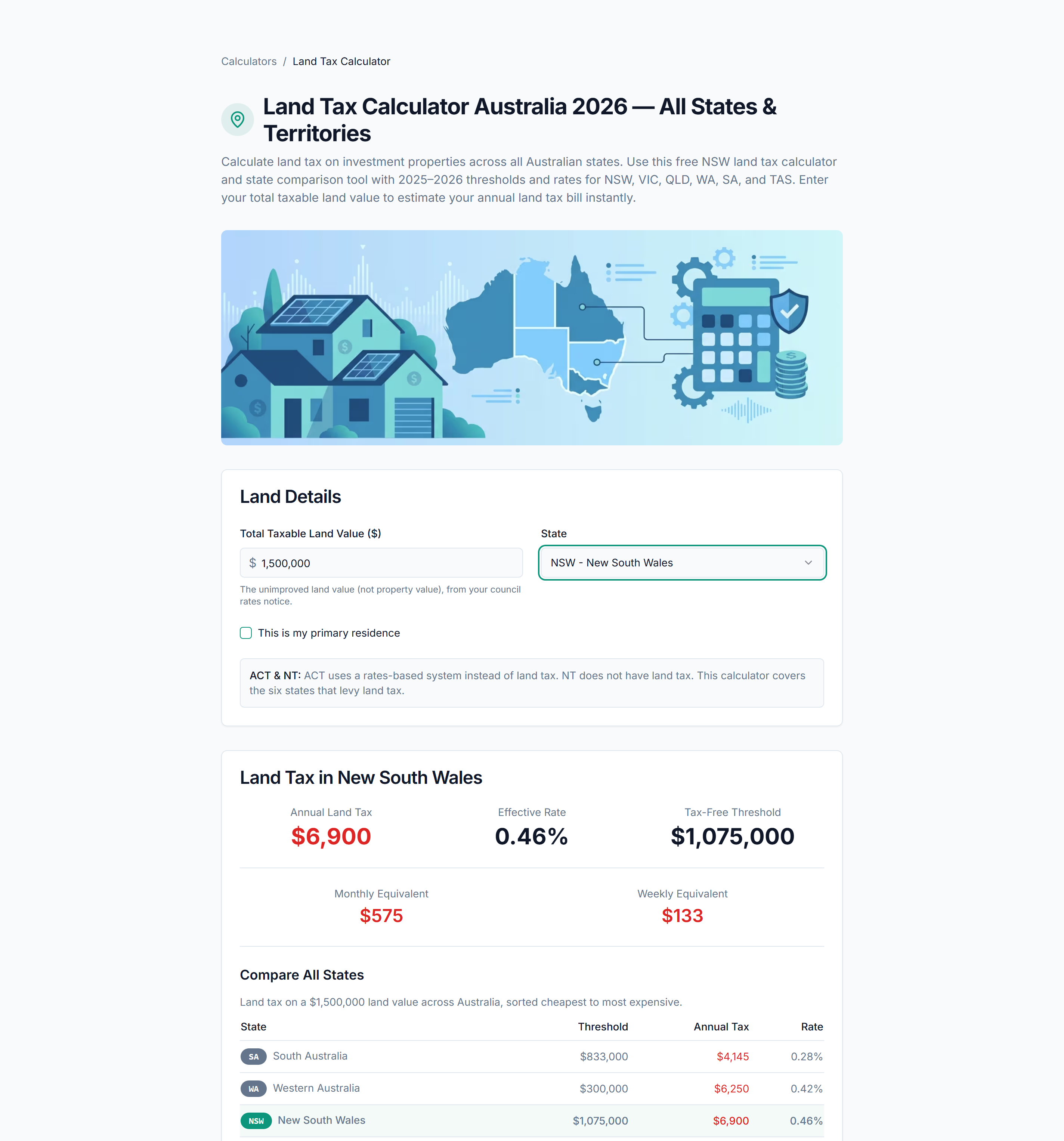

Worked Multi-State Calculation

| Property | State | Taxable land value |

|---|---|---|

| Unit in Parramatta | NSW | $520,000 |

| House in Newcastle | NSW | $430,000 |

| Townhouse in Cannon Hill | QLD | $380,000 |

| Apartment in South Yarra | VIC | $210,000 |

NSW total: $950,000, which is below the current general threshold in this guide context, so the indicative bill is $0.

QLD total: $380,000, which sits below the individual threshold used in this guide context, so the indicative bill is $0.

VIC total: $210,000, which is above Victoria's much lower threshold, so land tax is likely payable.

The lesson is not that one state is always "better." The lesson is that a national portfolio needs state-by-state modelling, because identical-looking acquisitions create very different holding costs.

Frequently Asked Questions

How to avoid land tax in QLD?

You cannot lawfully avoid Queensland land tax by hiding ownership or misclassifying property use. Legitimate ways to reduce exposure include staying below the applicable threshold, using available exemptions for a principal place of residence or qualifying land, buying assets with a lower land component, or spreading holdings across different ownership entities only after getting tax and legal advice. Investors should model the land tax cost before purchase rather than trying to repair the problem later.

What is land tax in Queensland?

Queensland land tax is an annual state tax on the taxable value of freehold land you own in Queensland at midnight on 30 June. It generally applies to investment, commercial, and vacant land, while a principal place of residence is usually exempt. The amount depends on the type of owner and the taxable value of the land.

Who pays land tax in Queensland?

In Queensland, land tax is paid by the owner of taxable freehold land as at midnight on 30 June. That can include individuals, companies, and trustees. Owner-occupiers are generally exempt for their main residence, but investors, owners of holiday homes, and many holders of vacant or commercial land can become liable once their taxable land value passes the relevant threshold.

How much is land tax in QLD?

The amount depends on your taxable Queensland land value and ownership type. For individuals, the tax-free threshold is higher than for companies and trustees, so some owners pay nothing while others move into a marginal rate schedule. The practical answer is to calculate from the latest land valuation and rate table rather than guessing from the purchase price of the property.

When do you pay land tax in QLD?

Queensland land tax is assessed based on land owned at midnight on 30 June. Assessment notices are then issued by the Queensland Revenue Office and the due date appears on the notice. Investors should not assume the bill is pro rata for part of the year, because the assessment is tied to the taxing date rather than the number of months held.

What is land tax in Australia?

Land tax in Australia is a state or territory charge on taxable land, usually based on the unimproved or site value of the land rather than the market value of the full property. Each state sets its own thresholds, rates, exemptions, and surcharges, so investors owning property in multiple states are dealing with multiple systems rather than one national rulebook.

What is the land tax threshold in QLD?

For the 2025-26 guide context, Queensland's individual threshold is generally treated as $600,000, with lower thresholds applying to companies and trustees. Investors should confirm the latest rate table for their ownership structure before relying on any threshold because state revenue offices can update rates, concessions, and assessment methods.

When is land tax payable in QLD?

Queensland land tax is payable by the date shown on the assessment notice issued after the 30 June taxing date. Payment options usually include BPAY, card, and other revenue-office methods. If cash flow is tight, it is better to contact the revenue office early than to ignore the bill and incur penalty interest.

How is land tax calculated in QLD?

Queensland land tax is calculated from the taxable value of your Queensland land, the threshold for your ownership type, and the applicable rate bracket. In general terms, the formula is base amount plus the marginal rate on the value above the threshold. The land value is not the same thing as the full market value of the property.

Is land tax tax deductible in Australia?

Land tax on an income-producing investment property is generally deductible as a rental expense in the year it is incurred, subject to normal tax rules and apportionment where relevant. It is not normally deductible for a principal place of residence because that is a private expense. Investors should keep clear records and confirm treatment with their accountant if the property use changed during the year.

Track Your Land Tax Automatically With PropBoss

Track your land tax automatically with PropBoss.

PropBoss helps Australian investors bring together purchase costs, holding costs, land tax, capital gains tax, and portfolio performance in one place. That matters most when you own property across multiple states and need a single view of recurring costs rather than a collection of separate notices and spreadsheets.

Get Started Free | Try the Calculator

Related Guides & Tools

- Land Tax Calculator - estimate your land tax bill with current assumptions.

- QLD Land Tax Calculator - calculate Queensland-specific land tax.

- NSW Land Tax Calculator - model NSW thresholds and rates.

- Cash Flow Calculator - test how land tax changes annual holding costs.

- Capital Gains Tax Calculator - model tax when you eventually sell.

- Tax Deduction Checklist - make sure recurring property expenses are recorded properly.

- Qld Land Tax Guide 2026 - deeper state-specific reading for Queensland investors.

- Land Tax in Australia 2026: Thresholds, Rates, and How to Calculate Your Bill - supporting cluster article with a broader explainer format.

Estimate the holding cost before you buy

Model the land value, compare state outcomes, and pressure-test the annual holding cost before you commit to the next purchase.