Using Equity to Buy a Second House in Australia Guide (2026)

A step-by-step guide to leveraging your home equity to purchase a second house or investment property in Australia, with worked examples and 2026 rates.

You can use the equity in your home as the deposit for a second house, instead of waiting years to save the cash.

For Australian property investors, the strategy is simple in theory: your current home has grown in value, your loan balance has fallen, and the difference can help fund the next purchase.

The details matter. You still need enough borrowing power, a sensible loan structure, cash buffers, and a clear view of the risks before using equity to buy.

Using Equity to Buy a Second House: Equity in Your Home

Equity is the difference between what your home is worth and what you still owe on the home loan.

For example, if a home is worth $800,000 and the mortgage balance is $400,000, you have $400,000 in equity. The basic calculation is current market value minus loan balance.

Banks usually calculate useable equity at up to 80% of the current market value, minus the loan balance. Borrowing above that level often means paying Lenders Mortgage Insurance, so the full equity figure is not always available.

To estimate useable equity, take 80% of your home value and subtract the existing mortgage balance.

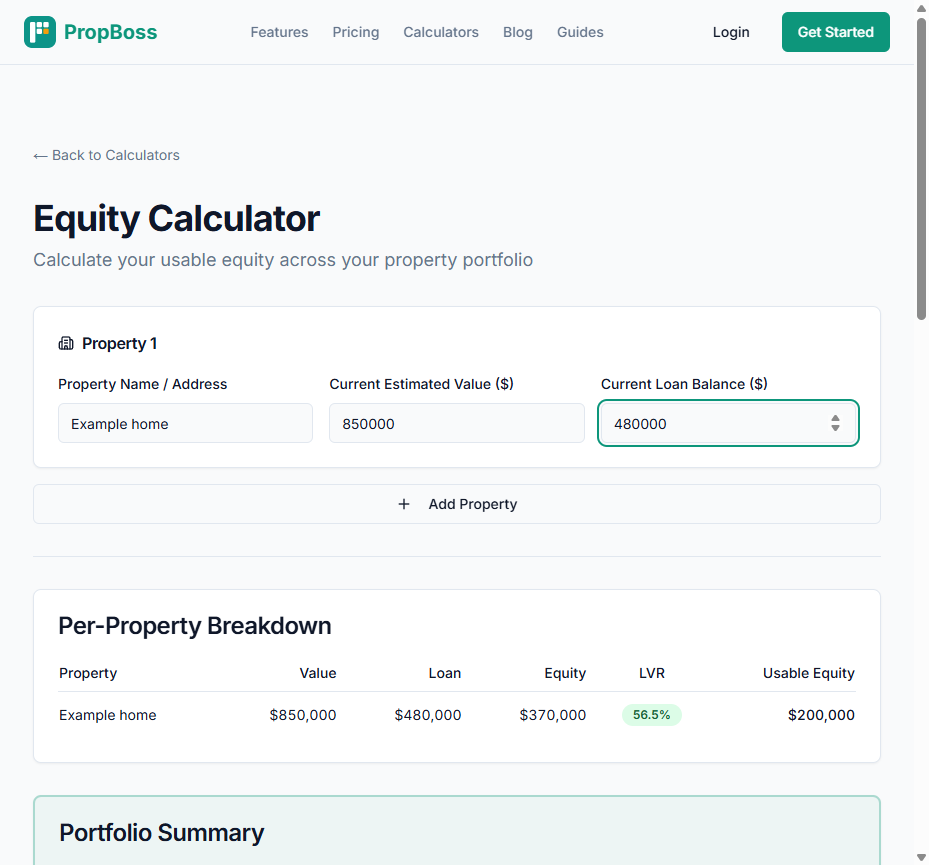

Take an $850,000 house with a $480,000 mortgage: 80% of $850,000 is $680,000. Subtract the $480,000 loan balance and you have $200,000 in useable equity that could help fund a second property.

How Much Equity Do You Actually Need to Buy Property?

The deposit required depends on the purchase price and whether the second property is a home you will live in or an investment property.

Most lenders prefer a 20% deposit to avoid LMI, plus enough equity or cash to cover stamp duty and buying costs.

For a $650,000 second property, the rough equity requirement might look like this:

| Cost | Amount |

|---|---|

| 20% deposit | $130,000 |

| Stamp duty (NSW estimate) | $24,740 |

| Legal and conveyancing fees | $2,500 |

| Loan application fees | $600 |

| Total equity needed | $157,840 |

That is why the useable equity number matters more than the headline equity number.

Do You Have Enough Equity?

If your useable equity is close to the figure above, you may be able to proceed.

If you are short, your options include paying LMI to borrow above 80% LVR, waiting for property values to rise, or making extra repayments to reduce the balance faster.

How to Use Home Equity to Buy Another Property

The process is not complicated, but it does need to happen in the right order.

Get a Current Market Valuation

Your lender will order a formal valuation to confirm the current market value. This determines how much equity you can access.

Do not rely only on online estimates. Bank valuations can be more conservative than realestate.com.au or app-based estimates.

Borrowing Power and Home Loan Specialists

A mortgage broker or home loan specialists at your bank will assess your financial commitments, living expenses, income, credit history, and existing debts.

In 2026, APRA requires lenders to apply a 3% interest rate buffer when calculating serviceability, so your borrowing power may be lower than the raw equity figure suggests.

Before proceeding, ask your accountant or registered tax agent how the loan structure affects tax deductions and record keeping.

Apply for a New Loan

There are three common ways to access equity: refinance your existing home loan, create a separate equity split, or cross-collateralise both properties under one lending structure.

Many investors prefer a separate split because it keeps the investment borrowing easier to track for tax and reporting.

Using Equity to Buy an Investment Property With a Home Loan

Buying an investment property rather than a second home adds a few extra issues.

Using equity to buy an investment property lets you enter the market without saving a large cash deposit. Rental income from tenants can also support borrowing power.

You may be able to claim deductions for interest, depreciation, and other property costs. For a broader portfolio view, read our guide on how equity works across an investment property portfolio.

Investment lending is usually assessed more tightly than owner-occupied lending. In 2026, investors should expect rates to be around 0.25-0.50% above comparable owner-occupier rates.

Before making an offer, model the repayments at the lender's assessment rate, not just the advertised rate.

Costs of Buying a Second House

You'll need to set aside more than just the deposit to cover these extra expenses:

- Transfer duty - varies by state. Use a stamp duty calculator before assuming the deposit is enough.

- LMI - if you borrow above 80% LVR, expect a bill that can run from about $8,000 to $35,000.

- Valuation and legal fees - typically $2,000-$4,000.

- Building and pest inspections - often $500-$800.

- Ongoing costs - council rates, insurance, repairs, and vacancy buffers need to be budgeted before settlement.

Tips to Help You Build Equity in Your Home Faster

Here are some smart ways to boost the equity in your existing home:

-

Make extra repayments - even an extra $200 a month on a $500,000 balance builds equity faster.

-

Use an offset account - parking savings against the loan balance can reduce interest while keeping the cash accessible.

-

Renovate selectively - a $30,000 kitchen renovation may add $50,000-$80,000 in value if it suits the local market.

-

Refinance your home loan - this triggers a new valuation and may reveal more current market value than the old loan file shows.

Risks of Using Equity to Buy Property

Using equity to invest in another property is common, but the risks involved are real:

-

Cross-collateralisation - if two properties secure the same loan, selling one can become more complicated.

-

Interest rates rise - a 1% increase on $800,000 of debt adds $8,000 a year in interest.

-

Values fall - if property prices drop, your available equity can shrink quickly.

-

Vacancy periods - no tenant means no rental income. Keep a cash buffer of 3-6 months' expenses.

Get Professional Advice

Before using a home equity loan, speak with an accountant or financial planner about the tax implications for your personal situation.

A financial adviser or registered tax agent can help you decide whether the investment strategy suits your income, debt level, and risk tolerance.

Professional advice matters even more if you already own multiple properties or plan to keep growing a portfolio.

This article is general information, not personal tax advice. Before acting, ask your adviser to review your existing property, property value, current loan, existing loan, loan amount, expected repayments, rent assumptions, vacancies, financial situation, financial circumstances, and whether you can afford the increased risk without creating financial stress.

Frequently Asked Questions

Can I Use Equity to Buy Property Without Saving a Deposit?

Yes. The equity in your home can replace a cash deposit when buying a new property, because the lender uses that equity as security.

You still need to cover buying costs such as stamp duty, legal fees, inspections, and loan costs.

How Does Equity Work When Buying a Second Home?

Your lender values your current home, subtracts the amount you owe, and then works out how much useable equity you can access. That amount can be used as the deposit for buying the new property.

Is There a Tool That Automates Equity Tracking?

PropBoss tracks equity positions across your investment properties with automated bank feeds, portfolio records, and ATO-compliant reporting. Start your free trial.

Keep Tabs on Your Equity Across Every Property

Stop guessing whether you have enough equity to buy another property.

PropBoss pulls in your financial data, tracks property values, and calculates usable equity across your portfolio.

The free equity calculator shows what you may be able to access before you speak to a lender. For a deeper look, see our can I afford an investment property.

Plans start from $1/property/month. Get started with a free trial.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more