Investment Property Depreciation Explained in Australia

Last updated: April 2026 · Financial year 2025-26

Investment property depreciation is one of the biggest tax levers Australian property investors underuse. It allows you to claim eligible wear and tear on the building and certain assets inside it, which can reduce taxable rental income and improve after-tax cash flow without increasing your weekly rent.

That matters in 2026 because many investors are still dealing with higher interest costs, tighter holding margins, and greater pressure to justify whether a property is truly working. A strong depreciation claim does not turn a bad investment into a good one, but it can materially change the after-tax outcome of a property that already makes strategic sense.

This guide explains how investment property depreciation works in Australia, what the difference is between depreciation schedules, capital works deductions, and plant & equipment, and how to estimate the impact on your own portfolio. Use it alongside the PropBoss Depreciation Estimator, the Cash Flow Calculator, and the Negative Gearing Calculator to test how the numbers move in practice.

Source note: the rule references in this guide were checked against current Australian Taxation Office rental-property depreciation guidance, including the ATO pages on depreciating assets, second-hand depreciating assets, and capital expenses, and reviewed against the live ATO guidance available on 30 April 2026.

This guide is general information only and is not personal tax, legal, or financial advice. Reviewed in the context of PropBoss product and investor workflows by Jonathan Zuvela, founder of PropBoss.

What Is Investment Property Depreciation?

Investment property depreciation is the tax deduction available for the decline in value of eligible parts of a rental property over time. In Australian tax language, you are generally dealing with two broad buckets: structural building deductions claimed over long periods, and shorter-life assets inside the property that wear out faster.

The concept is simple even if the reporting is not. A building ages. Fixtures and assets wear out. The tax system lets investors claim part of that decline in value where the property is used to produce rental income and the item qualifies under the current rules.

For investors, the practical importance is that depreciation is often a non-cash deduction. You might not spend an extra dollar this year, but you may still reduce your taxable rental income. That is why depreciation can materially improve the after-tax holding cost of a property even when rent, interest, and outgoings stay exactly the same.

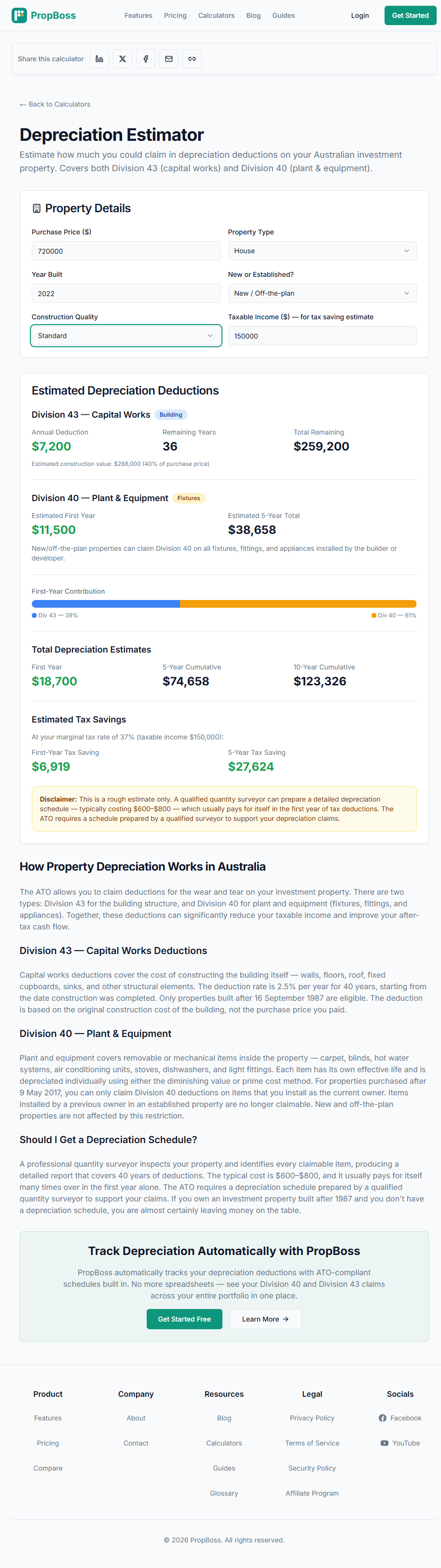

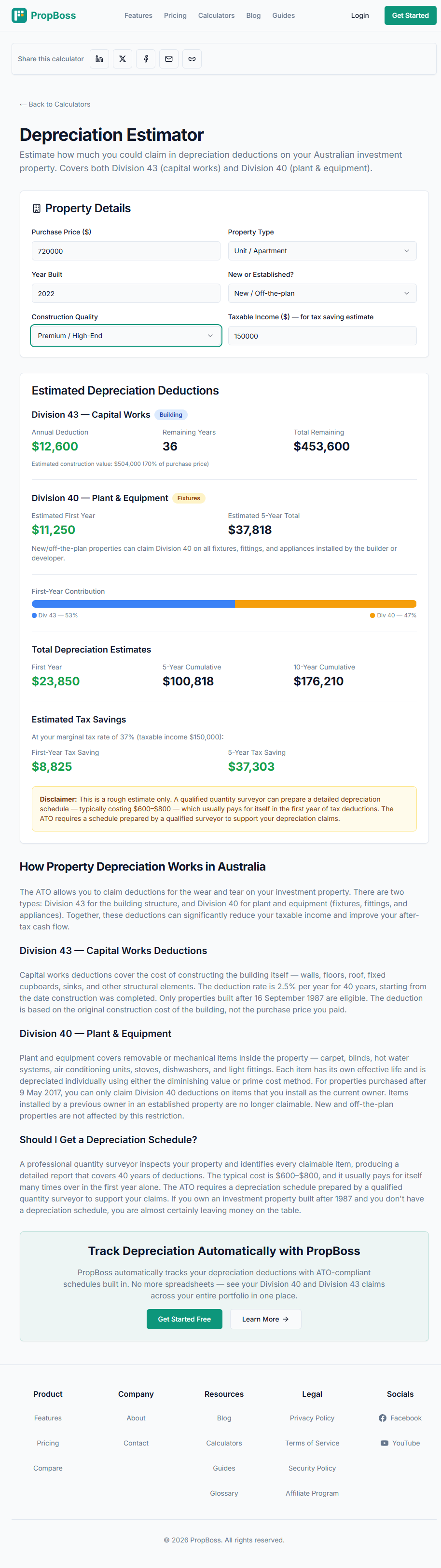

Worked Example - $720,000 Brisbane Investment Property

Assume you buy a near-new house in Chermside, Brisbane, for $720,000. Using the live PropBoss estimator with a 2022 build year, standard construction quality, and a taxable income of $150,000 produces the following directional estimate.

| Item | Annual Amount |

|---|---|

| Rental income ($760/week x 52) | $39,520 |

| Loan interest | -$31,600 |

| Rates, insurance, water, management, repairs | -$8,420 |

| Division 43 capital works claim | -$7,200 |

| Division 40 plant and equipment claim | -$11,500 |

| Total deductible expenses | -$58,720 |

| Net rental loss before tax | -$19,200 |

In this example, depreciation contributes $18,700 of first-year deductions without requiring a matching cash payment this year. At a 37% marginal rate, the estimator shows an indicative first-year tax saving of $6,919. If you only looked at rent minus cash expenses, you would miss a large part of the property's after-tax profile.

Estimate a similar scenario with the PropBoss Depreciation Estimator before you buy or before EOFY planning.

How Investment Property Depreciation Works

Step 1: Separate the building from the land

Land does not depreciate. The claim starts by separating the property into components that may be deductible and ignoring the land value for depreciation purposes.

Step 2: Classify each claim under the right category

Eligible structural elements usually sit under Division 43, while eligible removable or mechanical items sit under Division 40. This distinction matters because the timing and calculation method are different.

Step 3: Apply the correct rate or effective life

Division 43 is commonly claimed at 2.5% per year over 40 years for eligible residential construction. Division 40 assets are usually claimed based on effective life and the method used for the asset schedule.

Step 4: Apportion for ownership period and rental use

If you owned the property for part of the year, or there was any non-income-producing period, the claim needs to reflect that. The annual number is rarely a straight full-year figure for the first year.

Step 5: Feed the result into the real portfolio picture

Depreciation is only useful when it is connected to actual property decisions. Once you estimate the deduction, run it through the PropBoss Cash Flow Calculator and Negative Gearing Calculator to see how it changes the property's holding cost and tax position.

Tax Savings by Income Bracket - $10,000 Depreciation Deduction (2025-26 FY)

| Taxable Income | Marginal Rate | Tax Saved on $10K Deduction |

|---|---|---|

| $18,201 - $45,000 | 16% | $1,600 |

| $45,001 - $135,000 | 30% | $3,000 |

| $135,001 - $190,000 | 37% | $3,700 |

| $190,001+ | 45% | $4,500 |

The higher your marginal tax rate, the greater the immediate tax effect of the same deduction. That does not mean depreciation only matters to high-income earners. It means the same schedule can produce very different after-tax outcomes depending on who owns the property and how the ownership is structured.

Calculate your own estimate with the PropBoss Depreciation Estimator instead of relying on broad averages.

What Can You Claim Under Investment Property Depreciation?

| Claim Type | Description |

|---|---|

| Division 43 - building structure | Structural elements such as walls, roof, concrete, built-in cupboards, and eligible structural improvements. |

| Division 43 - capital improvements | Eligible extensions, structural renovations, and improvements that form part of the building. |

| Division 40 - appliances | Ovens, dishwashers, rangehoods, and other eligible removable assets, subject to the current rules. |

| Division 40 - floor and window assets | Carpets, blinds, and similar shorter-life assets where the item qualifies. |

| Division 40 - services equipment | Air conditioners, hot water systems, exhaust fans, smoke alarms, and similar assets where claimable. |

| Renovation components | New items you install yourself may be treated differently from items already in place when you bought the property. |

| Quantity surveyor or schedule support costs | Depending on the service and tax treatment, costs connected with preparing a schedule may also form part of the investor's tax workflow. |

If you are unsure whether an item belongs under plant and equipment or capital works, the safer move is to avoid guessing and model the property with a proper schedule workflow. The first time you mention a quantity surveyor in your own process is usually when accuracy starts improving.

For a deeper background on the technical split, see PropBoss's related article on Property Depreciation: A Complete Guide to Division 40 and Division 43 Claims.

New Build vs Established Property - Which Is Better for Depreciation?

| Factor | New Build | Established Property |

|---|---|---|

| Division 43 building claim | Usually strong if construction qualifies | Often still available if the building qualifies |

| Existing plant and equipment | More likely to be fully claimable when newly installed | Often restricted for previously used residential assets |

| First-year deduction size | Usually larger | Often more limited |

| Need for asset-level review | Important | Essential |

| Investor appeal | Higher tax leverage early on | More dependent on purchase price, age, and renovations |

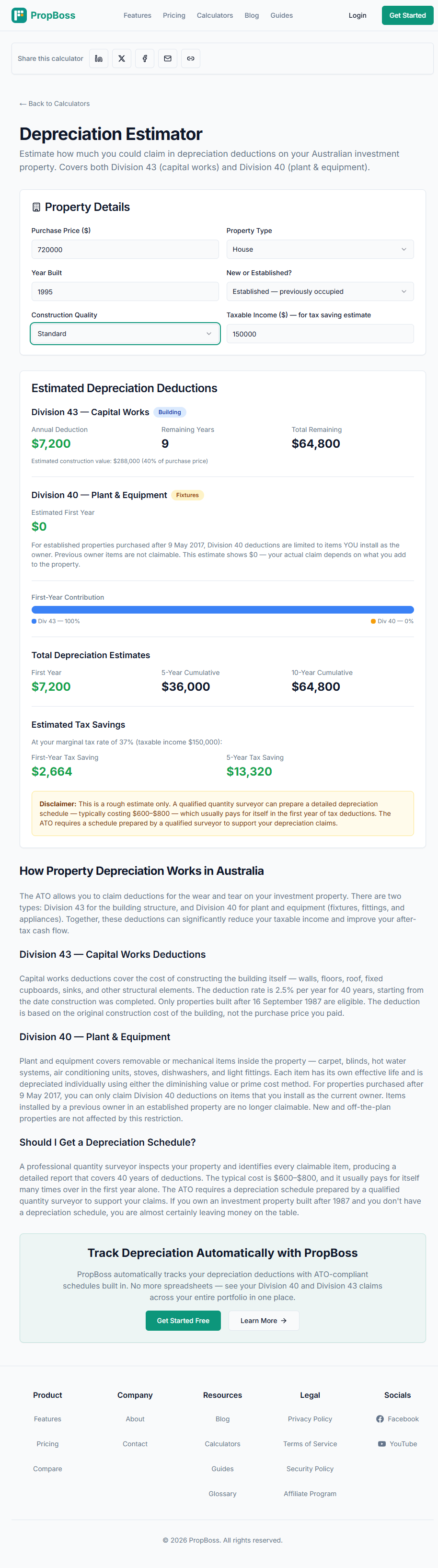

This is one of the biggest practical differences in the market. Newer properties often look stronger on depreciation because more of the asset base is still eligible and easier to substantiate. Established properties can still produce meaningful deductions, especially through Division 43, but investors should not assume the same result as a newly completed property.

Is Investment Property Depreciation Worth It in 2026?

In most cases, yes - but only when the property already makes sense without stretching the numbers. Depreciation is valuable because it improves the after-tax outcome of a rental property. It is not valuable if it becomes the only reason the purchase looks acceptable.

The 2026 environment makes that distinction more important. Holding costs remain meaningful for many investors, and a deduction that softens the tax bill can make a clear difference to annual cash flow. At the same time, depreciation does not fix weak rent, excessive debt, or a poor-quality purchase. It simply gives you a more accurate tax picture.

The right way to think about it is this: if two similar properties produce similar rent and similar risk, the one with better claimable depreciation may create a better after-tax result. That can matter when comparing a newer townhouse, a renovated unit, and an older house with limited claimable plant and equipment.

The Role of Division 40 and Division 43

The real engine room of depreciation is understanding the split between Division 40 and Division 43.

Division 40 - Plant and Equipment

Division 40 covers removable or mechanical assets such as carpets, blinds, appliances, air conditioners, and hot water systems. These assets have their own effective lives and are usually claimed faster than the building structure.

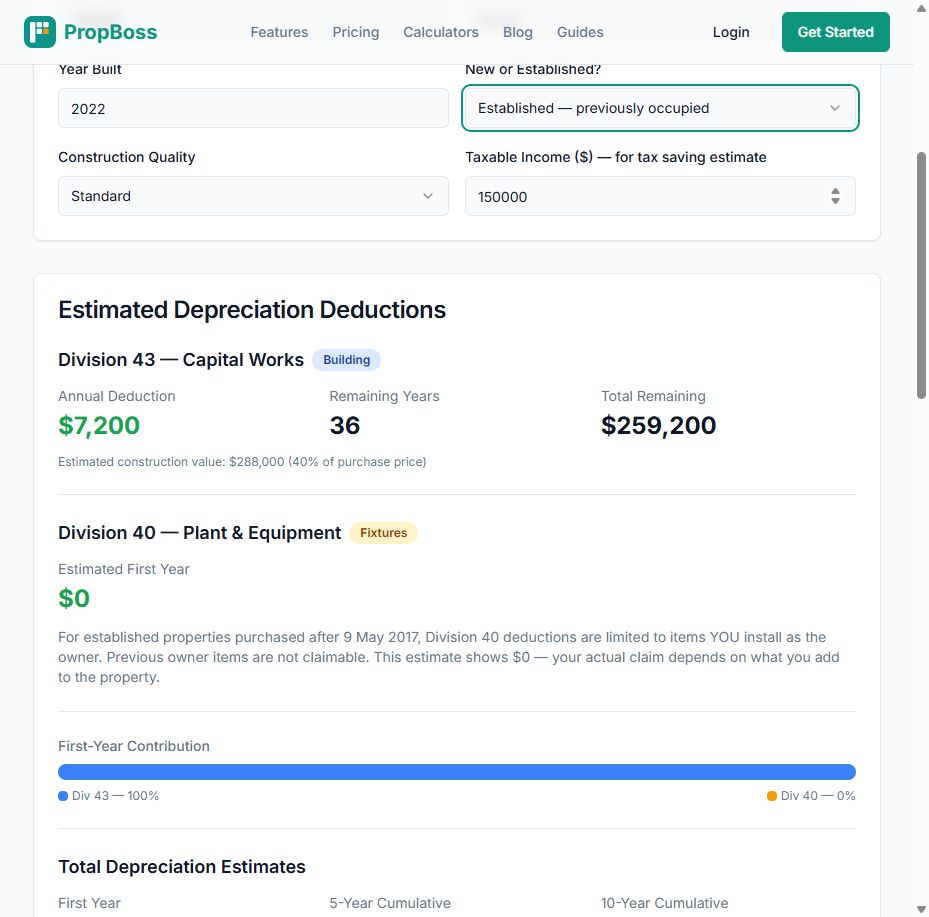

For residential investors, the current restriction that matters most is the treatment of previously used plant and equipment. For many established residential properties acquired after 9 May 2017, previously used plant and equipment cannot be claimed in the same way a newly installed asset can. That is why an older property may still have strong structural deductions but a much weaker plant and equipment profile.

Division 43 - Capital Works

Division 43 covers the building structure and eligible structural improvements. Residential construction that qualifies is commonly claimed at 2.5% per year over 40 years. That can create a long, steady deduction stream even when the property is not new.

Example: if the eligible construction cost is $280,000, a 2.5% annual claim produces $7,000 per year. Over time, that becomes one of the most stable tax offsets in the property's holding period.

This is also why depreciation is not just a "new apartment" topic. Investors often underestimate how much of the claim on an established property can still come from the building structure itself.

Common Depreciation Mistakes Investors Make

1. Treating all depreciation as the same

Investors often collapse everything into one number and miss the difference between structural claims and asset claims. That leads to bad comparisons between properties.

2. Assuming old properties have no claim

Many older properties still have eligible capital works deductions. The fact that plant and equipment may be restricted does not mean the entire property has no depreciation value.

3. Buying on the deduction alone

Depreciation should improve a sound acquisition, not justify a weak one. If the property only works after aggressive tax assumptions, the issue is usually the deal, not the tax treatment.

4. Forgetting private-use or timing adjustments

If the property was not income-producing for the full year, the claim may need to be apportioned. First-year claims are rarely plug-and-play.

5. Not connecting depreciation to cash flow

A schedule tells you the deduction. It does not tell you whether the property is comfortable to hold. Pair the deduction with the PropBoss Cash Flow Calculator to see the practical effect.

6. Ignoring the sell-side implications

Claiming depreciation can affect your tax position when you eventually sell. That does not make the deduction wrong, but it means investors should view depreciation as part of the whole property life cycle.

For a practical investor view, also read Depreciation: The Tax Deduction Most Property Investors Miss.

How To Calculate Depreciation on an Investment Property

The broad formula is:

Total annual depreciation = Division 43 capital works claim + Division 40 asset claims - any required apportionment

Here is a simplified worked example:

| Item | Annual Amount |

|---|---|

| Eligible construction cost | $300,000 |

| Division 43 claim at 2.5% | $7,500 |

| Eligible plant and equipment claim | $4,200 |

| Gross annual depreciation | $11,700 |

| Ownership/apportionment adjustment | -$1,170 |

| Net claim for the tax year | $10,530 |

If the investor is on a 37% marginal rate, that $10,530 deduction reduces tax by roughly $3,896.10. That does not mean the property "made" $3,896.10. It means the after-tax cost of holding the property is lower than it first appears.

Use the PropBoss Depreciation Estimator to get a fast directional number, then test the portfolio impact in the Portfolio Return Calculator.

Frequently Asked Questions

What is investment property depreciation?

Investment property depreciation is the deduction for the decline in value of eligible parts of a rental property over time. In practice, investors usually claim either structural capital works deductions, plant and equipment deductions, or both depending on the property and the current residential rental rules.

How does depreciation on an investment property work in Australia?

It works by identifying eligible assets or building components, assigning them to the correct tax category, and spreading the deduction across the relevant period. The final annual claim then reduces taxable rental income and may improve the investor's after-tax cash position.

What is the difference between Division 40 and Division 43 depreciation?

Division 40 usually deals with removable assets and shorter-life items, while Division 43 deals with the building structure and eligible structural improvements. The distinction matters because the rates, timing, and claim restrictions are not the same.

How do you calculate depreciation on an investment property?

You start by identifying the eligible construction and asset components, apply the relevant rate or effective life, and then adjust for ownership period or non-rental use where required. Many investors estimate the likely claim up front and then use a detailed schedule to support the final reporting position.

Do you need a depreciation schedule for an investment property?

A schedule is not just paperwork. It is often the cleanest way to support the claim and avoid under-claiming. The more complex the property, renovation history, or asset mix, the more useful a detailed schedule becomes.

Can you claim depreciation on an older or established property?

Often yes, especially for eligible capital works. The main caution is that previously used residential plant and equipment is treated differently from newly installed items, which means established-property deductions can still be strong but are usually less straightforward.

What items can you claim under plant and equipment depreciation?

Typical examples include carpets, blinds, appliances, hot water systems, and air conditioners where the asset is eligible under the current rules. The right answer depends on whether the asset is new, when it was acquired, and how it is being used in the rental property.

How does depreciation affect your tax return and cash flow?

Depreciation reduces taxable rental income, which can reduce the tax payable on net rent or increase the size of a rental loss. Because many depreciation deductions are non-cash, they can improve the after-tax cost of holding a property without changing the rent received.

Is a depreciation estimate enough or do you need a quantity surveyor report?

A quick estimate is useful for screening and planning, especially before you commit to a purchase. A detailed report is more appropriate when you need a stronger basis for a meaningful claim, have construction or renovation complexity, or want a clearer asset-by-asset schedule.

Does claiming depreciation affect capital gains tax when you sell?

It can. Previous claims may affect the tax treatment of the property or specific assets when the property is sold. Investors should treat depreciation as part of the whole acquisition-to-sale tax journey, not as an isolated refund strategy.

Track Your Investment Property Depreciation Automatically With PropBoss

Strong investors do not just ask what they can claim. They ask how the claim changes cash flow, tax, and portfolio performance across the year. PropBoss helps connect those numbers so you can model the property before purchase, plan for EOFY, and keep cleaner records as the portfolio grows.

Get Started Free | Try the Depreciation Estimator

Related Guides & Tools

- Depreciation Estimator - estimate likely deductions on a rental property

- Cash Flow Calculator - test pre-tax and after-tax holding costs

- Negative Gearing Calculator - model how deductions change taxable income

- Portfolio Return Calculator - see depreciation in the context of total returns

- Property Depreciation: A Complete Guide to Division 40 and Division 43 Claims

- Depreciation: The Tax Deduction Most Property Investors Miss

Estimate the deduction before EOFY

Use the estimator to compare new versus established properties, test the impact of building age, and see how depreciation changes your after-tax holding cost.