Rental Property Record Keeping Guide Australia 2026

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

A practical rental property record keeping guide for Australian property investors, covering rental income, loan interest, repairs, capital improvements, portfolio review, and tax-time evidence.

For Australian property investors, rental property record keeping guide should give a clear answer first: keep every record that explains ownership, rental income, borrowing costs, repairs, capital improvements, tax deductions, and the decisions you made along the way. The practical goal is not to keep a larger filing cabinet. It is to make sure every property can be reviewed, compared, refinanced, and handed to an accountant without guesswork.

A strong investor file connects the document to the decision. A loan statement matters because it explains interest, offset balances, and repayment structure. A property manager statement matters because it ties rent received to vacancy and management costs. A repair invoice matters because the tax treatment can change depending on whether the work restored the property or improved it. PropBoss is built around that same idea: each property should have a clean record, current numbers, and a next action.

Why record keeping matters for property investors

Most portfolio problems start small. A rent increase is not logged. A lender changes the repayment amount. A council rate notice sits in email but never reaches the spreadsheet. None of those misses looks serious on its own, but together they distort yield, cash flow, borrowing capacity, and tax preparation.

The Australian Taxation Office rental property guidance is a useful anchor because it treats rental property records as evidence, not decoration. If a deduction, capital cost, or rental income figure cannot be explained later, the investor carries the risk. That is why this guide treats record keeping as part of portfolio management rather than an annual tax chore.

The investor outcome is simple. You should be able to open one property record and answer four questions:

- what the property earned

- what it cost to hold

- what changed during the year

- what decision should happen next

The core records every investor needs

Start with the documents that prove the investment exists and explain the money moving through it. The essential file usually includes the purchase contract, settlement statement, loan approval, current loan split details, property manager statements, lease records, insurance, rates, strata notices, repairs, improvements, and sale documents if the property has been sold.

For tax time, the most useful structure is one folder or software record per property, not one folder per supplier. That means the Brisbane townhouse, Perth unit, or regional house each has its own income, expenses, loan, document, and review trail. This makes the accountant handover cleaner and keeps the investor focused on asset performance.

| Record type | Why it matters | Review rhythm |

|---|---|---|

| Rental income | Confirms rent received, vacancy, arrears, and agent fees | Monthly |

| Loan interest | Supports interest deductions and cash flow checks | Monthly |

| Rates, strata, insurance | Captures recurring holding costs | Quarterly |

| Repairs and maintenance | Supports deduction review and property condition history | As invoices arrive |

| Capital improvements | Separates improvement costs from ordinary repairs | Before tax time |

| Depreciation schedule | Supports building and plant deduction claims | Annual |

Separate repairs from improvements

Repairs and improvements are easy to mix together when everything is saved as a generic expense. A plumber replacing a broken fitting is not the same as renovating a bathroom. A small repaint between tenants is not the same as adding a new structure. The distinction matters because the tax timing and evidence can change.

The ATO guide to rental expenses investors can claim is a useful reference point when reviewing categories. The ATO page on capital works deductions is also relevant because many investors accidentally treat larger works as if they were ordinary repairs. PropBoss cannot replace tax advice, but it can make the conversation easier by keeping the invoice, date, property, note, and category together.

Use a short note whenever an item could be questioned later. A useful note says what happened, which part of the property was affected, whether the work restored a damaged item, and whether anything new was added. That note is much easier to write while the job is fresh than twelve months later.

Worked example: one missed cost changes the story

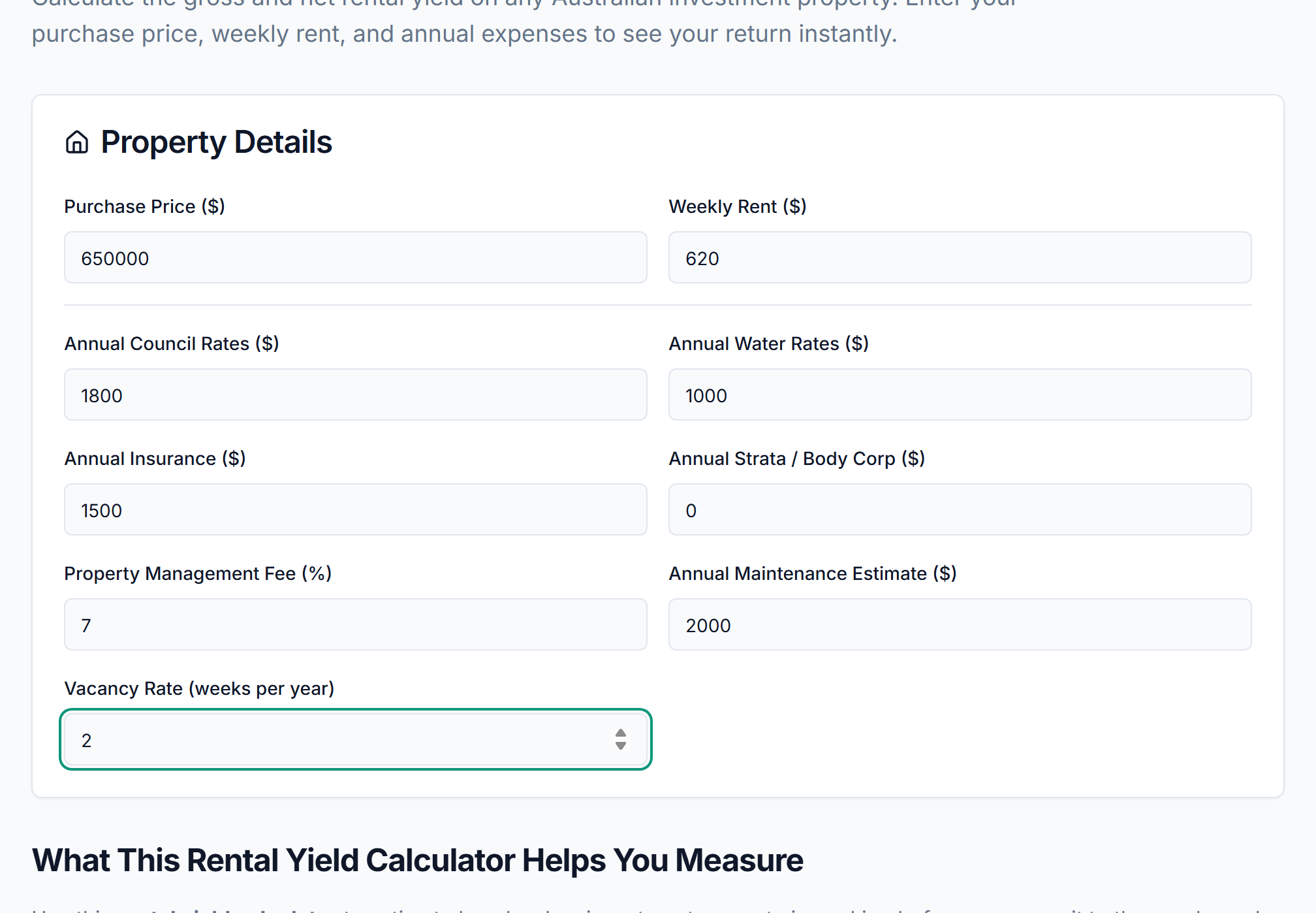

Assume an investor buys a $650,000 property and receives $620 per week in rent. The gross rent is $32,240 a year, which looks like a 4.96 percent gross yield before costs. If the investor forgets $2,400 in strata levies, $1,100 in insurance, and $900 in water charges, the property appears $4,400 stronger than it is.

That error does more than change a spreadsheet. It can influence whether the investor thinks the property is ready for a refinance, whether the rent review looks urgent, and whether the portfolio is carrying enough cash buffer. A missed recurring cost can make a marginal property look healthy.

The fix is not complicated:

- record recurring costs against the correct property

- check rent received against the property manager statement

- check loan interest against the lender statement

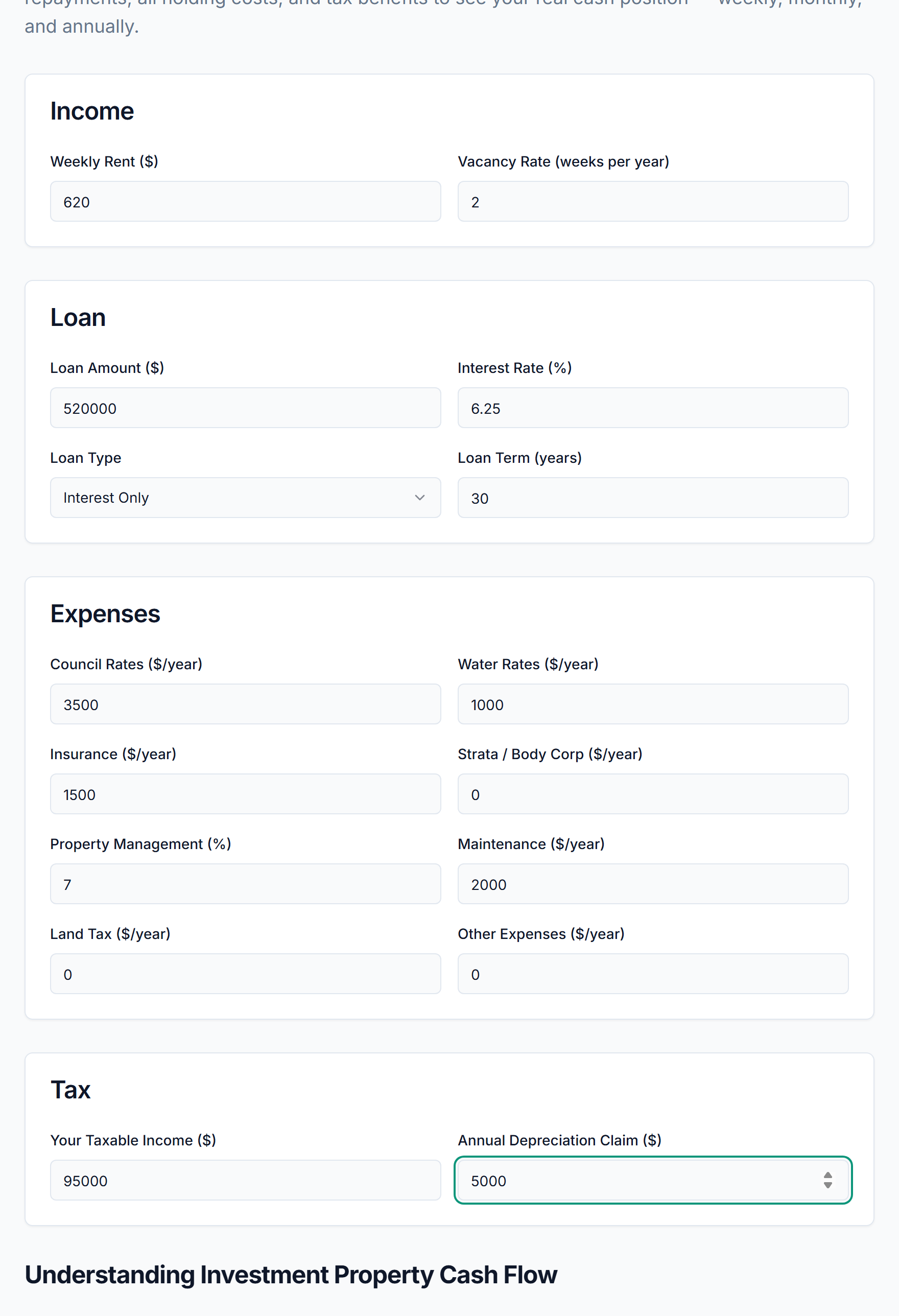

- compare the updated numbers in the rental yield calculator

- review monthly cash position with the cash flow calculator

Monthly workflow for investors

A monthly workflow keeps the file current without turning property investing into a second job. The aim is to catch missing documents and wrong assumptions while they are still easy to fix.

Start with rent. Confirm the property manager statement matches the rent expected under the lease. Note arrears, vacancy, letting fees, management fees, and maintenance charges that were deducted before money reached your bank account. Then check the loan statement. Record interest, repayments, offset balance, redraw activity, and any rate change.

Next, review expenses. Every invoice should be attached to one property and one category. If an invoice covers more than one property, split it while the detail is still clear. If it relates to a repair or improvement, add a note with enough context for an accountant to review later.

Finally, update the decision view. Look at yield, cash flow, upcoming lease dates, insurance renewal, loan expiry, and maintenance follow-up. PropBoss works best when the property record is not just a document store but a decision surface.

Tax-time preparation

Tax preparation is easier when the investor has already done the monthly work. The end-of-year process should be a review, not a reconstruction. Each property should have income, expenses, loan interest, capital costs, depreciation evidence, and notes ready to hand over.

Use the tax deduction checklist before sending records to an accountant. It helps investors think through common categories such as interest, property management fees, council rates, repairs, insurance, depreciation, borrowing costs, and travel restrictions. The checklist does not decide deductibility, but it reduces the chance that a valid document is missed.

Mixed-use loans deserve extra care. If a loan has private and investment use, the record needs to explain the split. Do not rely on memory or a single bank balance. Keep the loan purpose, redraw notes, and adviser guidance with the property file so the future review is based on evidence.

Portfolio comparison

The first property can often survive a spreadsheet. The second and third property usually expose the cracks. Different agents send statements in different formats. Lenders use different wording. Insurance renews on different dates. One property has strata, another has land tax, and another has higher repairs after a vacancy.

That is when comparison becomes more valuable than storage. Investors need to see which property is carrying cash flow pressure, which one has the strongest gross yield, which one has rising fixed costs, and which one needs a rent or loan review. A tidy folder does not answer those questions by itself.

PropBoss gives each property a consistent structure so the portfolio can be scanned. The investment property calculator is useful for comparing a possible purchase with the current portfolio before adding another asset.

Internal links and money-page alignment

Helpful PropBoss content should support the next investor action. For this topic, the next action is not only reading another article. It is opening the numbers and checking the portfolio. That means the article should connect to calculators, checklists, and account creation without forcing the reader through a sales page.

The best internal path is:

- use the rental yield calculator to confirm headline return

- use the cash flow calculator to check holding pressure

- use the tax deduction checklist to prepare accountant questions

- create your PropBoss account when the investor wants property records in one place

Common mistakes to avoid

The most common mistake is saving documents without assigning them to a property. The second is recording every cost as an ordinary expense. The third is waiting until tax time to reconstruct what happened. The fourth is keeping the numbers separate from the documents, which makes it hard to explain why a figure changed.

Another common mistake is treating gross yield as the whole story. Gross yield is useful, but it hides debt, repairs, vacancy, insurance, strata, land tax, and capital costs. A property can look strong on rent and weak on cash flow. Investors need both views.

Finally, avoid duplicate spreadsheets. If two versions exist, neither one is trusted. Pick one source of truth and keep it current.

FAQ

How long should Australian property investors keep records?

Investors should keep records long enough to support tax, capital gains, loan, and ownership questions. Tax record periods can depend on the item and circumstance, so confirm the exact retention requirement with your accountant or the ATO. For property, it is sensible to keep purchase, improvement, depreciation, and sale evidence for the full life of the asset and beyond the sale review period.

Should repairs and improvements be tracked separately?

Yes. Repairs, maintenance, capital works, and depreciating assets should be separated because they can be treated differently. The invoice alone may not explain the difference. Add a short note describing what happened and whether the work restored something existing or added something new.

Is a spreadsheet enough for one investment property?

A spreadsheet can work for one property if the investor is disciplined, the loan is simple, and documents are stored consistently. It becomes weaker when there are multiple properties, shared ownership, loan splits, recurring costs, or regular decisions to compare.

What should I review each month?

Review rent received, agent fees, loan interest, recurring expenses, repairs, upcoming lease dates, insurance renewal, and the current yield and cash flow view. The monthly check should take minutes when documents and numbers are already attached to the property.

Track your property portfolio with PropBoss

PropBoss helps Australian investors keep property records, calculators, checklists, and portfolio review notes in one place. Start with one property, attach the key records, check the numbers, and then add the rest of the portfolio when the workflow feels clean. When you are ready to move beyond scattered spreadsheets, create your PropBoss account.

Track Your Real Portfolio with PropBoss

Stop guessing with calculators and spreadsheets. PropBoss automatically tracks your rental income, expenses, bank feeds, depreciation, and tax position across your entire portfolio.

Jonathan Zuvela

Founder, PropBoss

Jonathan is an Australian property investor and the founder of PropBoss - an AI-powered platform that helps investors automate their property admin, track rental income and expenses, and make data-driven investment decisions.

Related Articles

Cash Flow Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep cash flow records accurate across rent, loan interest, recurring costs, repairs, and portfolio review.

Read more

Property Investment Record Keeping Checklist Australia 2026

A practical checklist for Australian property investors to keep rental income, loan, expense, tax, and portfolio records organised before tax time.

Read more

ATO Data Matching for Property Investors: What the ATO Sees

Learn what ATO data matching means for property investors, which records the ATO can cross-check, and how to stay review-ready before tax time.

Read more